Leasing can look attractive because of its lower monthly payments, but the tradeoff is limited flexibility and no ownership. Common drawbacks include mileage restrictions, wear-and-tear fees, early termination penalties, and the need to return the vehicle at the end of the lease. While you may enjoy driving a newer car, years of payments typically leave you with no equity and no asset to sell or trade in.

That doesn’t mean leasing is always foolish. It can work for low mileage drivers who want a new vehicle under warranty and don’t care about ownership. But if your goal is financial control, lower long term costs, and real car ownership, buying or financing a reliable used or certified pre-owned vehicle usually gives you more power.

Is Leasing a Car a Good Idea?

Whether leasing a car is a good idea depends on your driving habits, budget, and long-term financial goals.

Pros of Leasing a Car

Leasing typically offers lower monthly payments than financing the same vehicle, making it easier to drive a newer model with the latest features. Most leases also keep you under the manufacturer’s warranty, reducing the risk of expensive repair bills. At the end of the lease, you simply return the vehicle and choose your next one, without worrying about selling or trading it.

Cons of Leasing a Car

The biggest downside is that you don’t build ownership or equity. Lease agreements also come with mileage limits, potential wear-and-tear charges, and early termination fees. For drivers who put on a lot of miles or prefer to keep a car for many years, these restrictions can make leasing more expensive than expected.

The Brutal Reality: 10 Reasons Not to Lease a Car

1. You Own Absolutely Nothing

The harshest truth about leasing is that your payments don’t build equity. When you finance a car, each payment slowly moves you toward ownership. When you lease, you’re paying for the right to use the vehicle for a short period. At the end, you return it. You may have made 36 payments, but you don’t have an asset, resale value, or trade in value.

2. The Mileage Trap

Most leases limit you to 10,000, 12,000, or 15,000 miles per year. That may sound fine until life changes. A longer commute, road trips, school runs, family visits, or a new job can push you over the limit fast. Excess mileage fees may cost around $0.15 to $0.30 per mile. Drive 5,000 miles over the limit, and you could owe $750 to $1,500 just for using the car.

3. Punishing Early Termination Fees

A lease is not easy to escape. If you lose your job, move, need a bigger vehicle, or simply regret the deal, early termination fees can be brutal. You may owe remaining payments, penalties, and extra charges. This is one of the strongest reasons not to lease a car if your life is likely to change within the next few years.

4. Excess Wear Charges

Dealers expect the car back in clean, marketable condition. Small dents, stained seats, scratched wheels, cracked glass, worn tires, and interior damage can all become excess wear charges. Normal family life can become expensive at lease end, especially if you have kids, pets, tight parking, or rough weather.

5. Mandatory High Cost Insurance

Leased vehicles usually require full coverage insurance with strict limits. That often means comprehensive, collision, and higher liability coverage. Gap insurance may also be required or strongly recommended. Your monthly lease payment may look low, but the insurance bill can reduce the savings quickly.

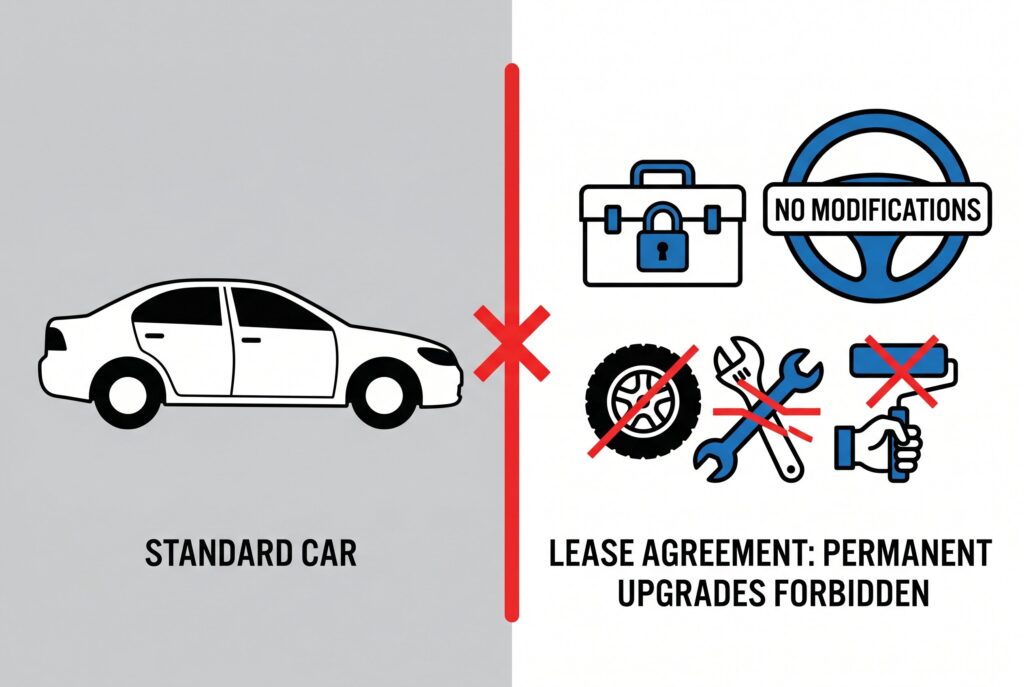

6. No Customization Freedom

When you lease, the car isn’t truly yours. You usually can’t modify the suspension, change the paint, add major accessories, tint windows beyond legal or contract limits, or make permanent upgrades without permission. Even small changes may need to be reversed before return.

7. Strong Credit Is Often Required

Attractive lease deals usually go to borrowers with excellent credit. If your credit score is average or damaged, you may face higher money factors, larger upfront payments, or worse terms. The advertised lease deal may not be the deal you actually qualify for.

8. The Money Factor Hides the Real Interest

Lease contracts can be confusing because they don’t always show interest the same way a loan does. Instead, they use a money factor. To estimate the APR, multiply the money factor by 2,400. A money factor of 0.0025 is roughly 6% APR. If you don’t understand this number, it’s easy to focus only on the payment and miss the true cost.

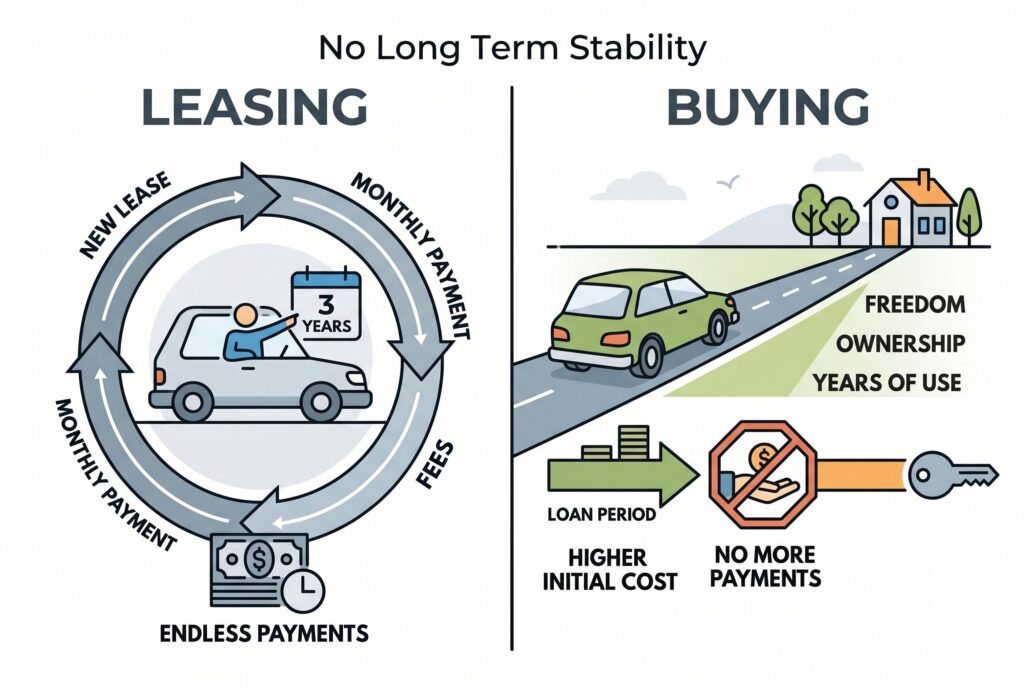

9. No Long Term Stability

Leasing can trap you in an endless payment loop. Every few years, you return the car and start over with another contract, another set of fees, and another monthly payment. Buying may cost more at first, but once the loan is paid off, you can enjoy years without a car payment.

10. Total Loss Can Become Complicated

If a leased car is stolen or totaled, insurance and gap coverage become critical. Without the right protection, you may face financial stress because the car’s market value, lease payoff, and insurance payout may not line up neatly. Always confirm gap coverage before signing.

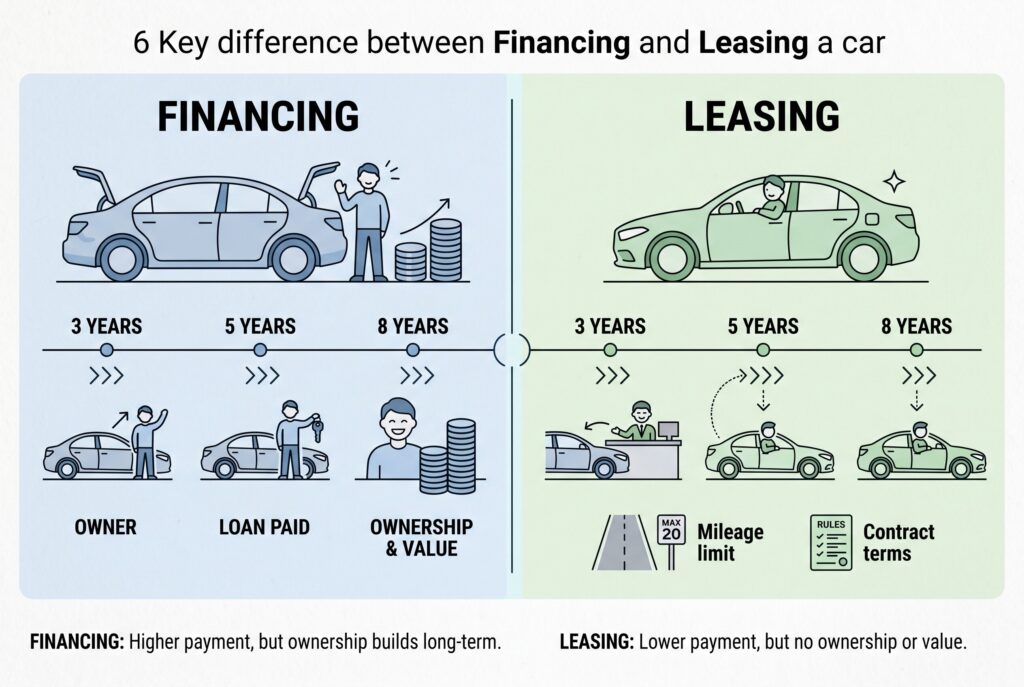

Leasing vs Financing a Car

- Ownership: Financing leads to ownership once the loan is paid off, while leasing only gives you the right to use the vehicle for a fixed period.

- Monthly Payments: Lease payments are typically lower because you’re paying for depreciation. Finance payments are usually higher because you’re paying toward the full purchase price.

- Long-Term Value: Financing allows you to build equity in the vehicle. Leasing does not create any ownership value or trade-in asset.

- Flexibility: Financed vehicles can be kept, sold, traded, modified, or driven as much as you want. Leased vehicles are subject to mileage limits and contract restrictions.

- End of Term: After financing, you own the car outright. At the end of a lease, you usually return the vehicle unless you choose to buy it.

- Total Cost Over Time: Leasing may save money in the short term, but financing often becomes more affordable in the long run if you keep the vehicle for several years after the loan is paid off.

Conclusion

Leasing can make sense if you drive predictable miles, want a new car every few years, and value lower monthly payments. But the tradeoff is less flexibility and no ownership. Mileage limits, wear-and-tear fees, early termination charges, and the lack of equity can make leasing more expensive than it first appears.

Before signing, ask yourself one question: do you want temporary access or long-term control? If ownership, freedom, and lower lifetime costs matter to you, financing a reliable used or certified pre-owned vehicle is often the smarter choice.