The term “policyholder” simply refers to the person or organization that purchases an insurance policy and holds the contractual rights under that policy. They buy the policy, pay the premiums, receive official policy documents, and usually have the legal power to change coverage, add or remove people, update beneficiaries, or cancel the contract.

How to Find the PolicyHolder on Insurance Card

Finding the policyholder on an insurance card depends on the type of insurance. Insurance companies don’t always use the word “policyholder” directly, which is why people get confused.

On an auto insurance card, look for “Named Insured,” “Insured,” or the name printed most prominently near the top. In most personal auto policies, that person is usually the policyholder or one of the named insureds. If your spouse, child, or another driver is listed elsewhere, they may be covered, but they may not own the policy.

On a health insurance card, the language can be different. You may see “Subscriber,” “Member Name,” “Enrollee,” or “Dependent.” If your insurance comes through an employer, the employer may technically hold the group policy, while you are the subscriber or member. Your spouse or children may appear as dependents. That doesn’t mean they control the plan.

On homeowners insurance documents, the policyholder is usually found on the declarations page, not a wallet card. Look for “Named Insured” or “Policyholder.” If you have a mortgage, your lender may be listed too, but that doesn’t make the bank the owner of your policy. The lender is usually listed to protect its financial interest in the property.

The CEO Powers: What Policyholders Can Usually Do

Policyholder rights vary by policy type, company, and state, but the core powers are similar. The policyholder can usually change coverage limits, pay premiums, update billing details, request documents, add or remove vehicles, add drivers, change deductibles, add endorsements, file claims, and cancel the policy.

In life insurance, the policyholder may also change beneficiaries, borrow against certain permanent policies, adjust payment methods, or surrender the policy, depending on the contract. But those powers aren’t unlimited. Some changes may require underwriting, consent from another owner, proof of insurable interest, or a new policy. For example, adding a high risk driver to an auto policy may change the premium. Increasing life insurance coverage may require health questions or a medical review.

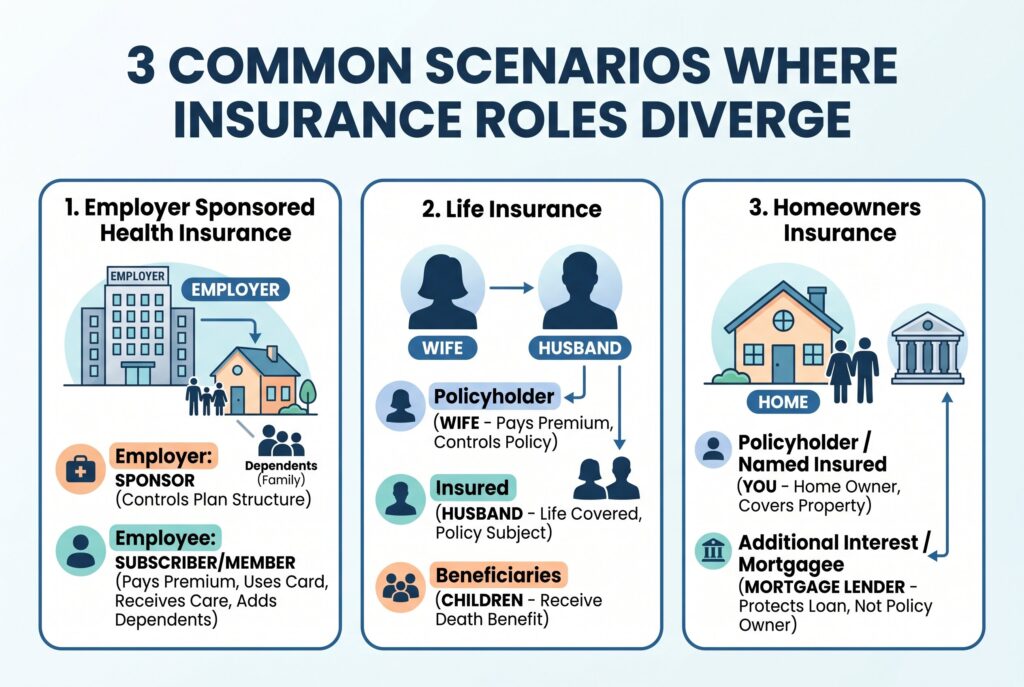

3 Common Scenarios Where Roles Diverge

1. Employer Sponsored Health Insurance

Your employer may sponsor the group plan. You may be the subscriber or member. Your spouse and children may be dependents. In daily life, you use the card, pay part of the premium, and receive medical care, but the employer still controls the group policy structure.

2. Life Insurance

A wife may buy a policy on her husband if she has an insurable interest and the insurer allows it. In that case, she may be the policyholder, he may be the insured, and their children may be beneficiaries. Three different roles can exist in one policy.

3. Homeowners Insurance

You may be the policyholder and named insured. Your mortgage lender may appear as an additional interest or mortgagee. That protects the lender’s loan, but it doesn’t make the lender the owner of your home insurance policy.

Can You Change a Policyholder?

Usually, you can’t simply transfer a policyholder name like changing a phone contact. Many insurance policies must be canceled and rewritten if ownership changes. For example, if you buy a car from your father, you usually can’t just remove his name and replace it with yours on his old auto policy. You need your own policy because you’re now the owner and primary risk. The same idea can apply after divorce, death, business ownership changes, or property transfers.

Some life insurance policies may allow ownership transfer, but that is more formal and may have tax or legal consequences. Always ask the insurer before assuming the change is simple.

Conclusion

The policyholder is the person who owns and controls the insurance policy, even though they are not always the one receiving the benefits or using the coverage. The answer to who is the policyholder for insurance is simple: it’s the person or organization that owns the policy and controls its terms.

Because insurance cards and policy documents use different terms, it’s worth taking a moment to identify who holds that role. Checking for labels such as “Policyholder,” “Named Insured,” “Subscriber,” or “Policy Owner” before filing a claim or updating your coverage can help you avoid unnecessary delays and confusion.