")

Many people treat every loan as a burden, but debt isn’t automatically good or bad. The difference in good debt vs bad debt depends on what the debt does to your future net worth. What is good debt? It’s borrowing used to buy assets, skills, or opportunities that may rise in value or create future income. What is bad debt? It’s borrowing, usually at a high interest rate, to buy things that lose value, create no income, or disappear long before the bill is paid. Smart borrowing isn’t about avoiding debt forever. It’s about using debt as leverage instead of letting debt control your life.

The Defining Line: ROI and Depreciation

The core rule is simple. Good debt has a reasonable chance of producing a return greater than its cost. Bad debt drains cash without building long term value.

ROI, or return on investment, is the key. If a loan helps you earn more money, build equity, increase income, or create a productive asset, it may be good debt. If the loan pays for short term consumption, depreciating assets, or lifestyle upgrades you can’t afford, it’s likely bad debt.

Interest rate matters too. A loan used for a productive purpose can still become dangerous if the APR is too high. Debt management starts with asking two questions: what am I buying, and what is this money really costing me?

| Criteria | Good Debt | Bad Debt |

| Purpose | Funds an investment, education, business, or asset that can generate future value | Pays for consumption, lifestyle spending, or non-essential purchases |

| Expected Return | Likely to produce a return greater than the borrowing cost | Unlikely to generate any financial return |

| Impact on Wealth | Builds net worth, equity, income, or productive assets | Reduces future cash flow without creating long-term value |

| Examples | Mortgage on an affordable home, business loan, student loan with strong earning potential | Credit card debt for shopping, vacations, luxury goods, or lifestyle upgrades |

| Interest Rate | Reasonable and manageable relative to expected returns | High APR that can quickly compound and become difficult to repay |

| Long-Term Effect | Strengthens financial position over time | Increases financial stress and weakens long-term finances |

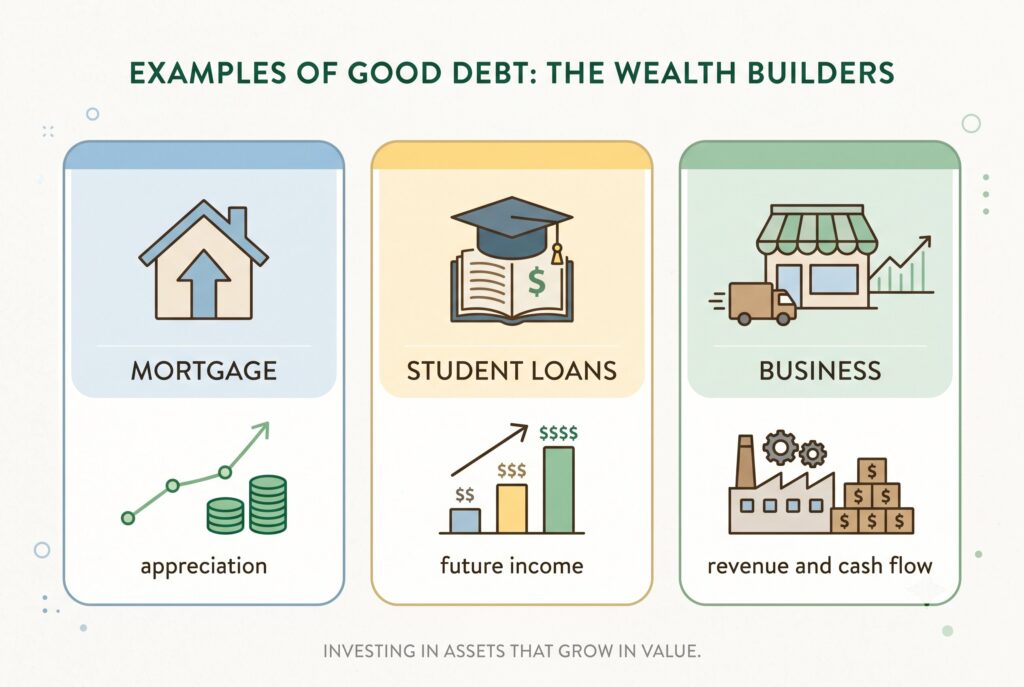

Examples of Good Debt: The Wealth Builders

1. Mortgage Debt

Mortgage debt is often considered good debt because it can help you buy an appreciating asset. A home may rise in value over time, provide stability, and build equity as you pay down the loan.

But a mortgage isn’t automatically good. If the payment consumes too much income, taxes and maintenance are ignored, or the buyer has no emergency fund, the house can become a financial trap. Good mortgage debt is affordable, fixed within a realistic budget, and tied to a home you can hold long enough to benefit from appreciation.

2. Student Loan Debt

Student loan debt can be good debt when it increases future income. A degree, certification, or professional license can raise earning power for decades.

The danger is borrowing without checking the expected salary. A $30,000 loan for a career that raises income by $25,000 per year may be reasonable. A $150,000 loan for a career that starts at $40,000 per year isn’t smart leverage. The value of education debt depends on outcome, not prestige.

3. Business Debt

Business debt can create wealth if it funds equipment, inventory, marketing, hiring, or systems that increase revenue and cash flow. For entrepreneurs, borrowing can speed growth when the business model is already proven. But business loans are risky when used to cover losses, delay hard decisions, or chase growth without profit. Good business debt should have a clear repayment plan and measurable return.

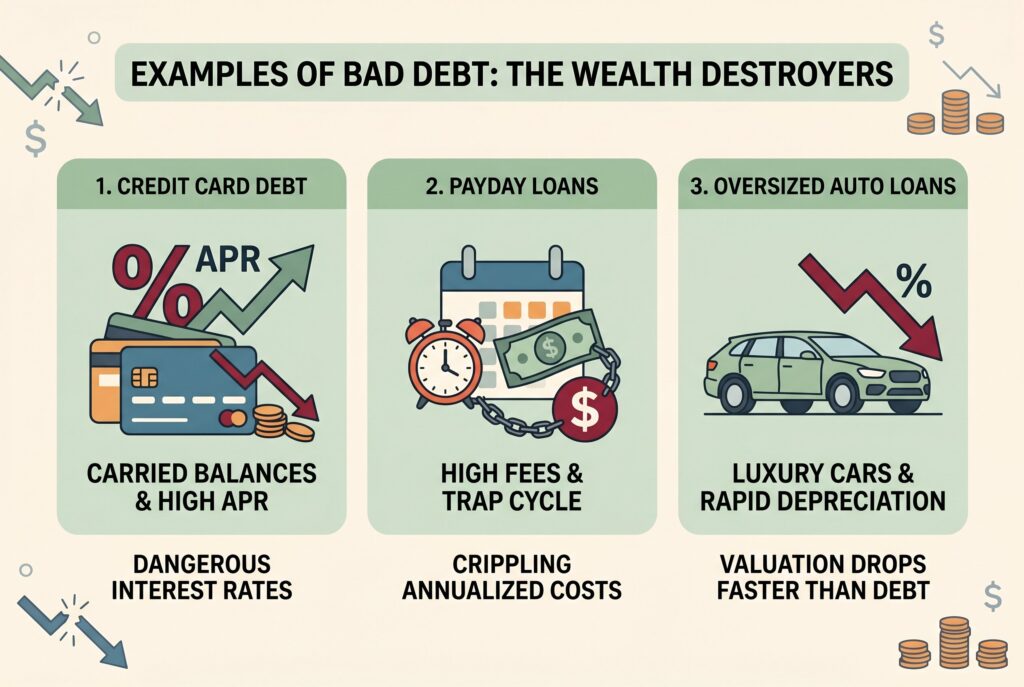

Examples of Bad Debt: The Wealth Destroyers

1. Credit Card Debt

Credit card debt is one of the clearest examples of bad debt when balances roll over month after month. With APRs often far above normal investment returns, interest can grow faster than your ability to repay. Using a credit card for rewards and paying it off in full can be fine. Carrying a balance for clothes, gadgets, travel, or dining out is different. The purchase may be gone, but the interest remains.

2. Payday Loans

Payday loans are dangerous because they often carry extremely high fees and annualized APRs. They can trap borrowers in a cycle where each paycheck is used to repay the last emergency. This type of high interest debt rarely builds value. It’s usually a sign that the household needs a cash flow reset, emergency fund, or safer borrowing alternative.

3. Oversized Auto Loans

A car loan isn’t always bad. Transportation can be necessary for work, family, and daily life. The problem starts when the loan is too large, the term is too long, or the car depreciates faster than the balance falls. Buying reliable transportation within your means is different from financing a luxury car that strains your budget. A vehicle usually loses value, so the loan should be practical and affordable.

The Gray Area: When Good Debt Turns Bad

No debt type is automatically good forever. The details decide. A mortgage can turn bad if you become house poor. That means the home payment leaves little room for saving, investing, repairs, insurance, or emergencies.

Student loan debt can turn bad if the degree doesn’t improve earning power enough to justify the cost. Business debt can turn bad if it’s used to hide cash flow problems rather than create profitable growth. Even low interest debt can become harmful if total payments overwhelm your monthly budget.

A useful rule is the 6% APR test. Debt below 6% may be manageable if the purpose is productive and payments fit your budget. Debt above 6% deserves closer attention because it begins competing with long term investment returns. Debt above credit card levels should usually be treated as urgent.

How to Measure Your Debt: The DTI Ratio

Don’t judge debt only by interest rate. Lenders also care about your debt to income ratio, or DTI ratio.

If your monthly debt payments are $2,000 and your gross monthly income is $6,000, your DTI is 33.3%.

As a general guide, below 36% is often healthy. Between 36% and 43% is a caution zone. Above 43% can be dangerous because too much income is already committed before food, utilities, insurance, savings, and emergencies. DTI doesn’t tell the whole story, but it’s one of the fastest ways to measure whether debt is helping or squeezing you.

Smart Debt Management Priorities

Start by listing every debt with balance, APR, minimum payment, and purpose. Then separate debts into three groups. High interest bad debt should be attacked first. This includes credit cards, payday loans, and personal loans with steep APRs. Productive but expensive debt should be reviewed. This may include private student loans, variable rate business loans, or auto loans that are too large. Low interest productive debt can usually be managed steadily while you build savings and invest. The goal isn’t to become debt free at any cost. The goal is to stop paying high interest on things that don’t build your future.

Conclusion

Good debt can help you buy a home, increase income, build a business, and grow net worth. Bad debt pulls money out of your future to pay for yesterday’s consumption. The difference isn’t just the loan type. It’s the APR, affordability, purpose, repayment plan, and expected return.

Use debt only when it supports a clear goal and fits your cash flow. Measure it with ROI, depreciation, APR, and DTI ratio. Pay down high interest debt aggressively, keep productive debt manageable, and remember that leverage works best when you’re in control.

Related Articles

- Debt Management Programs Explained: How They Work and When They’re the Smartest Debt Solution

- Debt Consolidation Explained: Key Benefits, How They Work, and When to Use Them

- How to Pay Off Debt Fast: 10 Proven Strategies to Regain Financial Freedom in 2026

- Debt Reduction Strategies: Smart Ways to Pay Off Debt Faster and Save Money

- Debt Settlement Explained: How It Works, Risks to Know, and Ways to Reduce Your Debt Faster

- Debt Refinancing Explained: How It Works, Benefits, Risks, and How to Make the Right Choice