: Unrealized Gains & Examples")

In addition to net income, companies also report comprehensive income to provide a broader view of their overall financial performance. Comprehensive income reflects not only the results of regular business operations but also certain gains and losses that affect shareholders’ equity. By presenting both net income and other comprehensive income, financial statements offer a more complete picture of changes in a company’s economic value during a reporting period.

Net Income vs OCI: Understanding the Realized Boundary

One of the biggest mistakes new accounting students, investors, and business owners make is assuming every gain or loss belongs on the income statement. Accounting standards draw a clear line between realized and unrealized results. Net income includes transactions that have been completed and recognized during the reporting period, such as product revenue, operating expenses, interest expense, taxes, and gains from assets that were actually sold. OCI works differently because it captures gains and losses that exist economically but haven’t yet become realized transactions.

Imagine a company owns a bond portfolio worth $10 million. If market interest rates rise and the portfolio loses $500,000 in market value, the company hasn’t necessarily sold those bonds. The loss exists on paper, but it remains unrealized. Instead of pushing that temporary market movement into operating profit, the loss may be reported through other comprehensive income. This is why comprehensive income vs net income matters so much. A company can report strong net income while also reporting large OCI losses that reduce total comprehensive income and shareholders’ equity.

Why Other Comprehensive Income Exists

Without OCI, financial statements would force companies into two imperfect choices. They could ignore unrealized gains and losses completely, which would make equity less connected to economic reality. Or they could send every market fluctuation through net income, which could make earnings extremely volatile and less useful for judging core operations. OCI solves this problem by giving certain unrealized gains, losses, expenses, and adjustments a separate reporting path.

This separate path matters because not every value change tells the same story. A currency translation loss from a foreign subsidiary doesn’t mean the company’s main product suddenly became less profitable. A pension adjustment doesn’t necessarily mean the current year’s operations collapsed. An unrealized loss on available for sale securities may reflect interest rate movements rather than poor management. OCI preserves that distinction. It keeps net income focused on realized performance while allowing comprehensive income to show a broader change in company value.

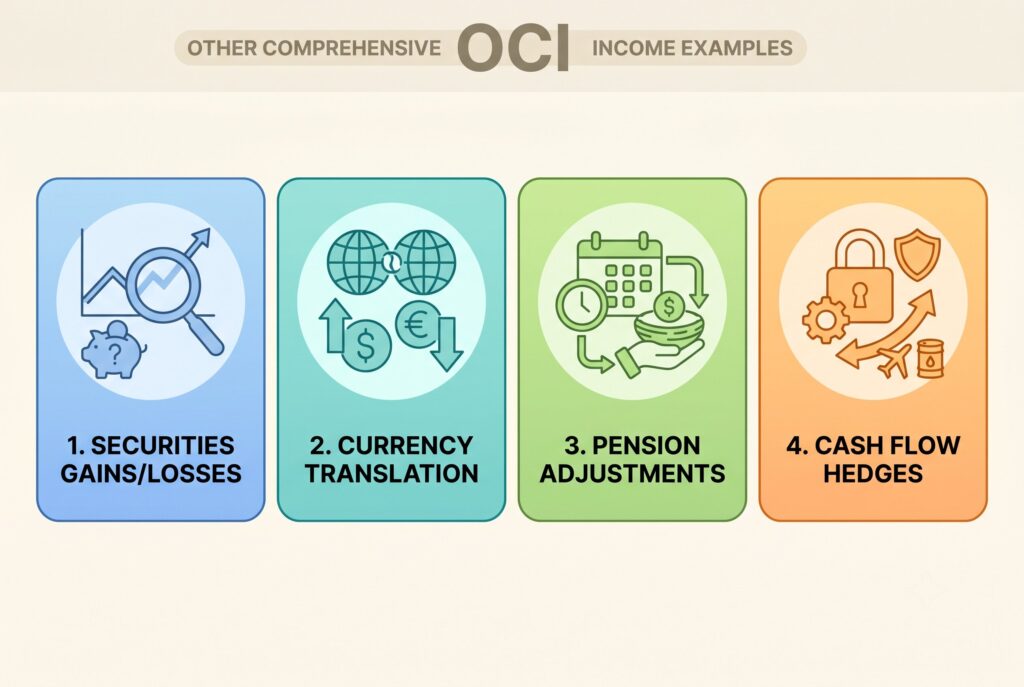

4 Classic Other Comprehensive Income Examples

1. Unrealized Gains and Losses on Securities

Unrealized gains and losses on certain investment securities are among the most common OCI examples. If a company holds securities that rise or fall in market value but hasn’t sold them, the gain or loss may be recognized through OCI instead of net income. This treatment is important because the company hasn’t converted the paper gain or loss into cash. The value change matters economically, but it isn’t yet a completed transaction.

This category is especially important for banks, insurers, and companies with large investment portfolios. A rising interest rate environment can create large unrealized losses on bond holdings, even while the company’s operating income looks healthy. Investors shouldn’t ignore these OCI movements because they may reveal balance sheet exposure that net income doesn’t show. At the same time, they shouldn’t automatically treat every unrealized loss as permanent damage. The right question is whether the company plans to sell the asset, whether the loss may reverse, and how large the exposure is relative to equity.

2. Foreign Currency Translation Adjustments

Foreign currency translation adjustments occur when a multinational company converts the financial statements of foreign subsidiaries into the reporting currency, such as U.S. dollars. Exchange rates constantly move, so the translated value of foreign assets, liabilities, revenue, and equity can change even when the underlying business is operating normally. Instead of allowing those currency movements to distort net income, many translation effects are reported through OCI.

For example, a U.S. company may own a profitable European subsidiary. If the euro weakens against the dollar, the translated value of that subsidiary may fall in U.S. dollar terms. That doesn’t necessarily mean the subsidiary sold fewer products or became operationally weaker. It may simply reflect currency movement. OCI helps separate that translation effect from core operating performance. For investors, persistent foreign currency translation losses can still matter because they reveal geographic exposure, but they need to be interpreted differently from falling sales or shrinking margins.

3. Pension Plan Adjustments

Pension plan adjustments are another major other comprehensive income example, especially for mature companies with defined benefit pension obligations. Pension accounting depends on assumptions about discount rates, expected asset returns, employee life expectancy, salary growth, and future benefit payments. When those assumptions change, the estimated pension obligation can rise or fall significantly.

These changes may not reflect current year operating performance, so many pension related gains and losses are reported through OCI. This prevents a single actuarial assumption change from overwhelming the income statement. However, investors should still pay attention. Large negative pension adjustments can signal long term obligations that may pressure future cash flow. OCI doesn’t make the risk disappear. It simply shows the risk in a different part of the financial statements. Analysts reviewing pension heavy companies should compare pension OCI movements with funding status, discount rate assumptions, and the size of shareholders’ equity.

4. Cash Flow Hedges

Cash flow hedges are used when companies want to reduce exposure to future changes in prices, interest rates, or exchange rates. Airlines may hedge fuel prices. Manufacturers may hedge commodity costs. Multinational companies may hedge foreign currency risk. When the effective portion of a hedge gains or loses value before the underlying transaction affects earnings, that unrealized hedge movement may be reported in OCI.

This treatment helps match the hedge result with the timing of the future cash flow it’s designed to protect. Without this approach, derivative gains and losses could create income statement noise before the related business transaction occurs. For example, if a company hedges a future purchase in euros, changes in the hedge value may first appear in OCI, then later move into earnings when the forecasted transaction occurs. For analysts, cash flow hedge OCI can provide insight into risk management quality and future margin protection.

OCI Accounting: Where Does OCI Appear?

OCI is usually presented in the statement of comprehensive income. The statement begins with net income, then lists each OCI component, calculates total OCI, and finally adds net income and OCI to arrive at comprehensive income.

A simplified statement might look like this:

Net Income: $500,000.

Unrealized Investment Loss: ($40,000).

Foreign Currency Translation Gain: $25,000.

Cash Flow Hedge Loss: ($10,000).

Total OCI: ($25,000).

Comprehensive Income: $475,000.

This structure helps readers see both realized performance and broader economic changes in one place. Net income still matters because it captures the company’s operating and realized financial results. But comprehensive income gives a wider view because it includes OCI items that affect equity. This is why investors, analysts, CPA candidates, and finance students shouldn’t treat OCI as a side note. It can explain why shareholders’ equity changed even when retained earnings and net income don’t tell the full story.

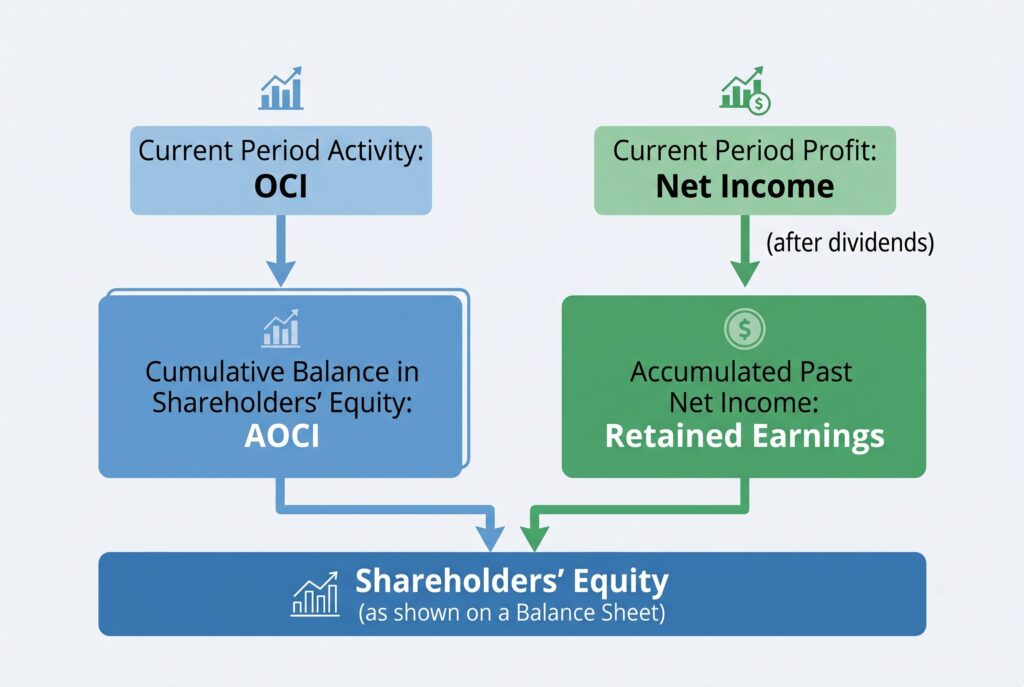

The Lifecycle: From OCI to AOCI

OCI is the current period activity, while accumulated other comprehensive income, or AOCI, is the cumulative balance sitting in shareholders’ equity. The easiest way to understand the relationship is to compare it with net income and retained earnings. Net income is the current period profit. Retained earnings accumulate past net income after dividends. OCI is the current period other comprehensive income. AOCI accumulates past OCI balances that haven’t been fully reclassified or settled.

This lifecycle matters because OCI doesn’t vanish after the statement of comprehensive income is prepared. It flows into AOCI on the balance sheet. That means OCI bypasses net income, but it doesn’t bypass equity. If a company records large negative OCI for several years, AOCI can become a major drag on shareholders’ equity. Conversely, positive OCI can increase equity even when those gains haven’t yet appeared in net income. Understanding AOCI helps investors see the long term accumulation of unrealized gains, translation effects, pension adjustments, and hedge movements.

Understanding Reclassification Adjustments

Some OCI items eventually move from AOCI into net income when they become realized. This process is called reclassification or recycling. For example, a company may record an unrealized gain on an investment through OCI while it still holds the security. If the company later sells that security, the gain is no longer unrealized. Depending on the accounting treatment, the amount may be reclassified from AOCI into net income as a realized gain.

Reclassification prevents double counting and helps connect the timing of recognition to the economic event. It also explains why analysts must be careful when reading OCI. Some OCI items are temporary parking places before an eventual income statement impact. Others may remain in equity for a long time. The important question isn’t only whether OCI is positive or negative. It’s whether the item may later affect earnings, whether it reflects temporary market movement, and whether it reveals a deeper risk.

Investor Interpretation: Is an OCI Loss a Red Flag?

An OCI loss isn’t automatically a red flag, but it should never be ignored. Many investors focus heavily on earnings per share and net income because those numbers are familiar. However, OCI can reveal risks that haven’t yet reached the income statement. A bank may report stable profits while holding large unrealized losses in its debt securities portfolio. An insurer may show strong underwriting results while its investment portfolio weakens. A multinational company may grow sales locally while translation losses reduce reported equity in U.S. dollar terms.

The right interpretation depends on the source of OCI. Unrealized bond losses may reflect interest rate risk. Foreign currency translation losses may reflect global exposure. Pension adjustments may point to long term benefit obligations. Cash flow hedge gains or losses may show how well management is protecting future cash flows. OCI is most useful when viewed with balance sheet size, capital ratios, liquidity needs, management’s holding period, and the likelihood of reclassification. It isn’t just accounting noise. In some cases, it’s the first place hidden economic pressure appears.

Conclusion

Other comprehensive income (OCI) is an important component of financial reporting because it captures unrealized gains and losses that affect shareholders’ equity without immediately impacting net income. Common OCI items include foreign currency translation adjustments, unrealized gains and losses on certain securities, pension adjustments, and cash flow hedges. By analyzing OCI alongside net income and comprehensive income, investors can gain a more complete understanding of a company’s financial performance and potential risks.