Comprehensive income provides a more complete view of a company’s financial performance than net income alone. By incorporating both operating results and certain changes in value that haven’t yet been realized, comprehensive income helps stakeholders better understand the overall impact of economic events on a company’s financial position. As a result, it serves as an important measure for evaluating changes in shareholders’ equity and assessing a company’s true financial performance over a reporting period.

What Is Comprehensive Income?

Comprehensive income is the broadest measure of a company’s income under US GAAP because it includes both net income and other comprehensive income. The formula is simple:

Comprehensive Income = Net Income + Other Comprehensive Income

The Core Difference: Comprehensive Income vs Net Income

The easiest way to understand comprehensive income vs net income is to focus on realized and unrealized changes.

Net income reflects what has already flowed through business performance. Revenue was earned, expenses were incurred, taxes were recorded, and gains or losses were recognized. It is the familiar bottom line of the income statement. Comprehensive income goes wider. It starts with net income, then adds other comprehensive income items that affect equity but aren’t yet part of regular profit and loss. For example, imagine a company reports $5 million in net income. During the same period, its foreign subsidiary loses $700,000 in value after translation into USD, and its available for sale securities rise by $300,000. The company’s OCI is negative $400,000. Comprehensive income becomes $4.6 million.

That difference matters. A company can look profitable on the income statement while unrealized market or currency losses quietly reduce shareholder equity.

Components of Comprehensive Income

Comprehensive income has two main components.

1. Net Income

Net income includes the results of normal business activity and recognized gains or losses. This includes sales revenue, cost of goods sold, operating expenses, interest expense, taxes, and other items reported through the income statement. Net income is important because it shows whether the company generated profit from its recognized business activities during the period.

2. Other Comprehensive Income

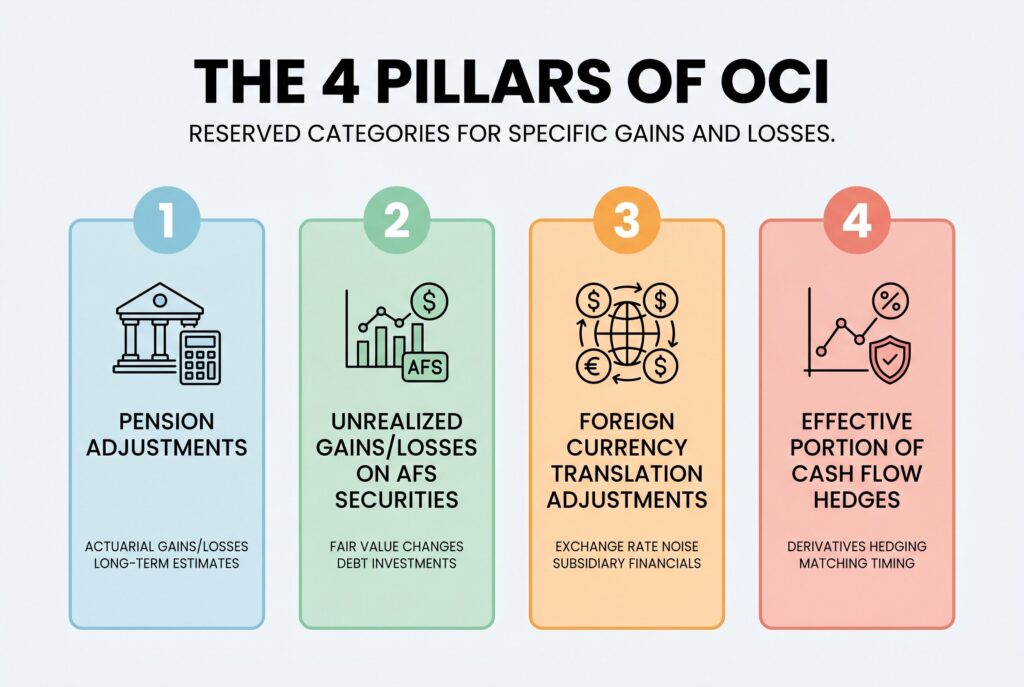

Other comprehensive income, often called OCI, includes certain gains and losses that US GAAP excludes from net income until specific conditions are met.

OCI isn’t a general category for any unusual item. It is limited to specific accounting items, such as:

- Foreign currency translation adjustments

- Unrealized gains and losses on certain debt securities

- Pension and postretirement benefit adjustments

- Effective portions of qualifying cash flow hedges

These items affect shareholders’ equity even though they do not immediately affect net income.

Comprehensive Income Statement Format

US GAAP allows companies to present comprehensive income in either a single continuous statement or in two separate statements. In a single continuous statement, the company presents revenue and expenses, calculates net income, and then continues with other comprehensive income items. The final line is total comprehensive income. In a two statement format, the company first presents a traditional income statement ending with net income. Then it presents a separate statement of comprehensive income that begins with net income and adds or subtracts OCI items.

A simple example may look like this:

| Item | Amount |

| Net Income | $5,000,000 |

| Foreign Currency Translation Loss | ($700,000) |

| Unrealized Gain on Available-for-Sale Securities | $300,000 |

| Pension Adjustment Loss | ($100,000) |

| Total Other Comprehensive Income | ($500,000) |

| Comprehensive Income | $4,500,000 |

This format helps readers understand how the company moved from net income to total comprehensive income.

Comprehensive Income and Shareholders’ Equity

Comprehensive income matters because it explains changes in shareholders’ equity that net income alone may not show. Net income usually closes into retained earnings. Other comprehensive income flows into accumulated other comprehensive income, or AOCI, which appears in the shareholders’ equity section of the balance sheet.

This means comprehensive income connects three important areas of the financial statements:

- The income statement

- The statement of comprehensive income

- The shareholders’ equity section of the balance sheet

For example, a company may report stable net income year after year, but if AOCI becomes increasingly negative, shareholders’ equity may still be under pressure. That pressure may come from currency losses, pension remeasurements, investment value changes, or hedge adjustments.

Why Comprehensive Income Matters for Investors

Comprehensive income provides a more complete picture of a company’s financial performance than net income alone. By including both net income and certain unrealized gains and losses that bypass the income statement, comprehensive income helps investors understand changes in shareholders’ equity that might otherwise go unnoticed.

For banks, insurers, investment firms, and multinational corporations, comprehensive income can be particularly important. Changes in investment portfolios, foreign currency translations, pension obligations, and hedging activities may significantly affect comprehensive income even when net income remains relatively stable. As a result, reviewing comprehensive income can give investors a deeper understanding of a company’s overall financial position and risk exposure.

This is why comprehensive income is useful for evaluating financial resilience. It shows whether shareholder equity is growing from both realized earnings and unrealized valuation changes. A healthy company shouldn’t be judged by one number. Net income explains operating performance. Comprehensive income explains the wider change in economic value.

Conclusion

A traditional income statement tells only part of the story. Net income shows realized profitability, but comprehensive income shows a broader picture of how equity changed during the period.

Because comprehensive income captures more than just earnings reported on the income statement, it provides a broader view of financial performance. Factors such as foreign currency movements, investment valuation changes, pension adjustments, and hedging activities can all impact comprehensive income and lead to meaningful changes in shareholders’ equity, even before those effects are reflected in net income.

For serious analysis, don’t stop at the bottom line of the income statement. Review OCI, AOCI, and total comprehensive income together. That fuller view helps you understand not only how much profit a company earned, but also how much hidden market, currency, pension, or hedge exposure may be moving underneath the surface.