Every organization faces risk when pursuing its business objectives, whether from cyber threats, operational disruptions, compliance failures, or strategic decisions. While security controls, policies, and mitigation measures can significantly reduce potential threats, no environment can be made completely risk-free. Some level of exposure will always remain, even after extensive efforts to identify, assess, and address vulnerabilities.

Understanding the level of risk that persists after safeguards are implemented is essential for effective risk management. This remaining exposure influences decision-making around security investments, compliance requirements, risk acceptance, and business continuity planning. By evaluating the risks that continue to exist after mitigation efforts, organizations can determine whether additional action is needed or whether the remaining exposure aligns with their risk tolerance and business objectives.

What Is Residual Risk?

Residual risk is the level of risk that continues to exist after controls are applied. It accepts a practical truth of risk management: no control removes risk completely. Even with strong cybersecurity controls, employee training, vendor due diligence, encryption, backups, insurance, and monitoring, some exposure remains.

In cybersecurity, residual risk may be a phishing email that still reaches an employee after filtering tools are installed. In vendor risk management, it may be the remaining chance that a third party suffers a breach after due diligence and contract protections. In business continuity, it may be the risk that recovery plans fail during a real disaster. This concept matters because leadership can’t make smart decisions from raw risk alone. They need to know what risk remains after real safeguards are in place.

The Residual Risk Formula: A Step by Step Guide

To understand how to calculate residual risk, start with the original exposure. This is usually called inherent risk. Then measure how much your controls reduce that exposure.

The simple formula is:

Residual Risk = Inherent Risk − Control Effectiveness

A more practical scoring method uses likelihood and impact:

Risk Score = Likelihood x Impact

For example, suppose a phishing attack has an inherent likelihood score of 5 and an inherent impact score of 4.

Inherent Risk Score = 5 x 4 = 20

Now assume your email filtering, employee awareness training, multi factor authentication, and incident response process reduce the risk by 75%.

Residual Risk = 20 x 25% = 5

The remaining score is 5. That doesn’t mean the threat disappeared. It means controls reduce the exposure from a high risk scenario to a lower one. For board reporting, this before and after comparison is powerful because it shows whether controls are actually reducing risk or only creating a false sense of safety.

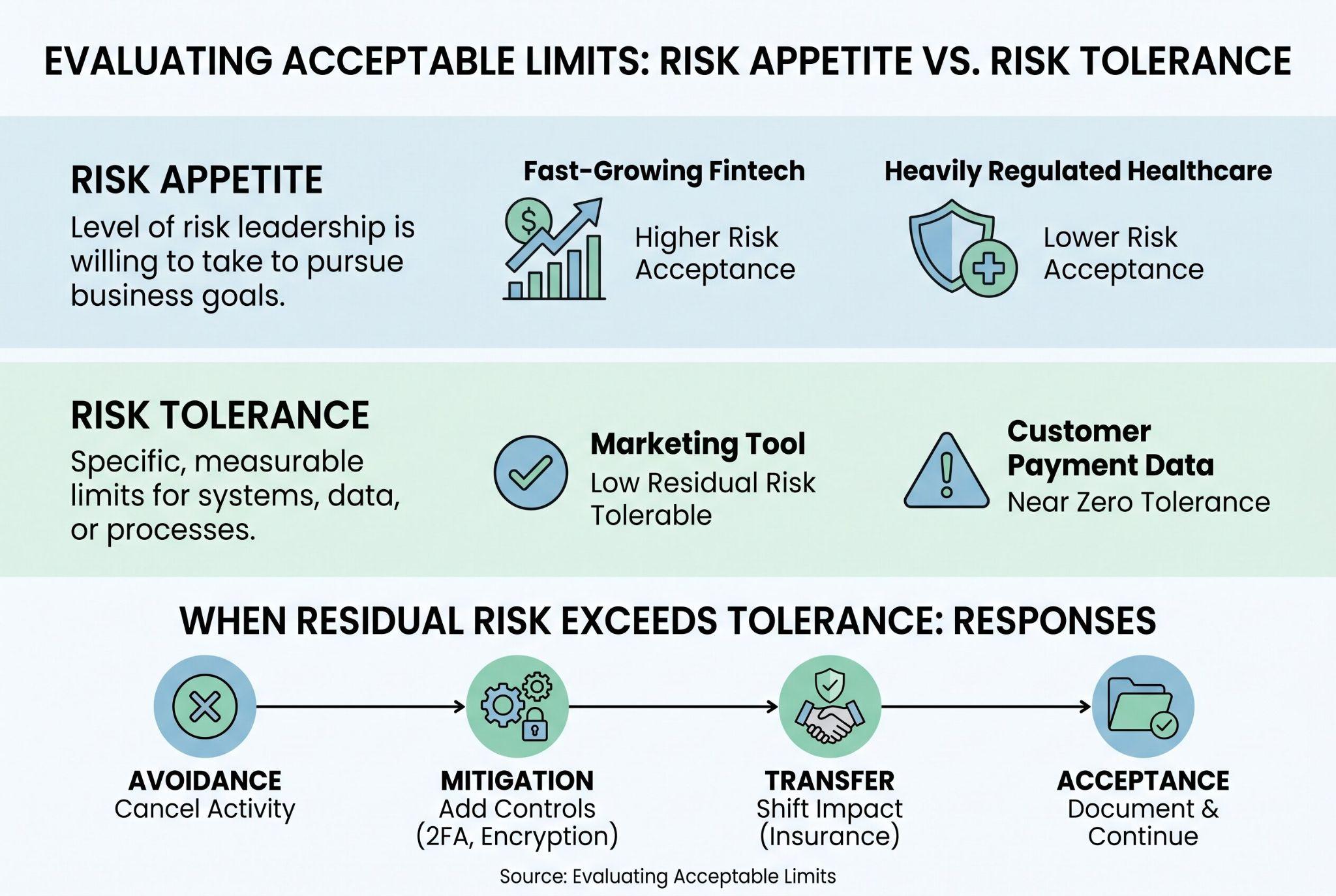

Evaluating Acceptable Limits: Risk Appetite vs. Risk Tolerance

Calculating residual risk is only half the process. The real decision is whether the remaining risk is acceptable.

Risk appetite is the level of risk leadership is willing to take in pursuit of business goals. A fast growing fintech company may accept more technology risk than a heavily regulated healthcare provider. Risk tolerance is more specific. It defines the measurable limit that a business unit, system, vendor, or process can’t exceed. For example, a company may accept low residual risk for a marketing tool, but it may require near zero tolerance for risks involving customer payment data, financial reporting, patient records, or critical infrastructure.

If residual risk sits below the approved tolerance, management may accept it and document it in a risk register. If it exceeds tolerance, the organization needs a response.

There are four common risk response options. Avoidance means canceling the risky activity, vendor, product, or system. Mitigation means adding more controls such as 2FA, encryption, monitoring, backups, or approval workflows. Transfer means shifting part of the impact through cyber insurance, contractual liability, or vendor indemnification. Acceptance means documenting the exposure and continuing because the cost of further reduction isn’t justified.

The Trap of Third Party Residual Risk

Third party residual risk is especially dangerous because it sits outside your direct control. You may secure your own systems well, but once a vendor receives data, processes transactions, hosts infrastructure, or connects to your network, your organization inherits part of that vendor’s risk profile.

A vendor may pass an onboarding questionnaire today and become risky six months later. Its financial condition may weaken. It may change subcontractors. It may suffer a security incident. It may fail to patch systems. It may expand access privileges without notifying your team.

This is why vendor risk management can’t stop at initial due diligence. Attack surface monitoring, updated security evidence, SOC reports, contract reviews, access recertification, and continuous monitoring are essential. A low risk vendor may only need basic annual review. A critical cloud provider, payment processor, payroll platform, or outsourced IT provider should receive deeper and more frequent residual risk assessment.

Residual Risk Examples Across Business Functions

Residual risk examples become easier to understand when viewed by function.

- In cybersecurity, a company may deploy endpoint protection, but malware can still bypass detection. The remaining exposure is residual risk.

- In compliance, a financial services company may train employees on anti money laundering rules, but human error or intentional misconduct can still occur.

- In operations, a manufacturer may have backup suppliers, but a regional disaster can still interrupt production.

- In business continuity, a recovery plan may meet its recovery time objective during testing, but real world conditions may delay restoration.

- In cloud computing, encryption and access control reduce exposure, but misconfiguration or compromised credentials can still create residual risk.

These examples show why residual risk management requires ongoing attention. A control that worked last year may not be strong enough against today’s threat environment.

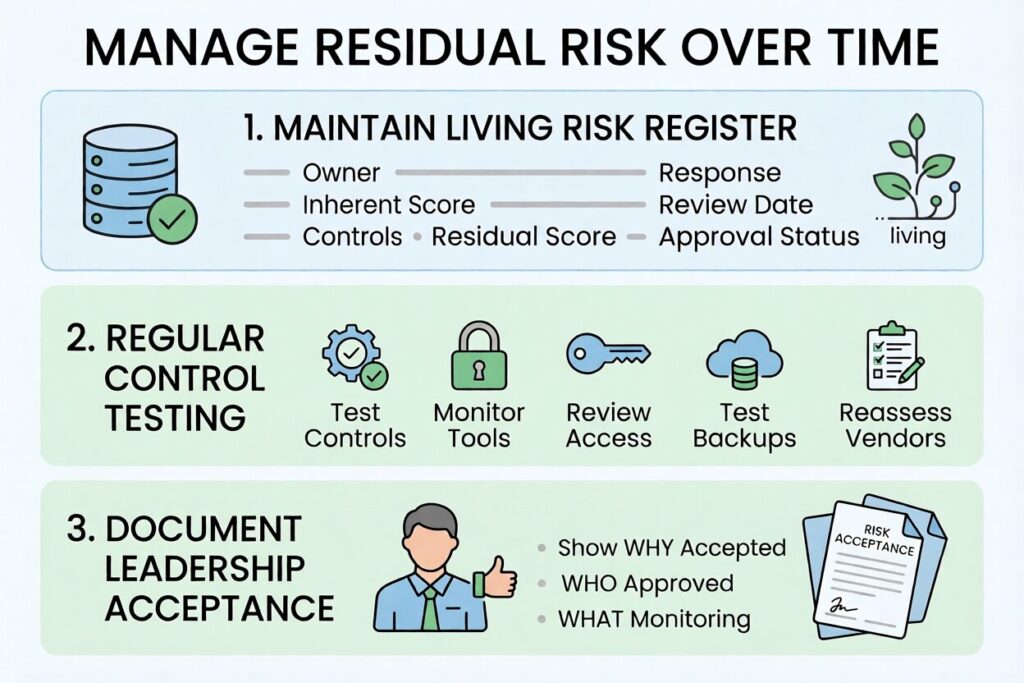

How to Manage Residual Risk Over Time

Residual risk isn’t static. Threats change, systems age, vendors evolve, employees make mistakes, and new regulations appear. A residual risk score that was acceptable last quarter may become unacceptable after a breach, audit finding, or infrastructure change. The best way to manage residual risk is to maintain a living risk register. Each risk should include the owner, inherent score, controls, residual score, risk response, review date, and approval status.

Control testing should also be regular. A policy isn’t a control unless it works in practice. Security tools should be monitored, access rights should be reviewed, backups should be tested, and vendors should be reassessed.

For compliance programs such as ISO 27001, documenting residual risk acceptance is especially important. Leadership should be able to show why a risk was accepted, who approved it, and what monitoring remains in place.

Conclusion

Residual risk is the honest answer to one of the most important questions in risk management: after everything we’ve done, what exposure still remains? A strong residual risk program doesn’t pretend risk can be reduced to zero. Instead, it measures the gap between inherent risk and the protection created by controls. Then it compares that remaining exposure against risk appetite, risk tolerance, and business value.

Residual risk should be monitored continuously as threats, systems, vendors, and regulations change over time. Regular reviews help organizations spot when risk levels rise and decide whether more controls, risk transfer, or leadership action is needed.