Your credit card balance is one of the most important numbers in personal finance because it directly affects how much you owe, how much interest you may be charged, and how quickly debt can grow. Whether you use a card for everyday purchases, emergencies, or recurring bills, understanding your balance helps you make smarter decisions and avoid costly mistakes.

What a Credit Card Balance Actually Means

A credit card balance is the total amount you currently owe on your credit card account. It includes purchases you’ve made, balance transfers, cash advances, interest charges, fees, and any unpaid amount carried over from earlier billing cycles.

Many cardholders assume the balance is just the amount they spent at stores or online, but that’s only part of the picture. If interest has been added or a late fee has posted, your total balance can rise even if you haven’t made any new purchases. That’s why reviewing your statement carefully matters.

It’s also important to know that a credit card account can show more than one balance at the same time. You may see a current balance, a statement balance, and sometimes a minimum payment due. These figures serve different purposes, and confusing them can lead to poor repayment decisions.

Current Balance vs. Statement Balance

One reason credit cards feel confusing is that the balance changes often. Your current balance is the amount you owe right now, including recent purchases, posted payments, fees, and interest. It updates as transactions move through the account.

Your statement balance is the amount listed on your billing statement at the end of a billing cycle. That number is especially important because paying the full statement balance by the due date is usually how cardholders avoid interest on purchases, assuming the account has a grace period and they haven’t carried a balance from before.

For example, suppose your statement closes with a balance of $800. After that date, you spend another $150. Your current balance may rise to $950, but your statement balance remains $800 until the next cycle closes. If you pay the $800 statement balance on time, you may avoid interest on that statement period’s purchases, even though the current balance shown online is higher. Understanding this distinction can help people budget more effectively and avoid paying either too little or more than necessary at the wrong time.

How a Credit Card Balance Turns Into Debt

A credit card balance becomes debt when it isn’t paid in full by the due date and begins carrying over from month to month. Once that happens, interest can start accumulating on the unpaid amount, making repayment more expensive.

This is where many people run into trouble. A balance that seems manageable at first can become harder to eliminate when interest keeps adding to what’s owed. If new purchases continue while old balances remain unpaid, debt can build faster than expected.

Carrying a balance doesn’t always mean someone is in a financial crisis. Sometimes people rely on credit cards during periods of tight cash flow, medical expenses, job changes, or unexpected repairs. Still, the longer a balance remains unpaid, the more likely it is to become a burden. That’s why understanding how balances grow is key to staying in control.

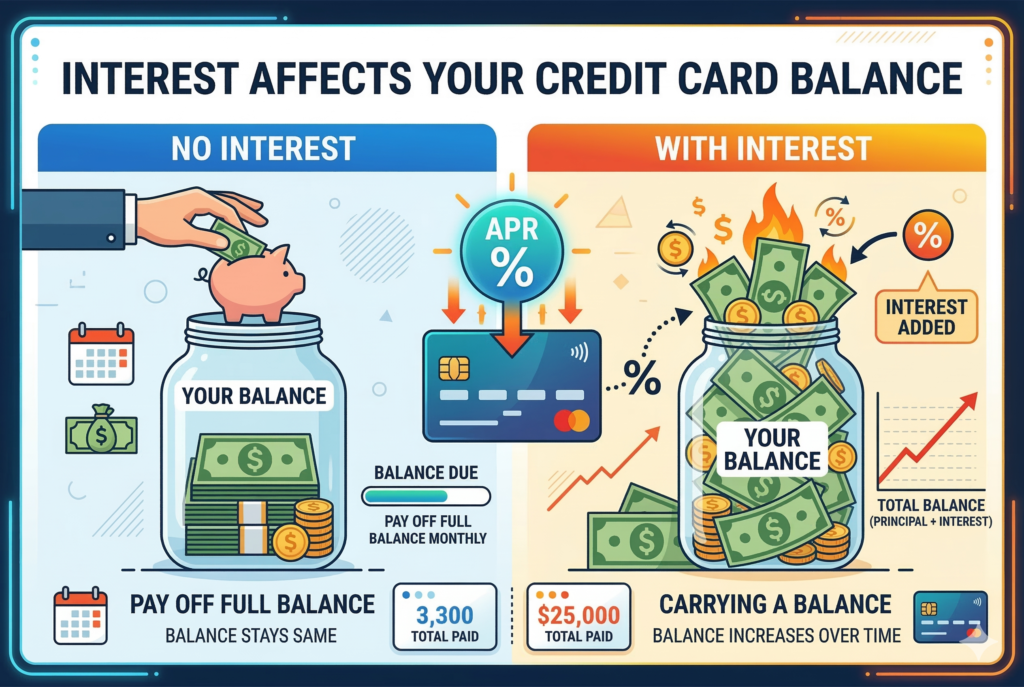

How Interest Affects Your Credit Card Balance

Interest is one of the biggest reasons a credit card balance can grow. If you don’t pay your statement balance in full, your card issuer may charge interest based on your APR, or annual percentage rate. Although APR is stated annually, interest is often calculated daily and applied over time.

That means even a modest unpaid balance can become more expensive than expected. If someone keeps carrying a balance while making only small payments, a larger portion of each payment may go toward interest rather than reducing the principal.

Cash advances can be even more expensive. Many cards charge a separate, often higher APR for cash advances, and interest may begin immediately without a grace period. Fees can also apply. Because of that, cash advances usually increase debt faster than regular purchases. Interest doesn’t just add cost. It also slows progress. A person who focuses only on making minimum payments may feel like they’re paying consistently, yet their balance may decline very slowly.

Why Your Balance Matters for Your Credit Score

Your credit card balance doesn’t only affect what you owe. It also plays a major role in your credit score, especially through credit utilization. Credit utilization is the percentage of your available credit that you’re using.

If you have a card with a $5,000 limit and a $2,500 balance, your utilization on that card is 50 percent. High utilization can signal greater borrowing risk to lenders, even if payments are made on time. Lower utilization generally supports a stronger credit profile.

This is one reason large balances can hurt financially in two ways at once. First, they may lead to more interest charges. Second, they can lower a credit score, which may affect future borrowing options, insurance pricing in some states, or the terms offered on loans and additional credit cards. Even people who never miss a payment can see score pressure if their reported balances are too high relative to their limits. That’s why balance management is important even for disciplined card users.

The Minimum Payment Trap

Every monthly statement includes a minimum payment, which is the smallest amount required to keep the account in good standing for that billing cycle. Paying at least that amount helps avoid late payment marks and penalty fees, but it’s rarely the best long-term strategy if you’re carrying debt. Minimum payments are often structured so they cover interest, fees, and only a small portion of the balance itself. As a result, debt can linger for years. The card remains active, but the borrower pays much more over time.

This structure can create a false sense of progress. Someone may feel they’re handling the account responsibly because they never miss a payment, yet the balance stays stubbornly high. In practical terms, minimum payments protect the account from immediate delinquency, but they don’t solve the underlying debt problem. Paying more than the minimum, even by a modest amount, can make a noticeable difference in how quickly the balance declines.

Common Reasons Credit Card Balances Keep Growing

For many households, rising credit card balances aren’t caused by one single mistake. More often, they grow because of a combination of habits and circumstances.

A common issue is using credit cards to cover routine expenses when income doesn’t fully cover monthly costs. Another is continuing to spend heavily while carrying an unpaid balance. Promotional offers can also create confusion. A low introductory rate may seem manageable, but once the promotion ends, interest charges can increase sharply.

Late fees, annual fees, and missed due dates can add to the problem. So can relying on multiple cards at once, which makes balances harder to track. In some cases, people simply don’t review statements closely enough and underestimate how quickly small charges accumulate. The good news is that understanding the cause of a growing balance is often the first step toward reversing it.

How to Manage Your Credit Card Balance More Effectively

Managing a credit card balance starts with consistency. The most effective approach is usually paying the full statement balance each month whenever possible. That keeps interest from building on purchases and helps prevent revolving debt.

If paying in full isn’t realistic, the next goal should be to pay as much above the minimum as your budget allows. It also helps to reduce new spending while working down existing balances. Otherwise, debt repayment becomes much harder.

Reviewing your statement every month is another smart habit. Look for interest charges, fees, subscription payments, and unusual transactions. Setting payment alerts and due date reminders can also reduce the risk of missed payments. For people dealing with larger balances, a structured repayment strategy can help. Some focus on paying off the highest-interest balance first, while others prefer eliminating the smallest balance for momentum. The best plan is the one that’s realistic enough to maintain month after month.

When a High Balance Becomes a Warning Sign

A high credit card balance becomes especially concerning when it keeps increasing despite regular payments, takes up too much of your monthly income, or forces you to depend on credit for basic necessities. Those signs may suggest the debt is no longer temporary and needs closer attention.

In that situation, it may be time to revisit your budget, pause discretionary spending, or explore lower-interest repayment options. The earlier someone addresses an unsustainable balance, the more choices they usually have. Waiting too long often leads to higher costs and fewer solutions.

Conclusion

A credit card balance is more than just a number on a statement. It reflects what you owe, influences how much interest you may pay, and affects your overall debt picture as well as your credit profile. When managed carefully, a credit card can be a useful financial tool. When balances are left to grow, they can become expensive and difficult to control. Understanding how your balance works is one of the most important steps toward reducing debt, protecting your credit, and making stronger everyday financial decisions.