A 15-year fixed-rate mortgage can be a powerful option for homebuyers and homeowners who want a shorter payoff timeline, a predictable interest rate, and lower total interest costs over the life of the loan. It isn’t the right fit for every budget, but for borrowers who can handle the higher monthly payment, it can offer meaningful long-term savings and faster equity growth.

Current 15-Year Fixed Mortgage Rates

Mortgage rates move constantly, so there’s no single number that applies to every borrower. As of March 12, 2026, Freddie Mac reported the national average for a 15-year fixed-rate mortgage at 5.50%, while the average 30-year fixed rate was 6.37%. Freddie Mac’s March 5 release showed the 15-year average at 5.43%, which reflects how quickly rates can shift from week to week.

That spread matters. A 15-year mortgage often carries a lower interest rate than a 30-year mortgage, which can reduce the total borrowing cost significantly over time. Still, the rate you’re offered depends on factors like credit score, down payment, loan size, debt-to-income ratio, property type, and whether you’re buying or refinancing. The CFPB also notes that mortgage pricing can vary based on the borrower’s profile and loan details, which is why rate shopping remains essential.

What a 15-Year Fixed-Rate Mortgage Means

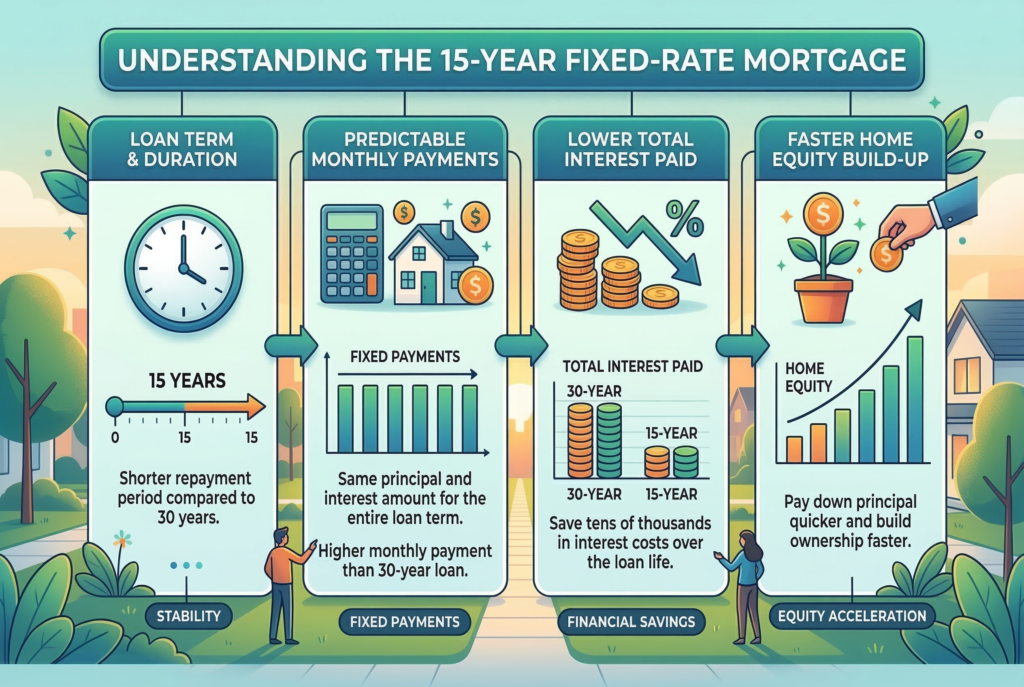

A 15-year fixed-rate mortgage is a home loan with a repayment term of 15 years and an interest rate that stays the same for the life of the loan. That fixed structure means the principal and interest portion of your monthly payment remains predictable, which can make long-term budgeting easier.

Compared with longer-term mortgages, this loan is designed to pay off the home much faster. Because the balance is repaid over half the time of a standard 30-year mortgage, each monthly payment usually includes a larger amount going toward principal. That accelerates debt reduction and builds home equity more quickly. The tradeoff is straightforward. Borrowers usually benefit from a lower rate and less total interest, but they commit to a higher monthly payment than they’d face with a longer repayment term.

Why This Loan Often Costs Less Over Time

One of the biggest reasons borrowers choose a 15-year fixed mortgage is the potential for long-term savings. There are two main reasons it can cost less overall.

First, shorter-term mortgages typically come with lower interest rates than 30-year loans. Freddie Mac’s recent surveys show that pattern clearly, with the 15-year average running below the 30-year average.

Second, you’re borrowing for fewer years. Even if the monthly payment is higher, you’re paying interest for a much shorter period. That combination can dramatically reduce the total amount paid over the life of the mortgage.

For buyers who want to minimize lifetime interest and become mortgage-free sooner, that can be a compelling advantage. A shorter term may also be attractive for homeowners refinancing from a 30-year loan if their income has increased and they want to speed up repayment.

Key Benefits of a 15-Year Fixed-Rate Mortgage

A major benefit is predictability. Because the rate stays fixed, borrowers don’t have to worry about payment shocks caused by changing interest rates. That stability can be especially valuable in a fluctuating rate environment.

Another benefit is faster equity building. Since more of each payment goes toward principal earlier in the repayment schedule, homeowners build ownership in the property at a quicker pace. That can improve financial flexibility later, whether the goal is selling, refinancing, or borrowing against equity.

There’s also the psychological and practical advantage of becoming debt-free sooner. Paying off a home in 15 years instead of 30 can free up substantial cash flow later in life. For some households, that lines up well with long-term goals like retirement planning, college funding, or reducing fixed monthly obligations.

The last major benefit is lower total interest cost. Even when the difference in rate looks modest, the shorter repayment period can translate into tens of thousands of dollars in savings over time, depending on the loan size.

The Main Drawback Borrowers Shouldn’t Ignore

The biggest challenge with a 15-year fixed-rate mortgage is the monthly payment. Because the same loan balance is being repaid over a shorter term, the payment is usually much higher than on a comparable 30-year mortgage.

That can strain a budget if income is tight, other debts are substantial, or household expenses are already high. A loan that looks efficient on paper can become stressful in real life if it leaves too little room for savings, repairs, childcare, healthcare, or emergencies.

This is where mortgage decisions need to be practical, not just mathematically appealing. A lower rate doesn’t automatically make the 15-year option the best choice. The right loan is the one that fits your cash flow comfortably, not just the one that pays off fastest.

When a 15-Year Fixed Mortgage Makes Sense

This type of loan often makes sense for borrowers with strong, stable income and enough budget flexibility to handle a larger monthly payment without sacrificing other financial priorities.

It can be a smart choice for buyers who are purchasing below their maximum budget, homeowners refinancing with the goal of paying off their loan faster, or borrowers nearing retirement who want to eliminate housing debt sooner. It may also suit households that already have solid emergency savings and manageable non-housing debt.

In many cases, the best candidate for a 15-year mortgage is someone who values certainty, wants to reduce interest costs, and doesn’t need the extra monthly breathing room that a 30-year loan provides.

When a 30-Year Loan May Be the Better Fit

A 15-year fixed-rate mortgage isn’t always the better move. A 30-year mortgage may be more appropriate for first-time buyers, households with variable income, or anyone who needs lower monthly payments to keep their budget resilient.

Lower required payments can create room for other priorities, such as retirement contributions, emergency savings, home maintenance, childcare costs, or paying down higher-interest debt. In some situations, preserving flexibility matters more than paying off the mortgage as quickly as possible.

That’s especially true if choosing a 15-year loan would leave you house-rich but cash-poor. The best mortgage should support your broader financial life, not crowd it out.

How to Compare 15-Year Fixed Mortgage Rates Wisely

When comparing offers, don’t focus only on the advertised rate. The CFPB recommends reviewing the full Loan Estimate, which helps borrowers compare interest rate, projected monthly payment, closing costs, and other loan terms across lenders.

It’s also smart to compare the APR, not just the note rate, because APR reflects certain fees and gives a broader view of borrowing cost. Looking at lender fees, discount points, and cash-to-close requirements can prevent surprises.

Even small differences matter on a mortgage. Shopping with multiple lenders can help borrowers find a structure that works better for their budget and long-term goals. The CFPB’s mortgage tools also emphasize that changing factors like credit score, down payment, and loan term can materially affect the rate a borrower receives.

Questions to Ask Before Choosing This Loan

Before committing to a 15-year fixed-rate mortgage, ask yourself whether the higher monthly payment still leaves room for retirement saving, emergency reserves, and routine living costs. It’s also worth thinking about job stability, future family expenses, and how long you expect to stay in the home.

Another useful question is whether you truly need the discipline of a 15-year term or whether a 30-year mortgage with optional extra principal payments would give you more flexibility. Some borrowers prefer the built-in structure of a shorter loan. Others want the lower required payment while still having the option to pay extra when cash flow allows.

Conclusion

A 15-year fixed-rate mortgage can be an excellent option for borrowers who want a lower interest rate, faster equity growth, and a shorter path to owning their home outright. Recent Freddie Mac data shows that 15-year rates remain lower than 30-year rates, which reinforces why this loan can reduce total interest costs over time. But the higher monthly payment is a serious tradeoff, and it won’t suit every household. For borrowers with steady income and enough room in the budget, this loan can make strong financial sense. For others, a longer term may provide the flexibility that keeps homeownership sustainable.