Plans Explained: How They Work, Tax Benefits, and Who Should Consider One")

Saving for retirement can look different depending on where you work, and that’s especially true for employees in schools, nonprofits, and certain public-sector organizations. A 403(b) plan is one of the main retirement savings tools available in those settings. For eligible workers, it can offer a practical way to invest for the future through payroll deductions, with meaningful tax advantages and the potential for long-term growth.

What Is a 403(b) Plan?

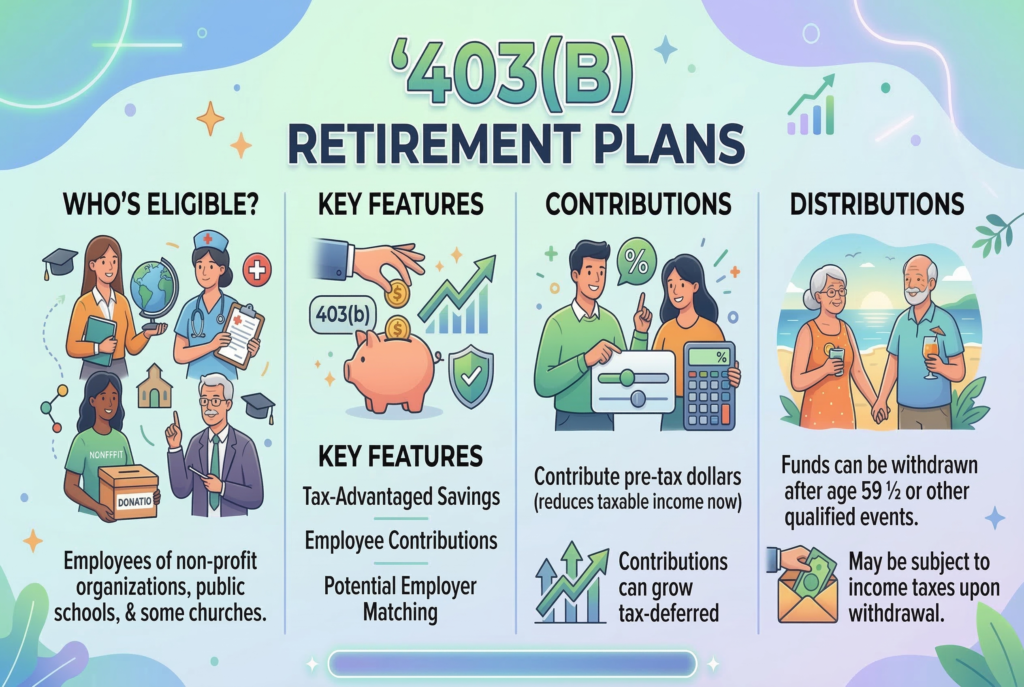

A 403(b) plan is an employer-sponsored retirement plan available to employees of public schools, certain nonprofit organizations, churches, and some tax-exempt institutions. In many ways, it functions similarly to a 401(k), but it’s designed for a different group of employers.

Employees who participate in a 403(b) can contribute part of each paycheck into the account. Those contributions are then invested in options offered through the plan, such as mutual funds or annuity contracts. Over time, the money can grow on a tax-advantaged basis until retirement.

For many workers, the biggest advantage is convenience. Contributions come directly from payroll, which can make retirement savings more consistent and easier to maintain. Instead of relying on manual transfers each month, the plan helps turn long-term saving into a regular habit.

How 403(b) Plans Work

A 403(b) plan works by allowing eligible employees to defer a portion of their salary into a retirement account. When you enroll, you select how much to contribute, usually as a percentage of your pay or a flat dollar amount. Your employer deducts that amount from your paycheck and deposits it into your 403(b) account.

In many plans, participants can choose between traditional contributions and Roth contributions, depending on what the employer offers. Traditional contributions are generally made before federal income taxes are applied, which may reduce your taxable income today. Roth contributions are made with after-tax dollars, so they don’t lower taxable income now, but qualified withdrawals in retirement can be tax-free.

The money inside the account is typically invested in a menu of plan options. Depending on the plan, these may include mutual funds, target-date funds, fixed or variable annuities, or other retirement-focused investments. Your returns depend on contribution levels, market performance, fees, and how long the money remains invested.

Some employers also contribute to the plan, either through matching contributions or fixed contributions. Not every 403(b) includes an employer match, but when it does, that can significantly improve long-term savings potential.

Tax Benefits of a 403(b) Plan

One of the main reasons people use a 403(b) retirement plan is the tax treatment. These accounts are built to support long-term retirement saving, and the tax advantages can make a major difference over time.

With traditional 403(b) contributions, money usually goes into the account before current federal income tax is applied. That can lower your taxable income for the year, which may reduce your immediate tax bill. The money then grows tax-deferred, meaning you generally won’t owe taxes on investment gains each year while the funds remain in the account. Taxes are usually due when you withdraw the money in retirement.

With Roth 403(b) contributions, the tax benefit comes later. Contributions are made after tax, so there’s no upfront deduction, but qualified withdrawals in retirement can be tax-free. This can be appealing for workers who expect to be in a higher tax bracket later or who want more flexibility in retirement income planning.

The long-term value of these tax benefits often becomes clearer in the long run. Consistent contributions, combined with years of tax-advantaged growth, can help participants build a larger retirement balance than they might through ordinary taxable investing alone.

403(b) Plans vs. 401(k) Plans

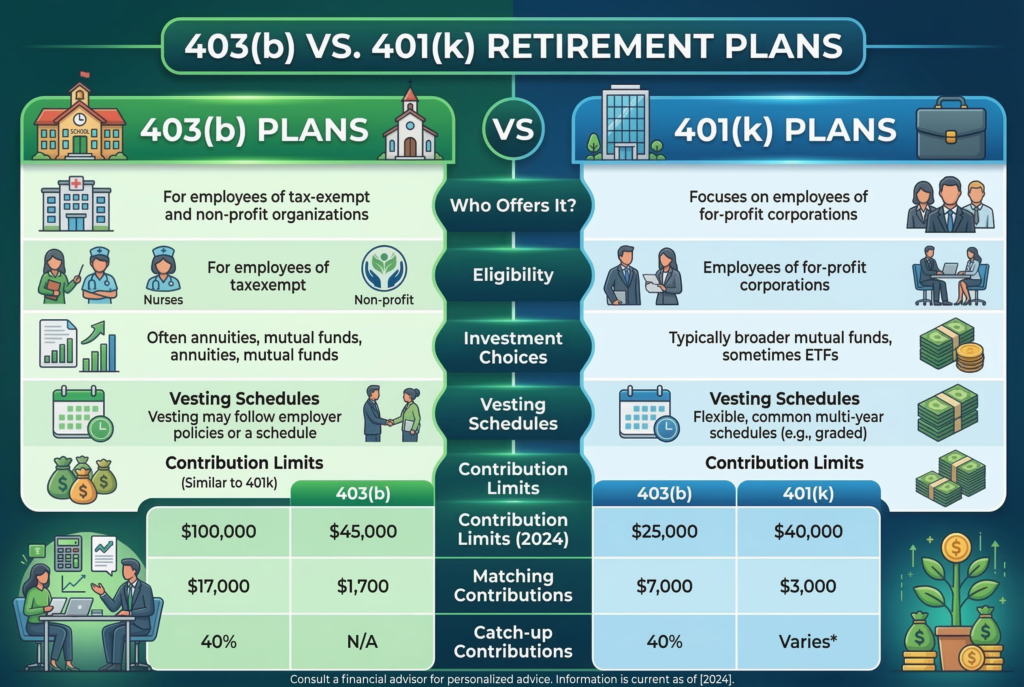

A 403(b) is often compared with a 401(k) because the two plans share many features. Both are workplace retirement plans that allow employees to contribute through payroll deductions. Both may offer traditional and Roth contributions. Both are intended to help workers save for retirement in a tax-advantaged way.

The biggest difference is the type of employer that offers the plan. A 401(k) is common in the private sector, while a 403(b) is typically offered by schools, nonprofits, and certain tax-exempt organizations.

Another difference may involve investment options and plan costs. Some 403(b) plans historically relied more heavily on annuity products, while many 401(k) plans are structured around mutual funds. That said, modern 403(b) plans vary widely, and many now offer diversified mutual fund menus and target-date options similar to those found in 401(k) plans.

From the employee’s perspective, the core retirement-saving function is often quite similar. The more important question is usually not whether the plan is a 403(b) or 401(k), but whether the plan has reasonable fees, strong investment options, and a contribution structure that fits your goals.

Key Benefits of a 403(b) Plan

A 403(b) can be a valuable retirement tool for eligible employees, especially when used consistently over time.

Automatic Payroll Contributions

Because contributions come directly from your paycheck, the plan makes saving easier and more consistent. This setup can help people invest regularly without having to think about moving money manually every month.

Tax-Advantaged Retirement Saving

The tax treatment is a major advantage. Whether you choose traditional or Roth contributions, the plan provides a more efficient structure for retirement investing than a standard taxable account.

Potential Employer Contributions

If your employer offers matching or supplemental contributions, that can increase your total retirement savings. Employer contributions can be especially valuable because they add to your account without requiring additional money from your paycheck.

Long-Term Growth Potential

A 403(b) is built for long-term investing. The earlier you start and the more consistently you contribute, the more time your investments have to compound.

Useful for Public Service and Nonprofit Employees

Workers in education, healthcare, and nonprofit roles may not always have access to the same compensation structure as private-sector employees. A 403(b) helps provide a dedicated retirement savings vehicle tailored to these workplaces.

Potential Drawbacks to Consider

A 403(b) plan can be useful, but it isn’t automatically perfect. Some plans have limited investment menus, and some may include high-cost annuity products or funds with relatively high expense ratios. Over time, those fees can reduce returns.

Another issue is that some employees enroll without fully understanding what they’re buying. A plan may offer good choices, weaker choices, or both. Reviewing the investment lineup matters. Workers should also pay attention to vesting rules if employer contributions are involved. Your own contributions are yours, but employer-funded amounts may require a certain number of years of service before they fully belong to you.

Early withdrawal rules are important too. Taking money out before retirement age can trigger taxes and possible penalties, depending on the circumstances. Because of that, a 403(b) works best when it’s treated as long-term retirement money rather than a flexible savings account.

Who Should Consider a 403(b) Plan?

A 403(b) may make sense for many eligible employees, especially those who want a simple and structured way to save for retirement through work. It can be a strong option for teachers, nonprofit professionals, healthcare employees at qualifying organizations, and others who want to contribute automatically from each paycheck. It may be especially attractive if the employer offers matching contributions or if the plan includes low-cost, diversified investment choices.

It can also work well for people who prefer a disciplined saving approach. Since the money is deducted from payroll, it may be easier to stay consistent than trying to save only when extra cash happens to be available.

Still, not every participant should contribute blindly. If your plan has high fees or poor investment choices, it may be worth balancing your strategy with other accounts, such as an IRA, depending on your income, eligibility, and retirement goals.

How to Get Started With a 403(b)

Starting with a 403(b) usually begins by reviewing your employer’s retirement plan materials. Look at eligibility rules, contribution options, employer contributions, available investments, and fees. If there’s an employer match, contributing enough to receive the full match is often a smart first step. After that, you can decide whether traditional or Roth contributions make more sense based on your tax situation and long-term goals.

It’s also important to review the investment menu carefully. Many participants choose a target-date fund for simplicity, while others prefer to build a mix of stock and bond funds themselves. The best choice depends on your comfort level, time horizon, and how much involvement you want in managing the account.

Conclusion

A 403(b) plan can be a powerful retirement savings tool for employees of schools, nonprofits, and other qualifying organizations. It offers payroll-based saving, important tax benefits, and the potential for long-term investment growth. For many eligible workers, it provides one of the most practical ways to build retirement security over time.

Still, the value of a 403(b) depends on how the plan is used. Contribution strategy, investment choices, fees, and employer support all matter. When you understand how your plan works and use it consistently, a 403(b) can become a strong foundation for long-term retirement planning.