State income tax can have a real impact on your paycheck, your annual tax return, and even where it makes financial sense to live or work. While federal income tax rules apply nationwide, state tax systems vary widely. Some states charge no broad individual income tax at all, others use a single flat rate, and many apply graduated tax brackets that rise with income. Understanding how state income tax works can help you estimate what you owe, plan more effectively, and look for legal ways to reduce your tax bill.

What State Income Tax Is

State income tax is a tax imposed by a state government on income earned by individuals, and in some cases by estates or trusts. Depending on where you live and where you work, it may apply to wages, self-employment income, investment income, retirement income, or a mix of those categories. Every state writes its own rules, which is why two people with the same income can owe very different amounts depending on location.

In practice, state income tax usually works alongside federal tax withholding. If you’re an employee, your employer may withhold state tax from each paycheck. If you’re self-employed or have income not covered by withholding, you may need to make estimated tax payments during the year. The IRS also notes that state and local income taxes paid may matter on your federal return if you itemize deductions, subject to IRS rules.

How State Income Tax Works

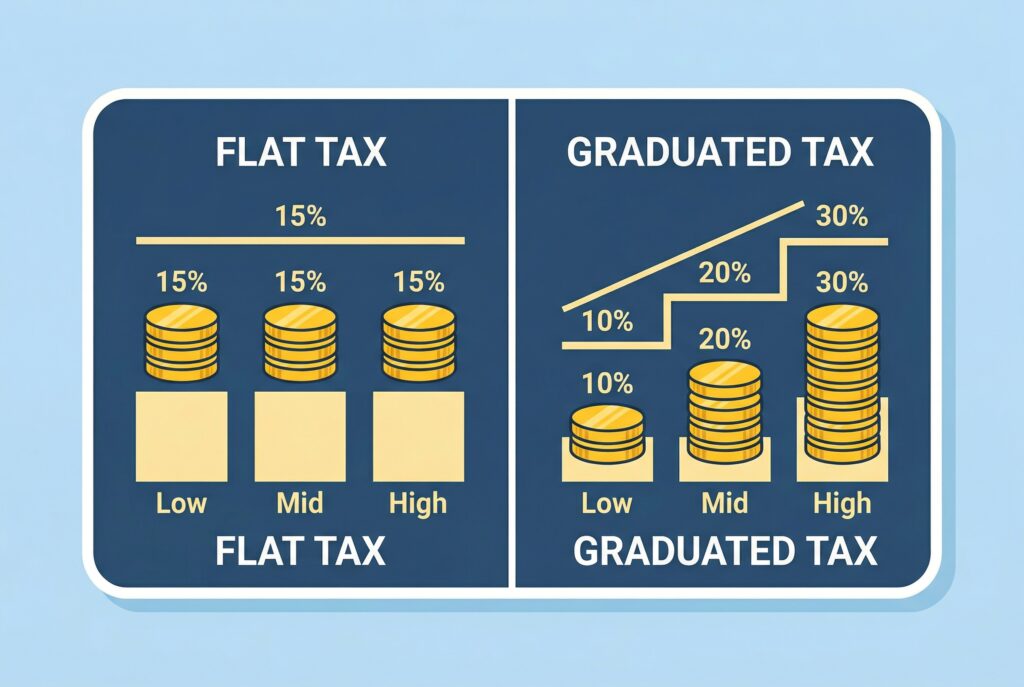

Most states that levy an income tax use one of two structures: flat tax or graduated tax. A flat-tax state applies one rate to taxable income, while a graduated-rate state applies higher rates as taxable income rises through brackets. Taxable income itself is usually based on your federal income as a starting point, then adjusted using state-specific deductions, exemptions, and credits.

That means your actual state tax bill depends on more than just the headline rate. Two states may appear similar on the surface, but one may offer a larger standard deduction, more generous dependent exemptions, or different treatment of retirement income. This is why comparing state income taxes requires looking at the full tax structure, not just the top bracket.

Rates by State Aren’t All the Same

As of 2026, states fall into three broad categories. Some have no broad individual income tax. Tax Foundation’s 2026 data shows Alaska, Florida, Nevada, South Dakota, Tennessee, Texas, and Wyoming in that group, while New Hampshire repealed its tax on interest and dividends effective January 1, 2025. Washington still doesn’t tax wage income, but it does impose a tax on certain long-term capital gains for high earners.

Other states use a flat income tax, meaning one rate generally applies to taxable income. Tax Foundation’s 2026 state map lists states such as Colorado, Illinois, Indiana, Kentucky, Massachusetts, Michigan, North Carolina, Pennsylvania, and Utah in the flat-tax category.

Many other states and the District of Columbia use graduated tax brackets, including California, New York, New Jersey, Oregon, Minnesota, and others. In these systems, higher slices of income are taxed at higher rates, which can make state tax planning more important as income rises.

Why Your State Tax Bill May Be Higher or Lower Than Expected

One reason people get surprised by state income tax is that residency and sourcing rules can get complicated. If you live in one state and work in another, you may have to file more than one state return depending on reciprocity agreements, residency rules, and whether tax was withheld in the right place.

This is especially relevant for commuters, remote workers, and people who moved during the year. State tax agencies and the Federation of Tax Administrators both maintain links to state departments and research resources because these rules differ substantially by state.

Another reason is that not all income is treated the same way everywhere. Some states offer exclusions for certain retirement income, pensions, or Social Security, while others tax more categories broadly. Investment income may also receive different treatment, especially in states with specialized rules like Washington’s capital gains tax.

Common Ways People Pay State Income Tax

For most workers, state income tax is paid through payroll withholding. The amount withheld may or may not match the amount actually owed when the return is filed, which is why some taxpayers get refunds and others owe money in April. The IRS recommends checking withholding periodically and adjusting forms when income, deductions, or life circumstances change.

People with side income, freelance income, capital gains, or rental income may also need to make estimated tax payments during the year. Waiting until filing season can lead to a larger bill and, in some cases, penalties. This matters for state taxes just as it does for federal taxes.

Ways to Lower What You Pay

Pre-tax Retirement Contributions

One of the most effective ways to reduce state taxable income is using pre-tax retirement contributions when your state follows federal treatment for those accounts. Contributions to a 401(k), 403(b), or traditional IRA may reduce taxable income in many situations, though each state has its own rules. This can lower both current taxes and overall taxable income on your return.

Health-related Tax Advantages

Health-related tax advantages can help too. In many cases, contributions to an HSA or certain flexible spending arrangements reduce taxable income, again depending on state conformity rules. These accounts won’t eliminate state tax everywhere, but they can be an efficient part of broader tax planning.

State-Specific Credits and Deductions

You should also pay close attention to state-specific credits and deductions. Many states offer credits for dependents, child care, property taxes, education expenses, low- to moderate-income households, or retirement income exclusions. Because these vary so much, checking your own state’s department of revenue site is often where the biggest savings opportunities appear.

Reciprocity Agreements and Nonresident Filing Rules

If you work in one state and live in another, reviewing reciprocity agreements and nonresident filing rules can also save money or prevent overpayment. Sometimes taxpayers end up overwithheld in the work state or miss a credit for taxes paid to another jurisdiction. Fixing that can reduce double taxation risk and improve cash flow.

Checking Withholding

Another practical strategy is checking your withholding during the year instead of waiting for tax season. If too much is withheld, you’re effectively giving the state an interest-free loan. If too little is withheld, you may face a painful bill later. Adjusting withholding to better match expected liability can make your tax situation more efficient.

Moving for Tax Reasons Isn’t Always Simple

People often look at states with no income tax and assume moving there will automatically save money. Sometimes it does, but not always. States still need revenue, so lower income taxes may be offset by higher sales taxes, property taxes, or other costs. Tax Foundation’s state tax resources emphasize looking at the broader tax structure rather than one number in isolation.

Residency also matters. You can’t usually avoid a state tax obligation just by spending more time elsewhere informally. States may examine where you live, work, vote, maintain a driver’s license, or keep your primary home. Anyone considering a move primarily for tax reasons should make sure the change is legally and financially real.

Mistakes to Avoid

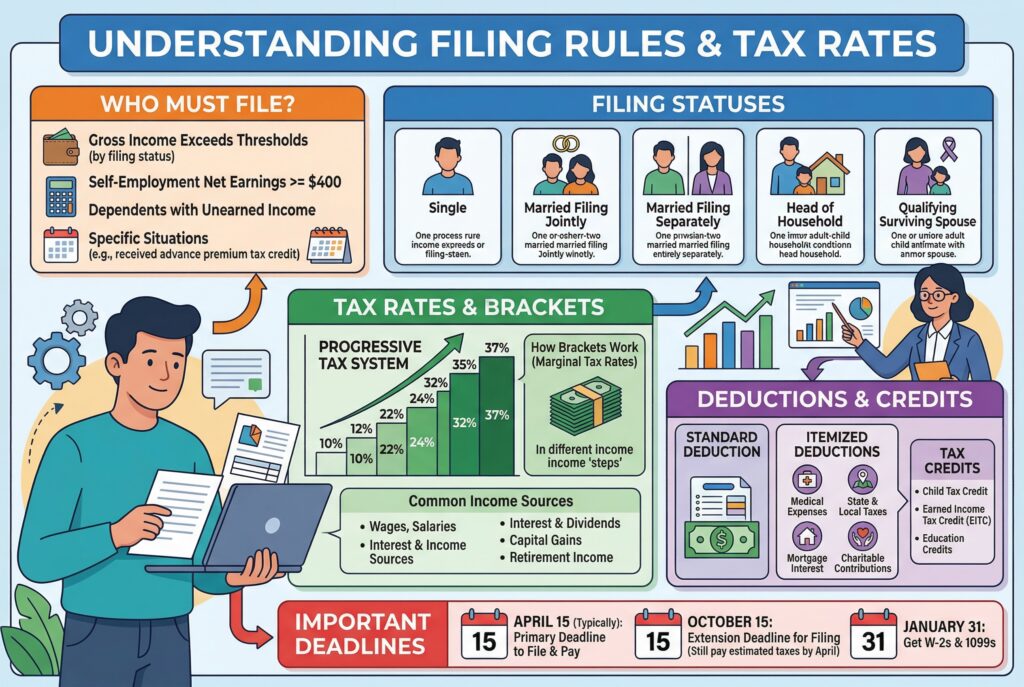

A common mistake is assuming the highest tax bracket applies to all of your income in a graduated-rate state. In reality, only the income that falls within each bracket is taxed at that bracket’s rate. That misunderstanding can make people overestimate what they owe.

Another mistake is focusing only on the tax rate and ignoring deductions, credits, and filing rules. A state with a lower headline rate may not always produce a lower tax bill if it offers fewer deductions or taxes more kinds of income. Likewise, forgetting about nonresident returns, estimated payments, or withholding adjustments can lead to avoidable costs.

Conclusion

State income tax can look simple on a paycheck stub, but in reality it’s shaped by where you live, where you work, how your state defines taxable income, and what deductions or credits you qualify for. Some states impose no broad individual income tax, others use flat rates, and many rely on graduated brackets. Those differences can materially affect your take-home pay and annual tax bill.

The best way to lower what you pay is usually a combination of smart withholding, careful filing, use of tax-advantaged accounts, and attention to state-specific deductions and credits. If you understand your own state’s rules and plan ahead, you’re much more likely to keep more of your money and avoid unpleasant surprises at tax time.