For a lot of Americans, debt isn’t just numbers on paper. It sticks with you in everyday life. You might be dealing with credit card balances, unpaid medical expenses, or student loans, all while trying to take care of yourself or your family. Some months, no matter how hard you try to pay it off, the debt barely budges.

Have you ever thought, “Why can’t I seem to make progress?” or “How can I move forward faster?” If you have, the debt snowball method could be just what you’ve been looking for.

Below, you’ll find out how this method works, why it’s so successful, the reasoning behind its approach, real-life examples, pitfalls people often face, and tools to help you stick with it. This version also highlights trends and insights for 2024–2025 to give you up-to-date and practical advice.

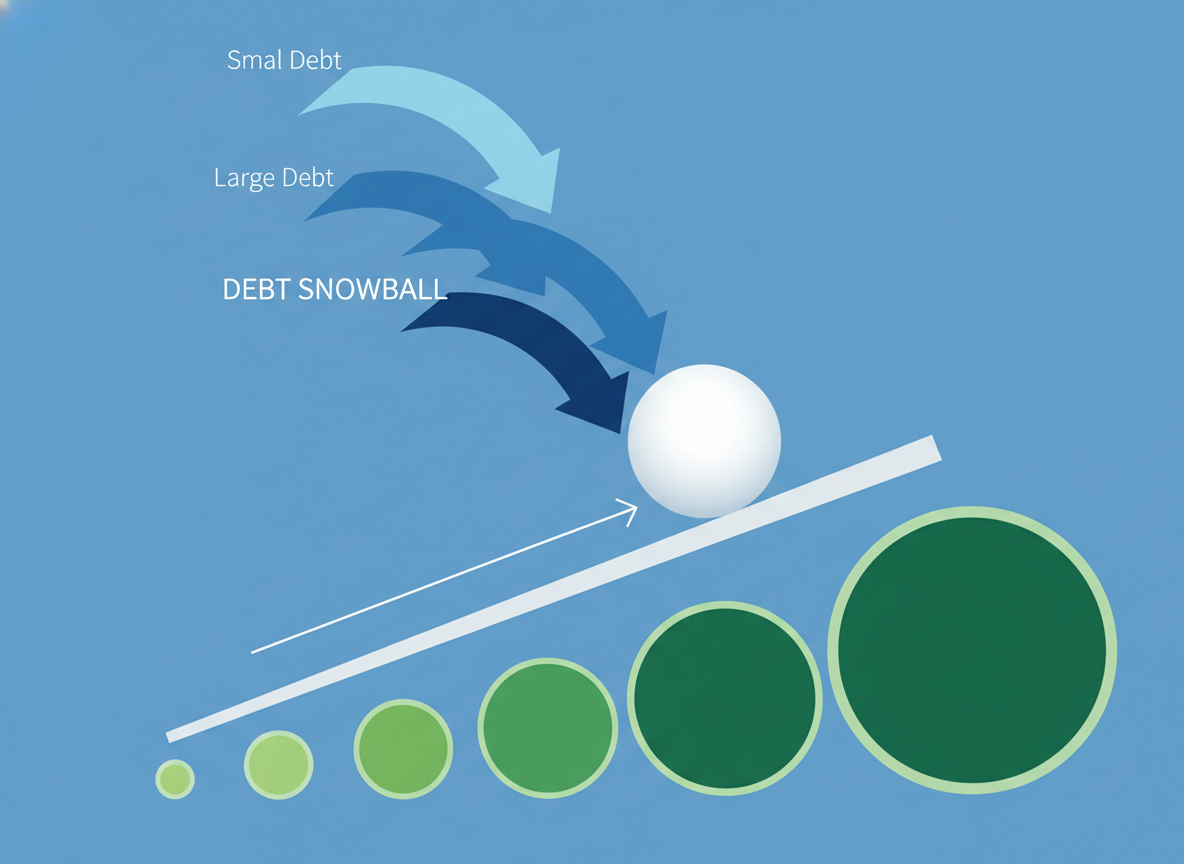

What Is the Debt Snowball Method?

The debt snowball method helps you pay your debts from the smallest balance up to the largest, without worrying about the interest rates. By clearing out the smallest debt first, you can gain confidence and pick up speed much like a snowball growing as it rolls downhill.

This method doesn’t rely on interest calculations. It focuses on real human habits and emotions. Knocking out small debts gives quick victories. These wins keep you moving forward, which is essential to clearing all your debt.

Why the Debt Snowball Method Works (Psychology Explains)

The problem for most people isn’t math. It’s things like staying motivated, feeling overwhelmed, getting stuck from too many choices, or getting worn out.

Behavioral finance research shows that:

1. Small wins build momentum

Clearing even one small debt shows your brain that you can succeed. That feeling of achievement makes it more likely you’ll keep going.

2. Fewer accounts bring less stress

Paying off a debt means fewer bills to manage, fewer deadlines to track, and one less worry on your plate.

3. The snowball method beats frustration

Many people quit debt payoff plans because they don’t see progress fast enough. The snowball approach gives you quick wins that keep you motivated.

4. Real-world success needs motivation, not just math

An ideal plan on paper won’t matter if you abandon it. A plan that keeps you inspired and consistent will always perform better.

Step-by-Step Guide to Using the Debt Snowball Method

Step 1: Organize Debts from Small to Big

Leave out your home loan. Focus on credit cards, medical expenses, personal loans, student loans, and car loans. Don’t bother with interest rates now. This approach builds momentum.

Step 2: Pay Minimums on All Debts Except the Smallest

Paying minimums prevents fees and protects your credit score while you tackle the smallest amount first.

Step 3: Put Every Spare Dollar Toward Your Smallest Debt

Even adding an extra $20 or $50 toward your payments can make a meaningful difference and help maintain momentum. That extra money might come from temporarily cutting a small expense, earning a bit through a side gig, selling unused items, or putting a tax refund or bonus toward your debt.

Step 4: After Paying Off the Smallest Debt, Add That Payment to the Next One

This step is what triggers the snowball effect. For example, if you’ve been paying $50 toward Debt 1 and $30 toward Debt 2, once Debt 1 is paid off, you redirect that $50 to Debt 2, boosting its payment to $80 and accelerating progress.

Step 5: Keep Going Until You’re Free From Debt

Each win boosts your confidence, builds emotional strength, and increases how much you can pay.

Example: How the Debt Snowball Plan Works in Real Life

Here’s a common debt situation:

| Debt | Balance | Minimum payment |

|---|---|---|

| Credit card A | $500 | $50 |

| Credit card B | $2,500 | $63 |

| Auto loan | $7,000 | $135 |

| Student loan | $10,000 | $96 |

Things to Keep in Mind

The snowball method can be effective, but it isn’t perfect. Because it doesn’t prioritize the highest-interest balances first, you may end up paying more interest over time compared to the avalanche method. It’s also not always ideal for debts with extremely high interest rates, where a blended or alternative approach may work better. And like any payoff strategy, it requires real habit changes, such as sticking to a budget, staying consistent, and making temporary cutbacks to keep progress on track.

How to Decide if the Debt Snowball Works for You

This method works well when you:

- Feel stressed managing several debts

- Need small wins to keep pushing ahead

- Have tried other ways but gave up midway

- Like simple actions better than complex plans

- Get discouraged when progress feels slow

It might not suit you if:

- Your debt carries high interest, like 20% or more.

- You analyze a lot and get motivated by saving more over time.

- You choose the plan with the lowest cost.

Debt Snowball vs. Debt Avalanche vs. Hybrid: A Quick Look

| Method | What it focuses on | Ideal for | Advantages | Disadvantages |

|---|---|---|---|---|

| Snowball | Paying the smallest debt first | People who need encouragement | Quick results, easy to follow | Adds more interest in the end |

| Avalanche | Paying the highest interest debt first | Those who think mathematically | Saves the most money on interest | Takes time for progress to show |

| Hybrid (Smart Snowball) | Combining small debts with high-interest ones | People who want a balance | Gets both motivation and reduced interest | Takes extra effort to plan |

Today’s Trends: Why Snowball Is Back in Style Again

People today value simplicity and steady progress. In 2024–2025, the snowball method has become more relevant than ever because credit card APRs are sitting at record highs, often between 20–30% or more, making small wins feel urgently motivating.

At the same time, the rise of buy-now-pay-later services has left many people juggling multiple small balances, which fits naturally with a snowball-style approach. Modern budgeting tools like YNAB, Rocket Money, and Undebt.it further simplify tracking, making consistent progress easier to maintain.

Mistakes That You Should Avoid

Common mistakes can slow or even undo your progress if you aren’t careful. Skipping a starter emergency fund leaves you vulnerable to surprise expenses that can force you back into borrowing. Continuing to use credit cards while paying off debt works against you, and spreading extra payments across multiple debts can dilute momentum and motivation. Finally, failing to track your progress visually can make the journey feel harder than it is, since seeing wins clearly helps keep motivation strong.

Final Thoughts: The Debt Snowball Can Transform Your Finances

Debt might seem overwhelming at first, but using the debt snowball method lets you take manageable steps forward starting now. You don’t have to be perfect, have fancy tools, or understand everything about finances. You need simple victories, regular effort, and a plan you can follow. Using the snowball method, you do more than just tackle debt, you change how you see and handle money along the way.