Managing multiple debts can be overwhelming. From credit card bills to medical expenses and student loans, the weight of different payments each month can make it difficult to keep track of everything. For many individuals facing high-interest debt, debt consolidation offers a potential solution to simplify things and reduce financial stress. This process allows you to combine several outstanding debts into a single loan, ideally with a lower interest rate, making it easier to manage payments and potentially save money. But what exactly is debt consolidation, and when should you consider using it? In this article, we’ll explain everything you need to know about debt consolidation, how it works, its key benefits, potential risks, and how it can help you regain control of your finances.

What Is Debt Consolidation?

Debt consolidation is a financial strategy used to combine multiple debts, such as credit cards, personal loans, and medical bills, into one loan. The main goal of debt consolidation is to simplify your payments by combining them into one manageable monthly installment. This process often involves taking out a new loan that pays off your existing debts. The new loan may offer a lower interest rate than what you were paying on your previous accounts, which could help you save money over time. Instead of making multiple payments to different creditors, you would only make one payment to the lender of your consolidation loan.

Debt consolidation can be done in a variety of ways. Some of the most common methods include applying for a personal loan, transferring your balance to a 0% APR credit card, or using a home equity loan or home equity line of credit (HELOC). Each method has its own advantages, depending on the size of the debt, your credit score, and the terms of the loan.

How Does Debt Consolidation Work?

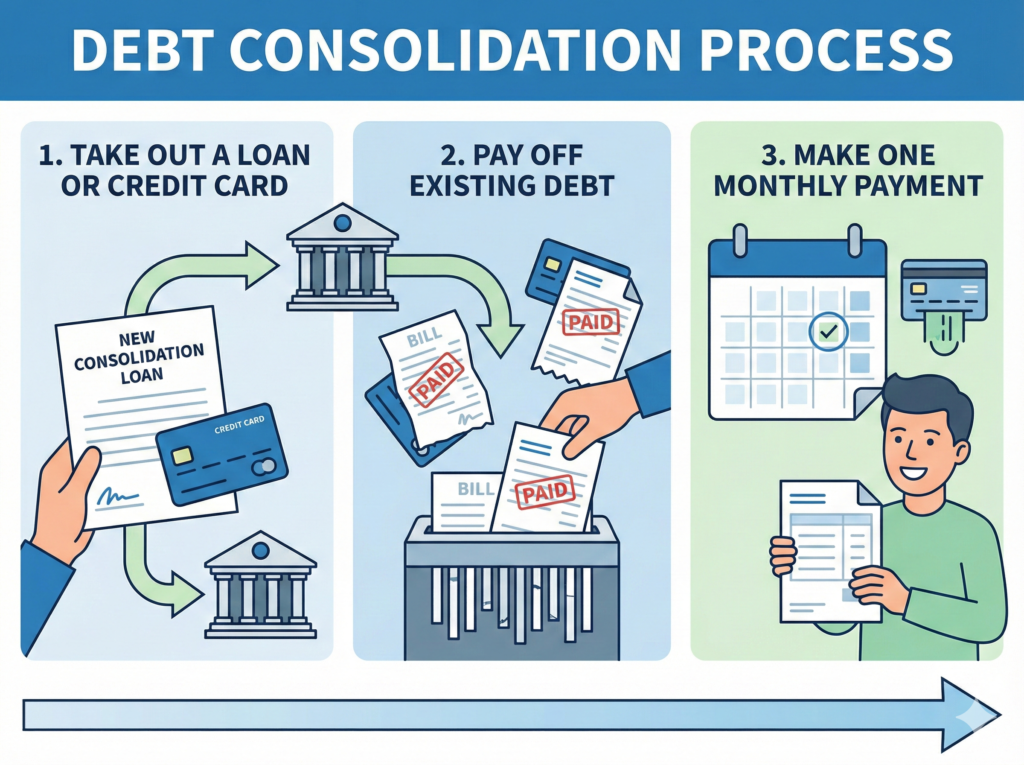

Here’s a simple breakdown of how the debt consolidation process works:

- Take out a loan or credit card: You apply for a personal loan, balance transfer card, or home equity loan to pay off your existing debts.

- Pay off existing debt: Once you’re approved, the new loan or credit line is used to pay off your current outstanding debts. This could be credit card balances, medical bills, or other unsecured loans.

- Make one monthly payment: Going forward, you’ll only need to make one monthly payment to the lender or credit card company that holds your consolidation loan, instead of several payments to multiple creditors.

Example of Debt Consolidation

Imagine you have three credit cards with balances of $3,000, $2,500, and $1,500, each with varying interest rates. Instead of paying multiple creditors, you decide to consolidate these balances into a single personal loan with a lower interest rate, say 8%, compared to the higher rates you were paying on the credit cards, which could range from 15% to 25%.

By consolidating, you’re reducing the amount of interest you pay on your total debt over time, and you only need to manage one monthly payment, making it easier to stay organized and on top of your finances.

Key Benefits of Debt Consolidation

Debt consolidation offers several potential benefits, making it an attractive option for people who struggle with multiple debts. First, consolidating your debts can help you simplify your finances by merging several monthly payments into one. This can reduce the likelihood of missing payments and help you stay organized. It’s much easier to manage one loan than to keep track of multiple payments with varying due dates.

Another significant benefit is the potential to lower your interest rates. If you qualify for a debt consolidation loan with a lower rate than what you were previously paying, you can save money on interest over time. For example, if you were paying 18% APR on a credit card and could consolidate it with a loan offering 10% APR, the difference in interest charges could make a noticeable impact on your overall financial health.

Debt consolidation can also help improve your credit score over time. When you consolidate debt, your credit utilization ratio (the ratio of your total credit balances to your available credit) can improve, which is a key factor in determining your credit score. By consolidating credit card debt and reducing your balances, you may be able to boost your credit score as you pay down the loan.

When Is Debt Consolidation a Good Idea?

Debt consolidation can be an effective tool for managing debt, but it isn’t the right choice for everyone. It’s ideal if you’re dealing with high-interest debt, such as credit card balances or payday loans, and you can qualify for a loan with a lower interest rate. If you’re struggling with multiple payments and find it hard to stay on top of due dates, consolidating your debt into a single payment can offer relief and prevent late fees.

Another situation where debt consolidation makes sense is if you have a steady income and can commit to the monthly payments required by the consolidation loan. If you’re facing a large amount of debt, consolidation can make it easier to pay it off in an organized and systematic way.

However, if you aren’t able to reduce your interest rates or if you continue to accumulate more debt after consolidation, it could end up making your financial situation worse. Before consolidating, it’s essential to assess your spending habits and ensure you’re committed to paying down the debt rather than adding more.

Risks of Debt Consolidation

The Extended Loan Term

One potential downside of consolidating your debt is that it may extend the repayment term. While this could lower your monthly payment, it may result in paying more interest over time, depending on the loan terms.

Fees and Costs

Some methods of debt consolidation, such as balance transfer credit cards or home equity loans, come with fees. It’s essential to weigh these costs against the potential savings.

Risk of More Debt

Debt consolidation can be a great strategy for paying down debt, but it’s only effective if you avoid accumulating more debt afterward. If you consolidate your credit card balances but continue to run up new charges, you may find yourself in a worse financial situation.

Secured vs. Unsecured Loans

If you consolidate debt using a home equity loan or HELOC (Home Equity Line of Credit), you’re using your home as collateral. This means if you fail to repay the loan, your home could be at risk. On the other hand, unsecured loans don’t require collateral, but may have higher interest rates.

Alternatives to Debt Consolidation

Debt Management Plans (DMPs)

A DMP involves working with a credit counseling agency to negotiate with creditors and reduce interest rates on your existing debt. Unlike debt consolidation, DMPs don’t involve taking out a new loan but can still help reduce your payments.

Debt Settlement

In debt settlement, you work with a company to negotiate with creditors to settle your debt for less than what you owe. However, this can have a negative impact on your credit score and may result in taxable income.

Bankruptcy

If you’re unable to pay off your debt, bankruptcy may be an option. This is a last-resort solution that provides relief but comes with long-term consequences for your credit.

Conclusion: Is Debt Consolidation Right for You?

Debt consolidation is an effective strategy for individuals struggling with high-interest debt and looking to simplify their payments. By consolidating your debts, you can lower your interest rates, reduce the number of monthly payments, and potentially improve your credit score. However, it’s essential to weigh the benefits against the risks and consider alternatives, such as debt management plans or debt settlement, before making a decision.

If you’re considering debt consolidation, be sure to choose the option that works best for your financial situation and future goals. With a clear plan and commitment to paying down debt, consolidation can be a powerful tool for achieving financial freedom.

Related Articles

Debt Management Programs Explained: How They Work and When They’re the Smartest Debt Solution