When planning for your child’s future, choosing the right savings account can make a world of difference. Two common options for parents are UGMA (Uniform Gifts to Minors Act) and UTMA (Uniform Transfers to Minors Act) accounts. Both allow you to save on behalf of your child while giving them access to those funds once they reach the legal age of adulthood, but how do you decide which one is right for you?

In this article, we’ll dive into the ins and outs of both accounts, their key differences, benefits, and drawbacks, and provide you with practical advice on how to choose the best account for your family’s savings goals.

What Are UGMA and UTMA Accounts?

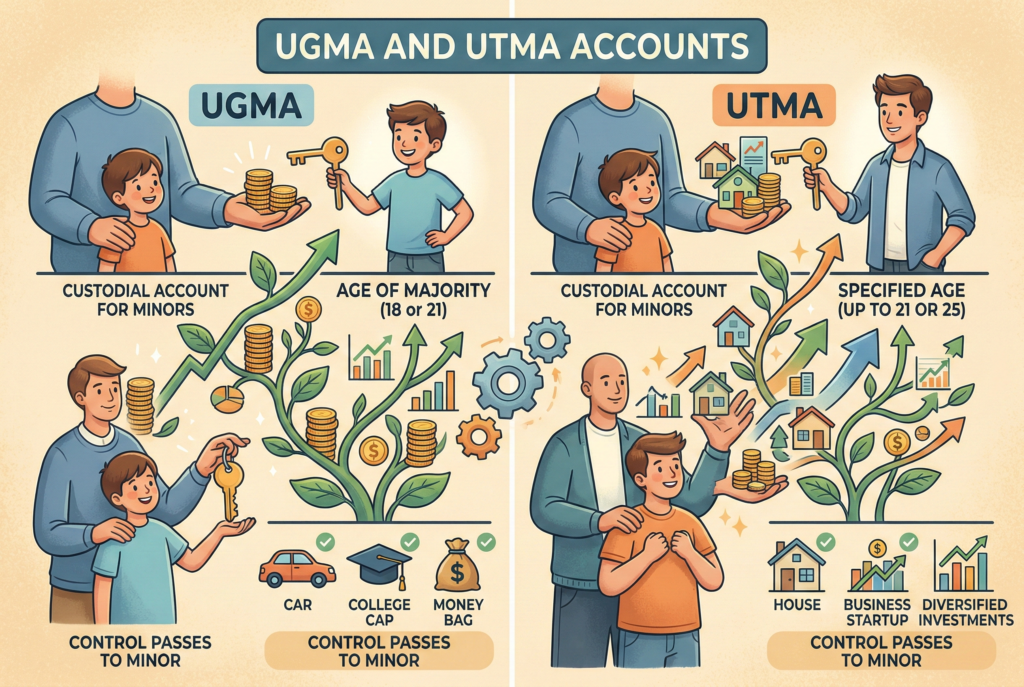

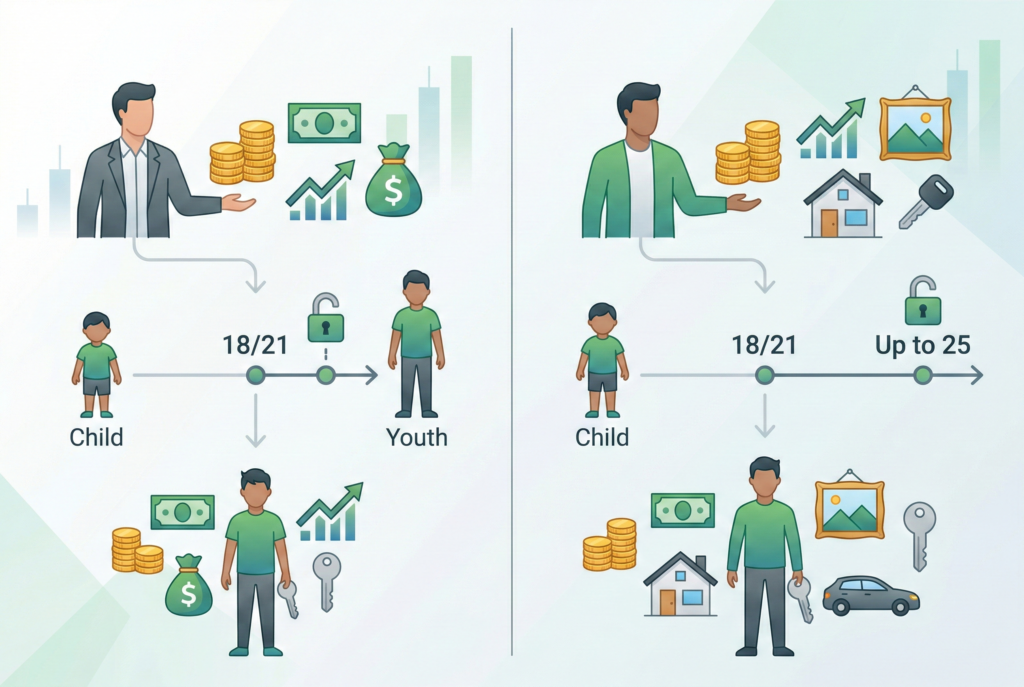

Both UGMA and UTMA accounts are custodial accounts that allow you to transfer assets to a minor under the management of a custodian (typically a parent or guardian). Once the child reaches the age of majority, they gain control of the account. While they have many similarities, the main differences lie in the types of assets they can hold.

UGMA accounts allow the transfer of financial assets like cash, stocks, bonds, and mutual funds to minors, making them more straightforward for families who want to invest in financial assets. UTMA accounts, on the other hand, offer a broader scope, allowing not only financial assets but also physical assets such as real estate, artwork, and patents. This flexibility in UTMA accounts can be especially useful for families with non-traditional investments or assets.

Key Differences Between UGMA and UTMA Accounts

While both accounts are designed to allow asset transfers to minors, the key differences are based on the types of assets allowed and the state laws governing them. UGMA accounts are limited to financial assets, making them ideal for traditional investments, while UTMA accounts allow for more diverse asset types, making them suitable for families interested in non-financial investments.

Another significant difference is the age at which the minor gains control of the account. In most states, UGMA accounts require the minor to take full control at age 18, while UTMA accounts can extend this to age 21, depending on the state. This added flexibility allows for more time to manage and grow the assets before the child takes control.

Tax Benefits and Implications

One of the most appealing aspects of UGMA and UTMA accounts is their tax advantages. These accounts are subject to the kiddie tax, which taxes unearned income at the parent’s tax rate if the child’s unearned income exceeds a certain threshold. However, once the child reaches a certain age, the tax treatment changes, and the child’s tax rate applies.

For families saving for their child’s future, these accounts can be a great way to accumulate wealth while paying little to no tax on the earnings, provided you plan ahead. The tax-deferred growth in these accounts allows the funds to grow without immediate taxation, which can lead to significant financial benefits as the assets compound over time.

The Impact of UGMA and UTMA Accounts on Financial Aid

When it comes to saving for a child’s education, UGMA and UTMA accounts can have a substantial impact on financial aid eligibility. Since the assets in these accounts are considered the children’s, they’re included in the Expected Family Contribution (EFC) formula for financial aid. This can reduce the amount of aid the child is eligible for, as the assets in these accounts will be counted toward the family’s ability to pay for college.

If you’re considering using UGMA or UTMA accounts for college savings, it’s important to keep in mind that these assets can impact your financial aid strategy. It’s worth discussing with a financial advisor to see how best to structure your child’s college savings to minimize the impact on financial aid eligibility.

UGMA vs UTMA: Pros and Cons

Advantages of UGMA and UTMA Accounts

- Tax advantages: Assets grow tax-deferred, and minors are taxed at potentially lower rates once they reach the age of majority.

- Flexibility: UTMA accounts, in particular, allow you to hold a wider variety of assets beyond just financial investments.

- Control: The custodian retains control of the assets until the minor reaches the legal age of majority.

- No contribution limits: There are no annual contribution limits, which makes these accounts ideal for families who want to save large amounts.

Disadvantages of UGMA and UTMA Accounts

- Kiddie tax: If the child’s unearned income exceeds a certain threshold, it is taxed at the parent’s rate.

- Loss of control: Once the minor reaches the legal age, they gain full control of the account and can use the funds however they wish, which may not align with the parent’s intentions.

- Impact on financial aid: As mentioned earlier, UGMA and UTMA accounts can reduce financial aid eligibility for college.

When to Choose UGMA or UTMA Accounts

Choosing between UGMA and UTMA accounts largely depends on your family’s specific goals and preferences. If you’re looking to invest in stocks, bonds, and mutual funds, a UGMA account may be your best bet due to its simplicity and tax advantages. On the other hand, if you want to transfer physical assets, such as real estate or artwork, or if you’re looking for more flexibility with your asset types, a UTMA account would be the better choice.

Both accounts are great options for saving for a child’s future, but it’s essential to understand the trade-offs in terms of taxation, financial aid, and the level of control once the child reaches adulthood. Consulting a financial advisor is recommended to determine which option is best suited to your needs and goals.

Conclusion: Making the Right Choice for Your Family

When deciding between UGMA and UTMA accounts, the decision ultimately comes down to your unique goals, the types of assets you plan to invest in, and how you want to handle the money once your child becomes an adult. These custodial accounts offer flexibility and tax benefits, making them excellent choices for long-term savings and investment growth.

While they come with their own set of pros and cons, understanding these key differences will empower you to make an informed decision. Whether you’re saving for your child’s education, a future business, or just to provide a financial cushion, UGMA and UTMA accounts can be an essential tool in helping you secure your child’s financial future.

Related Articles

UGMA Accounts: What They Are & How They Work for Children’s Savings