Running a business, whether it’s a startup or an established enterprise, often requires financing to support growth, equipment purchases, or day-to-day operations. Understanding business loans, their types, terms, and how they work can make a huge difference in the success of your business. In this article, we’ll break down everything you need to know about business loans, including the different types, loan terms, the application process, and tips on how to get approved for financing.

What Are Business Loans?

A business loan is a sum of money borrowed from a lender to fund various business needs, such as purchasing equipment, expanding operations, or managing cash flow. Depending on the loan type, a business may be required to pay it back over a set term, typically with interest. Business loans can either be secured, where the loan is backed by collateral like property or equipment, or unsecured, where no collateral is required.

Business loans are crucial for entrepreneurs, small businesses, and startups, providing the necessary capital to fund operations or invest in growth. These loans typically have terms that range from short-term (1-3 years) to long-term (5-30 years), depending on the loan’s purpose and the lender’s requirements.

Types of Business Loans

Secured vs. Unsecured Business Loans

Secured loans are backed by collateral, such as property, equipment, or inventory. If you default on the loan, the lender can seize the collateral to recover their losses. These loans generally come with lower interest rates because they represent less risk to the lender.

On the other hand, unsecured loans don’t require any collateral. While these loans offer more flexibility and less risk for you as a borrower, they come with higher interest rates because the lender takes on more risk.

Term Loans

A term loan is one of the most common types of business loans. It provides a lump sum of money that you agree to repay over a set period, usually with a fixed interest rate. These loans can be either short-term (1-3 years) or long-term (up to 30 years), depending on the loan’s purpose and amount. Term loans are ideal for businesses needing funding for capital expenses, such as buying equipment or expanding operations.

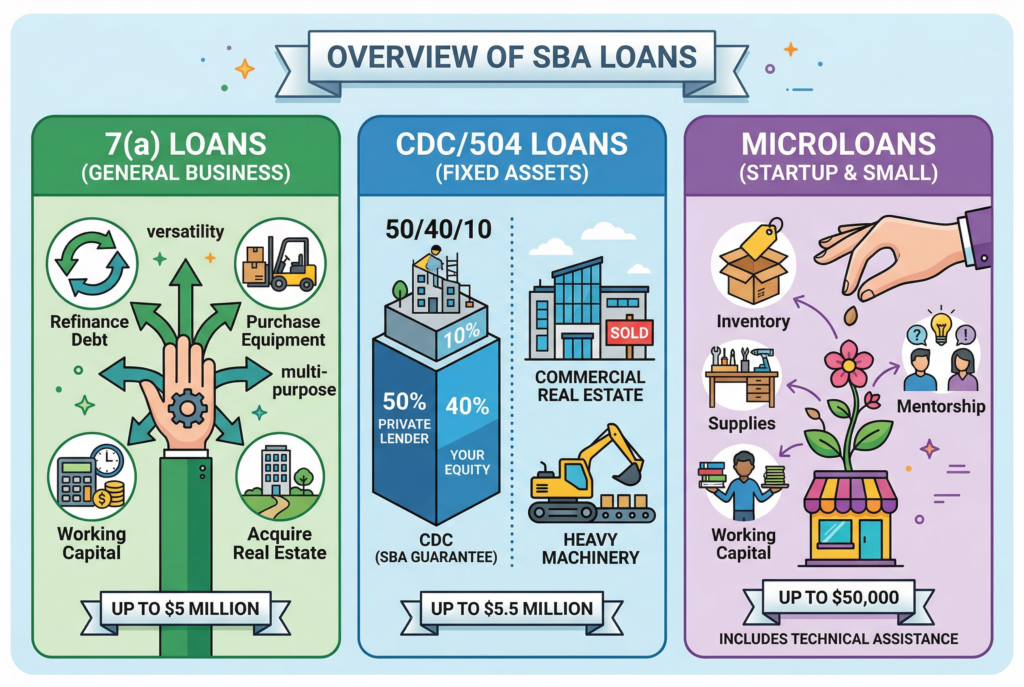

SBA Loans

SBA loans are loans guaranteed by the Small Business Administration (SBA), a government agency. These loans are designed to support small businesses and startups by providing easier access to financing with lower interest rates and longer repayment terms. However, the application process can be more lengthy and involved than with traditional loans. There are several types of SBA loans, including 7(a) loans, CDC/504 loans, and microloans, each with its own eligibility requirements and terms.

Business Line of Credit

A business line of credit is a flexible loan option that gives businesses access to a predetermined amount of capital, which they can draw from as needed. Unlike a traditional loan, you only pay interest on the money you actually use, making it a good option for managing cash flow or covering emergency expenses.

Lines of credit are typically unsecured, but the lender may require a personal guarantee or a strong business credit score for approval.

Equipment Loans

Equipment loans are used specifically to finance the purchase of equipment, machinery, or vehicles for your business. These loans are typically secured by the equipment itself, meaning the lender can repossess the equipment if you fail to repay the loan. They offer relatively low-interest rates compared to unsecured loans, and the term length usually matches the expected life of the equipment.

Invoice Financing

If your business is struggling with cash flow due to unpaid invoices, invoice financing may be a good option. With this type of loan, you borrow money based on the value of your outstanding invoices. The lender will typically advance you 80-90% of the invoice value, and you pay the loan back when the customer settles the invoice. Invoice financing is a short-term solution to improve liquidity, but it comes with higher fees than other types of loans.

Microloans

A microloan is a small loan offered by nonprofit organizations, typically aimed at helping small businesses or startups that may not qualify for traditional bank loans. The amounts are usually smaller, ranging from $500 to $50,000, and the repayment terms are more flexible.

Business Loan Terms: What You Need to Know

1. Interest Rates

The interest rate on a business loan is the percentage you’ll pay on the amount borrowed, and it can significantly impact the cost of your loan. Secured loans generally come with lower interest rates, while unsecured loans may have higher rates to compensate for the risk the lender is taking. The interest rate can either be fixed, meaning it remains the same throughout the loan term, or variable, meaning it can change depending on the market.

2. Loan Amount

The loan amount you’re approved for depends on several factors, including the lender’s requirements, your business’s financial history, and your ability to repay. Some lenders may also require you to have a personal guarantee if your business doesn’t have enough assets or creditworthiness to secure the loan.

3. Repayment Terms

Repayment terms determine how long you have to pay back the loan. Shorter terms generally mean higher monthly payments but lower overall interest. Longer repayment terms offer lower monthly payments but can result in paying more interest over time. It’s essential to choose a loan term that fits within your budget while still allowing you to maintain cash flow for other business needs.

4. Collateral and Guarantees

For secured loans, the lender may require collateral, such as real estate, equipment, or inventory, that they can seize if you fail to repay the loan. Unsecured loans don’t require collateral but may come with higher interest rates.

5. Fees

In addition to interest rates, many business loans come with fees, including origination fees, application fees, and processing fees. Make sure to account for these costs when calculating the total cost of borrowing.

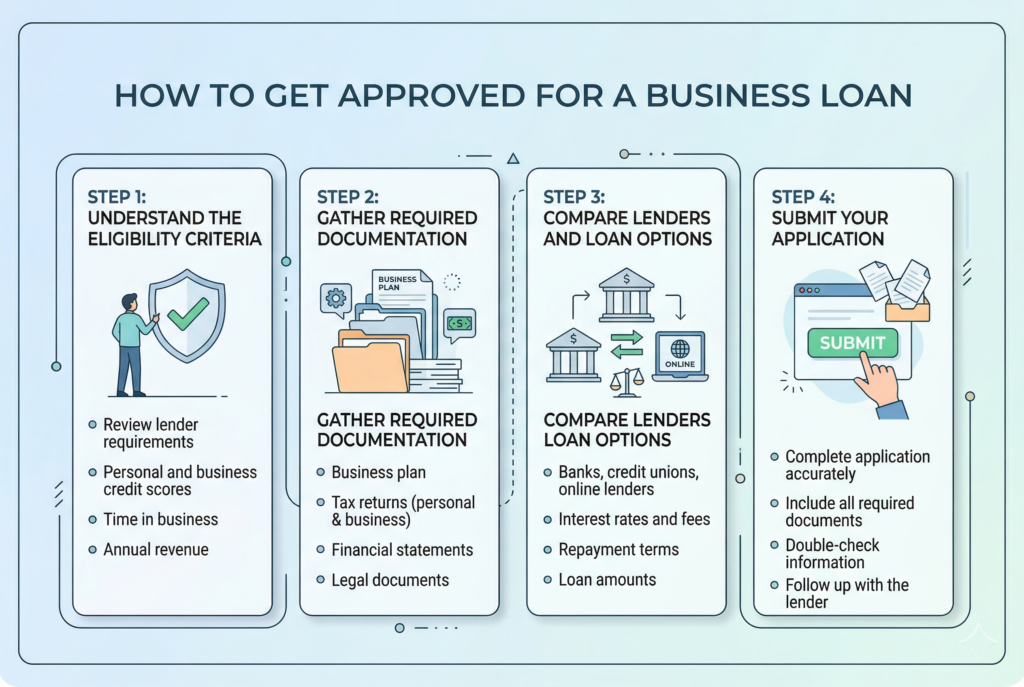

How to Get Approved for a Business Loan

The approval process for a business loan typically involves several steps. Lenders will evaluate your business’s creditworthiness, financial stability, and ability to repay the loan. Here’s what you need to know about getting approved:

Step 1: Understand the Eligibility Criteria

Lenders look at several factors when assessing your eligibility for a business loan:

- Credit score: Both your personal and business credit score will be evaluated. A higher credit score increases your chances of securing favorable loan terms.

- Revenue and cash flow: Lenders want to see that your business is generating enough revenue to cover loan payments. They may require financial statements or bank statements to verify your cash flow.

- Business history: Lenders often prefer businesses with a stable track record, typically at least two years in operation. Startups may need to provide a detailed business plan.

- Collateral: For secured loans, you may need to offer collateral to secure the loan. This is especially important if your business has limited credit or a high-risk profile.

Step 2: Gather Required Documentation

Before applying, make sure you have all the necessary documentation in order. This may include business and personal tax returns, financial statements and bank statements, business plan (for startups), and collateral documents (if applicable).

Step 3: Compare Lenders and Loan Options

Take time to compare different loan providers to find the best rates and terms for your business. You can approach banks, credit unions, or online lenders, each of which has different qualifications, interest rates, and processing times. Online lenders may be a good option for faster approvals, while traditional banks may offer better interest rates for established businesses.

Step 4: Submit Your Application

Once you’ve selected a lender, submit your application, ensuring that all required documents are included. Be prepared to explain your business’s needs and why you’re seeking the loan.

Conclusion: Make Smart Loan Decisions for Your Business

Understanding the types of business loans, their terms, and how they work is key to making informed borrowing decisions. By choosing the right loan, preparing for the application process, and staying within your repayment capacity, you can fuel your business’s growth without overextending your finances.

Whether you need a short-term loan to address immediate cash flow issues or a long-term loan for expansion, there are plenty of options available. Take the time to carefully evaluate your needs, compare loan options, and understand the terms to ensure you choose the best loan for your business.