A USDA loan can be one of the most affordable ways to buy a home if you qualify. For eligible borrowers, these loans can offer no down payment, competitive terms, and a path to homeownership in qualifying areas that many buyers wrongly assume are limited to farmland or very remote towns. The key is understanding how USDA loans work, who qualifies, and what tradeoffs come with them.

What a USDA Loan Is

A USDA loan is a mortgage backed by the U.S. Department of Agriculture through its Rural Development housing programs. The most common option for homebuyers is the Single Family Housing Guaranteed Loan Program, which helps approved lenders offer mortgages to low- and moderate-income households for primary residences in eligible rural areas. USDA also has a Direct Home Loan program for low- and very-low-income applicants, where the government lends directly.

The biggest reason USDA loans get attention is simple: they can allow qualified buyers to purchase a home with 0% down. That makes them especially appealing for first-time buyers or households that can afford a monthly mortgage payment but haven’t built a large down payment yet.

How USDA Loans Work

With the Guaranteed Loan Program, you apply through an approved private lender, not directly through USDA. The lender underwrites the mortgage, and USDA provides a guarantee that reduces the lender’s risk. With the Direct Loan program, USDA evaluates the borrower and makes the loan itself.

In both cases, the property must generally be your primary residence, and it must be located in an eligible area. USDA describes these homes as needing to be adequate, modest, decent, safe, and sanitary. These programs aren’t meant for second homes, vacation properties, or investment real estate.

For the guaranteed program, USDA materials also note an upfront guarantee fee of 1.00% and an annual fee of 0.35% of the unpaid principal balance, along with a $25 technology fee. These costs matter because even though there’s no down payment requirement, the loan still isn’t free of financing-related charges.

Who Is Eligible for a USDA Loan

Eligibility depends on several factors, but the biggest ones are income, property location, and occupancy. USDA states that eligibility for its housing programs is based on income and varies by area, and the official eligibility site emphasizes that the home must be in an eligible rural area and that household income must meet program guidelines.

One detail many buyers miss is that USDA eligibility can be based on household income, not just the income of the people listed on the mortgage. USDA’s eligibility help page explains that income from all adult household members may need to be disclosed for eligibility purposes, even if they aren’t applying for the loan.

For the Direct Loan program, USDA says it assists low- and very-low-income applicants, and that repayment ability and county loan limits are part of the review. It also says no down payment is typically required, though applicants with assets above asset limits may have to use some of those assets.

What Counts as a USDA-Eligible Area

One of the most misunderstood parts of USDA loans is the word rural. Many eligible areas aren’t isolated at all. Some are suburban communities, small cities, and outer-ring areas that still meet USDA’s geographic rules. USDA’s official eligibility tool is the place to check both property eligibility and income eligibility, and the agency notes that map results aren’t a final determination until a full application is reviewed. That means a buyer shouldn’t assume a property is disqualified just because it feels suburban, and shouldn’t assume it qualifies just because it looks rural. The map check is essential.

Key Benefits of a USDA Loan

The most obvious advantage is no down payment for qualified borrowers. That can remove one of the biggest barriers to buying a home. USDA also positions these programs as affordable homeownership tools for households that may not qualify as easily for conventional financing.

Another benefit is that USDA financing is built specifically for owner-occupied housing in eligible communities, which can help buyers who want a primary home rather than an investment property. The Direct Loan program can be especially helpful for lower-income households because USDA says payment assistance may reduce the effective interest rate to as low as 1% for eligible borrowers. For buyers with limited savings, these features can make a meaningful difference in affordability.

Drawbacks You Shouldn’t Ignore

Geography

The biggest limitation is geography. If the home you want isn’t in an eligible area, the loan won’t work. Income rules can also block otherwise qualified buyers, especially if total household income is too high for the location and household size.

Program Fees

There are also program fees. The guaranteed loan’s upfront and annual fees function somewhat like mortgage insurance in other loan types. So while the no-down-payment feature is attractive, buyers still need to evaluate the full monthly cost.

Restriction

The Direct Loan program is also more restrictive. It’s aimed at low- and very-low-income applicants and includes repayment ability reviews, area loan limits, and other program-specific conditions.

How to Buy a Home With No Down Payment Using a USDA Loan

The first step is to check the property area through USDA’s official eligibility tool. Then review your household income against the area limits. After that, decide whether you’re more likely to fit the Guaranteed program through a lender or the Direct program through USDA.

If you’re using the guaranteed route, talk with an approved lender about prequalification, monthly payment estimates, and total closing costs. If you may qualify for the direct program, contact USDA Rural Development in your state to review program requirements and application steps. USDA’s housing program pages confirm that both purchase and certain build or refinance uses may be available under qualifying circumstances.

The practical path is straightforward: confirm the area, confirm the income rules, choose the right program, and review the total cost of ownership instead of focusing only on the fact that the down payment may be zero.

How USDA Loans Compare With Other Low-Down-Payment Options

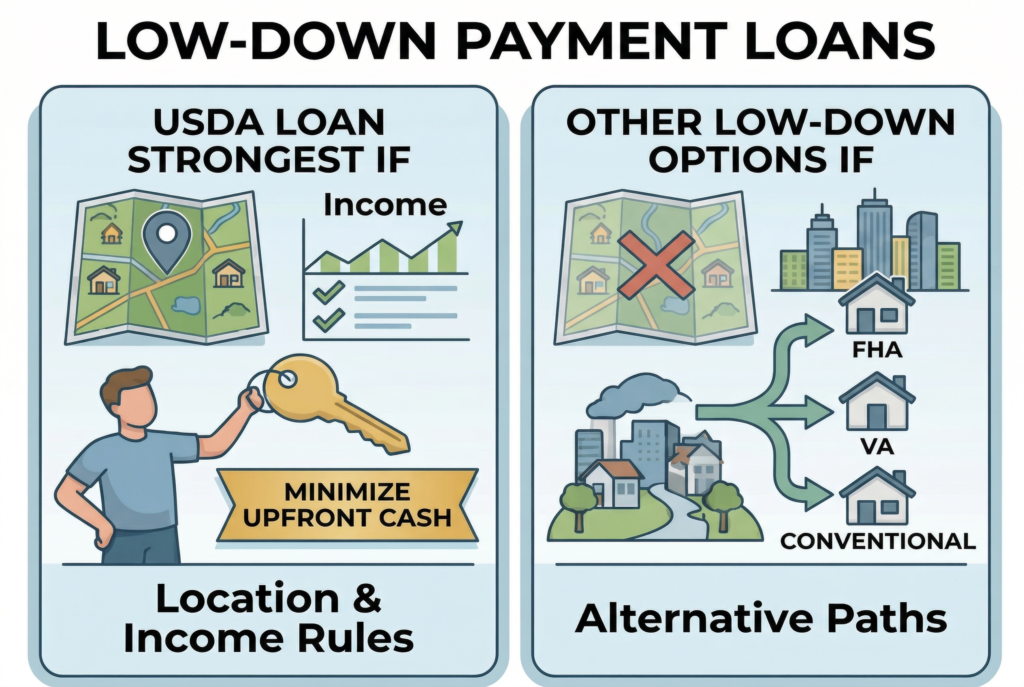

A USDA loan is strongest for buyers who meet the location and income rules and want to minimize upfront cash. If you don’t qualify geographically or by income, you may need to compare it with FHA, VA, or conventional low-down-payment loans. The USDA advantage is primarily the 0% down structure combined with program support for eligible households in qualifying communities. That said, the best loan is the one that fits your full situation, including home location, income, monthly payment comfort, and closing-cost readiness.

Conclusion

A USDA loan can be an excellent homebuying option for borrowers who want no down payment and are buying in an eligible area. The biggest things to understand are the property map rules, the household income rules, and the difference between the Guaranteed and Direct programs. For the right buyer, USDA financing can make homeownership much more accessible. But like any mortgage, it works best when you look past the headline benefit and evaluate the full long-term cost.