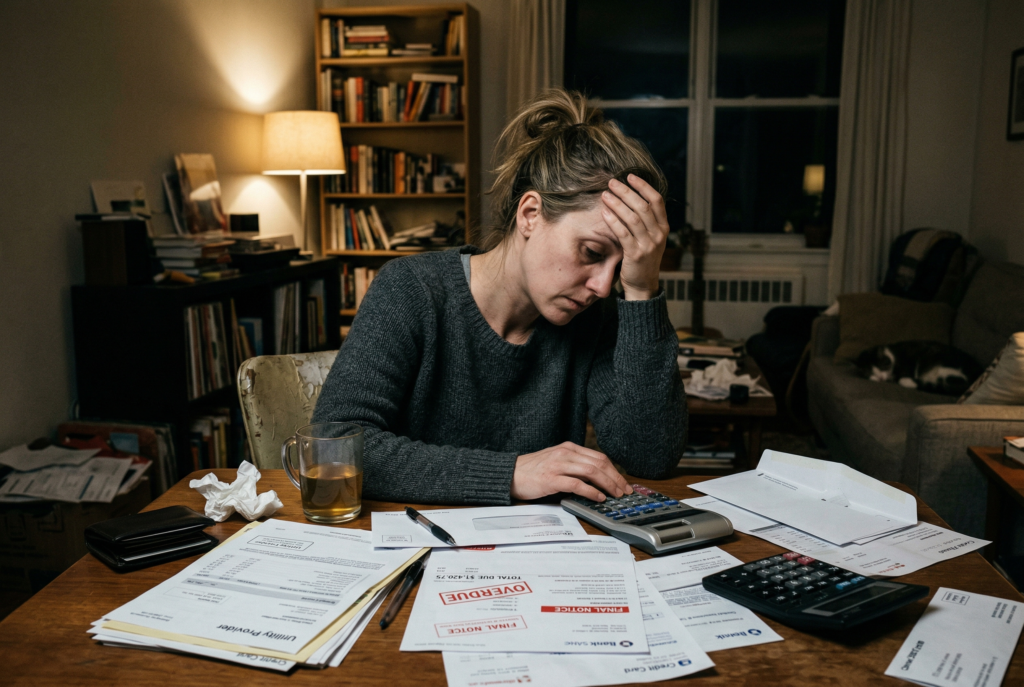

Declaring bankruptcy can be one of the hardest financial decisions a person makes, but for some households, it can also be the clearest path toward stability. When debt has become unmanageable, collections won’t stop, and there’s no realistic way to catch up, bankruptcy may offer legal protection and a chance to reset. Still, it isn’t a simple fix, and it comes with real consequences that deserve careful thought.

What Bankruptcy Actually Means

Bankruptcy is a federal legal process designed to help individuals or businesses deal with debts they can’t repay. For individuals, the most common options are Chapter 7 and Chapter 13 bankruptcy. Chapter 7 is often described as liquidation, while Chapter 13 is a repayment plan. Which one may be available depends on your income, debts, assets, and other eligibility rules.

A bankruptcy filing can trigger an automatic stay, which generally stops most collection actions, including many lawsuits, wage garnishments, and creditor contact while the case moves through court. That breathing room is one reason bankruptcy can be so powerful for people facing relentless financial pressure. At the same time, bankruptcy doesn’t erase every financial problem. Some debts may not be discharged, and filing can affect your credit, assets, and future borrowing options.

When Declaring Bankruptcy May Make Sense

Bankruptcy may make sense when debt is no longer just stressful but truly unworkable. That often means you can’t keep up with minimum payments, balances continue growing despite your efforts, or collection activity has made normal budgeting almost impossible.

It can also become a realistic option after major life events such as job loss, illness, divorce, reduced income, or a period of relying heavily on credit cards to cover basic expenses. If you’ve cut spending, tried to catch up, and still see no credible path out, bankruptcy may deserve serious consideration.

This decision tends to make the most sense when the problem is structural, not temporary. If a household is carrying more unsecured debt than it could reasonably repay within a few years, even with disciplined budgeting, continuing to struggle may do more harm than evaluating a legal reset.

The Difference Between Chapter 7 and Chapter 13

For most individuals, the two main forms of personal bankruptcy are Chapter 7 and Chapter 13.

Chapter 7 bankruptcy is designed to wipe out certain debts relatively quickly, but a trustee may sell nonexempt property to repay creditors. The court notes that individuals must also meet eligibility rules, including a means test, and complete approved credit counseling within 180 days before filing, with limited exceptions.

Chapter 13 bankruptcy is different. Instead of immediate liquidation, it involves a court-approved repayment plan funded over time. The U.S. Courts say those plans cannot last longer than five years, and during the case, creditors generally can’t start or continue collection efforts. Chapter 13 is often used by people who have regular income and want to catch up on secured debts such as a mortgage or car loan while keeping property.

The better option depends on your financial picture, not just your preference. Someone with little disposable income and mostly unsecured debt may be looking at a very different solution from someone who has steady income but needs time to catch up on arrears.

Signs You May Need to Consider Bankruptcy

A few warning signs often show when bankruptcy should move from a distant idea to a serious discussion.

One is using new debt to pay old debt. Another is being unable to cover necessities without leaning on credit cards. Repeated late payments, lawsuits from creditors, wage garnishment, or the threat of losing a home or car can also signal that the situation has become more severe.

Another important sign is emotional and financial exhaustion. If you’re making payments but balances barely move because interest and fees keep rebuilding the debt, the problem may no longer be fixable through ordinary repayment methods alone.

Bankruptcy isn’t only for people with no income or no assets. In many cases, it becomes relevant when a person still has income, but not enough to restore long-term stability under current debt obligations.

Key Consequences of Declaring Bankruptcy

The most immediate consequence is damage to your credit profile. Bankruptcy is a major negative event on a credit report, and it can affect approval odds, borrowing costs, rental applications, and financial flexibility for years.

There may also be consequences for your property. In Chapter 7, some assets may be protected through exemptions, but the court warns that a trustee may liquidate property that isn’t exempt. In Chapter 13, the focus is more on repayment over time, but you’re still entering a court-supervised process that demands consistency and documentation.

Another consequence is that not all debts disappear. The U.S. Courts explain that a discharge is not absolute, and some obligations aren’t discharged depending on the type of debt and the facts of the case. Also, a discharge does not automatically remove a valid lien from property.

Even so, consequences need to be weighed against the alternative. Continuing to fall behind, absorb fees, and face collection pressure may already be doing serious financial damage.

What Bankruptcy Can and Can’t Do

One of the biggest benefits of bankruptcy is that it can stop the spiral. The automatic stay can pause many creditor actions, and the eventual discharge can eliminate many unsecured debts, giving people a chance to rebuild instead of staying trapped in a cycle they can’t break.

But bankruptcy has limits. It doesn’t guarantee you’ll keep every asset. It doesn’t make every debt vanish. It doesn’t solve budgeting problems by itself. And it doesn’t mean you’ll instantly regain strong credit. That’s why bankruptcy works best when it’s part of a broader recovery plan. The court process may provide the legal reset, but long-term stability still depends on future spending habits, emergency savings, and realistic financial planning.

Alternatives to Declaring Bankruptcy

Before filing, it’s often worth reviewing alternatives. A nonprofit credit counseling agency may help you evaluate your full financial picture and, in some cases, set up a debt management plan. The CFPB explains that credit counseling organizations can help with budgeting, debt review, and debt management plans.

Some borrowers may also consider debt consolidation, hardship programs, direct negotiation with creditors, or other structured payoff methods. But these options only work when the debt is still realistically repayable. If the numbers don’t support repayment, delaying bankruptcy just to avoid the label may create deeper harm.

You should also be cautious with for-profit debt relief promises. The FTC warns that debt relief and credit repair scams target people struggling with significant debt, often by falsely promising big reductions.

How to Decide Your Best Option

The right decision usually comes down to one central question: can you realistically repay your debts within a reasonable time without sacrificing basic financial stability?

If the answer is yes, a non-bankruptcy solution may be better. If the answer is no, and the debt burden keeps worsening despite serious effort, bankruptcy may be the more responsible path.

It also helps to look at the type of debt you have. Someone overwhelmed by unsecured credit card balances may face a different choice from someone whose biggest issue is falling behind on a mortgage. Income stability matters too. A person with regular income may be a better fit for Chapter 13, while someone with little ability to fund repayment may need to examine Chapter 7 more closely. This isn’t a decision to make based on fear alone. It should be based on numbers, legal realities, and the long-term effect on your household.

Questions to Ask Before Filing

Before moving forward, ask yourself whether your debt problem is temporary or permanent, whether you’ve already tried realistic alternatives, and whether keeping up with current payments would still leave you financially unstable for years.

You should also ask what you’re trying to protect. Is the priority stopping lawsuits, keeping a home, ending credit card debt, or simply getting back enough breathing room to build a workable life again? Those answers help shape which option may fit best.

It’s also important to understand that courts provide general information, not personal legal advice. The U.S. Courts explicitly state that courts and bankruptcy courts can’t provide legal or financial advice to filers.

Conclusion

Declaring bankruptcy can make sense when debt has become impossible to manage, collection pressure keeps building, and there’s no realistic way to recover through ordinary repayment. It can provide legal protection, stop many creditor actions, and in some cases discharge debts that would otherwise keep dragging your finances down.

But it also carries serious consequences, including credit damage, possible asset loss, and limits on what debts can be erased. The best choice is the one that honestly reflects your financial reality. For some people, that will be budgeting, counseling, or a repayment plan. For others, bankruptcy may be the clearest and most effective path toward a genuine fresh start.