Debt refinancing is a powerful tool that can help homeowners, business owners, and individuals take control of their finances, reduce monthly payments, or consolidate debt. Whether you’re looking to lower interest rates, adjust your loan terms, or access home equity, refinancing can be a strategic move to improve your financial situation.

However, like any financial decision, it’s essential to understand how debt refinancing works, its benefits and risks, and how to choose the right option for your needs. In this article, we’ll explain what debt refinancing is, the various types, its potential benefits and risks, and guide you on when and how to refinance for optimal results.

What is Debt Refinancing?

Debt refinancing involves replacing your existing debt, whether it’s a mortgage, auto loan, student loan, or other forms of credit, by taking out a new loan with better terms. The goal is to replace the old debt with a loan that offers lower interest rates, better payment terms, or even cash-out options to use for other purposes. Essentially, you’re swapping your old debt for a new one that might be more manageable or better suited to your current financial situation.

For example, if you have a mortgage with a high interest rate, refinancing might allow you to secure a new mortgage with a lower rate, reducing your monthly payments and saving you money over time. Or, if you have high-interest credit card debt, you could refinance that debt with a personal loan at a lower rate.

Why Refinance?

Refinancing can help you achieve a variety of financial goals, including:

- Lowering interest rates to save on monthly payments.

- Extending your loan term to reduce your monthly payments.

- Shortening your loan term to pay off the debt faster and save on interest.

- Consolidating debt by combining multiple loans into one.

- Accessing home equity for home improvement, education, or other major expenses.

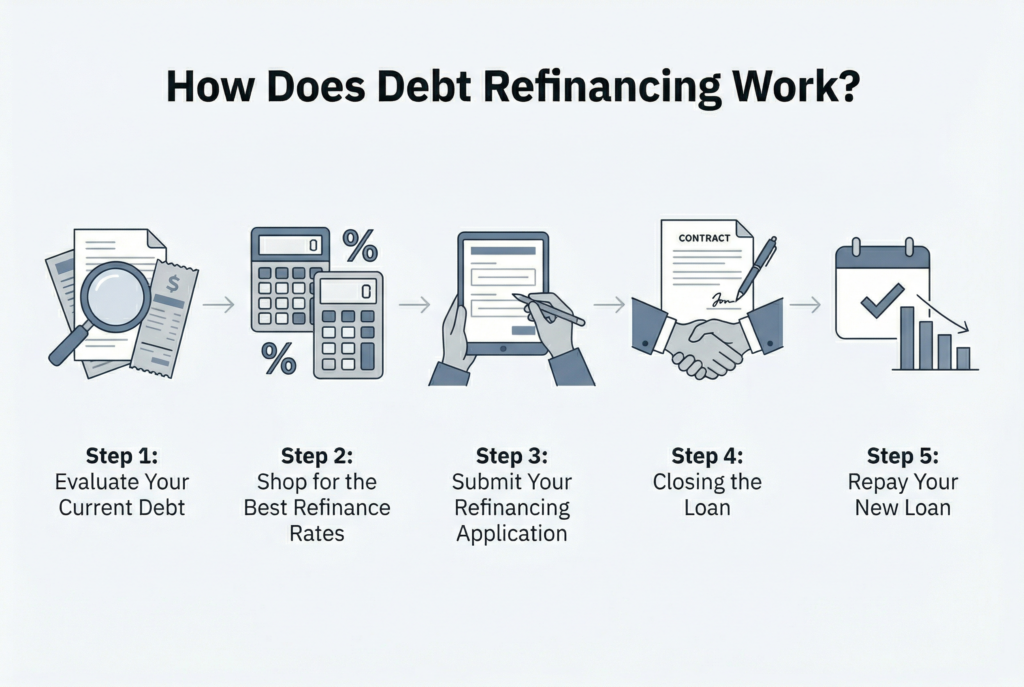

How Does Debt Refinancing Work?

Step 1: Evaluate Your Current Debt

The first step in refinancing is to assess your current financial situation. What kind of debt are you trying to refinance? Is it a mortgage, auto loan, or student loan? Take note of the interest rates, loan balance, and repayment terms on your current debt. Understanding your existing debt will help you determine if refinancing will be beneficial and help you identify areas where you can improve.

Step 2: Shop for the Best Refinance Rates

Refinancing can offer better terms depending on the interest rates and financial market conditions. You should compare different lenders and financial institutions to find the most favorable rates. Online tools like refinance calculators can help you estimate potential savings, allowing you to calculate how much you might save on your monthly payments and overall loan costs by refinancing. Make sure to factor in fees like closing costs, application fees, or prepayment penalties from your old loan, as these costs could impact the overall savings.

Step 3: Submit Your Refinancing Application

Once you’ve chosen a lender and determined the refinancing type that fits your goals, you’ll need to apply for the loan. Lenders will evaluate your credit score, income, debt-to-income ratio (DTI), and home equity (if refinancing a mortgage). Be prepared to submit documents like:

- Proof of income (pay stubs or tax returns)

- Proof of assets (bank statements or retirement accounts)

- Credit report (for credit score evaluation)

- Current loan details (balance or terms)

Step 4: Closing the Loan

If your application is approved, you’ll go through a closing process. This is similar to when you first obtained the loan, but it’s usually quicker since you’re refinancing. You’ll sign the loan documents, and the new loan will pay off your existing debt. Depending on the type of loan, closing costs may include fees for appraisals, title insurance, or loan origination. Some lenders may allow you to roll these costs into your new loan amount, while others may require you to pay them upfront.

Step 5: Repay Your New Loan

After refinancing, you’ll begin making payments on the new loan based on the agreed-upon terms. Your new loan may have a different monthly payment, interest rate, or loan term than your original loan, so be sure to review your payment schedule carefully. Stick to the new repayment plan to avoid penalties or additional fees.

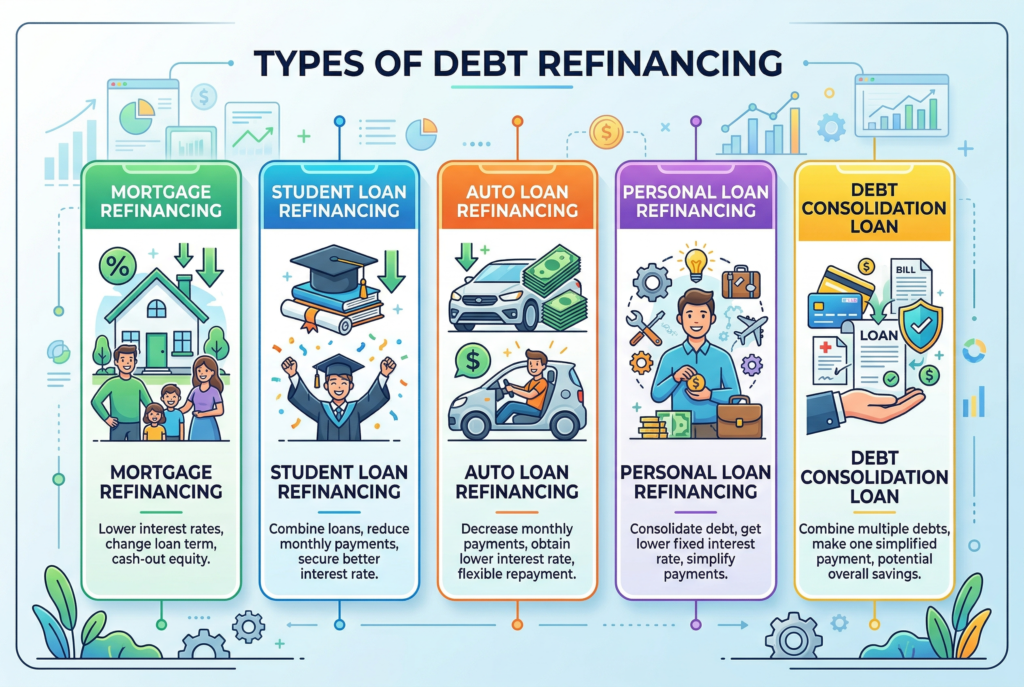

Types of Debt Refinancing

Mortgage Refinancing

Mortgage refinancing is the process of replacing your existing home loan with a new one that has better terms. Homeowners typically refinance to lower their interest rates, shorten the loan term, or switch from an adjustable-rate mortgage (ARM) to a fixed-rate mortgage for more stability. Refinancing a mortgage can also help you tap into your home equity for cash-out refinancing, which can be used for home improvements, consolidating debt, or other large expenses.

Student Loan Refinancing

If you have multiple student loans, refinancing can be a way to consolidate them into one loan with a lower interest rate and potentially better repayment terms. Refinancing federal student loans into a private loan may reduce your interest rate, but it also means losing access to federal protections such as income-driven repayment plans and loan forgiveness programs. If you’re considering refinancing student loans, it’s essential to weigh the pros and cons.

Auto Loan Refinancing

If you’re paying high interest on an auto loan, refinancing can help reduce your interest rate and lower your monthly payments. By refinancing, you may be able to shorten your loan term or extend it, depending on your needs. However, if the value of your car has significantly depreciated, refinancing might not always be a viable option.

Personal Loan Refinancing

Personal loan refinancing involves taking out a new personal loan to pay off existing debt, such as credit cards, medical bills, or other loans. This can help lower your interest rate and consolidate multiple debts into one manageable monthly payment. Be sure to check for origination fees and prepayment penalties before refinancing.

Debt Consolidation Loan

If you have multiple high-interest debts, a debt consolidation loan can combine them into one loan with a single monthly payment. This type of refinancing can help simplify your finances and reduce the amount of interest you pay over time. Debt consolidation loans can be secured (using collateral like your home) or unsecured, depending on your financial situation.

Benefits of Debt Refinancing

1. Lower Interest Rates

One of the biggest reasons people refinance is to lower their interest rates. When you refinance, you might qualify for a lower rate, which can significantly reduce your monthly payments and the total interest you pay over time. This is especially beneficial in a low-interest-rate environment or if your credit score has improved since you first took out the loan.

2. Lower Monthly Payments

Refinancing can reduce your monthly payments by extending the term of your loan or securing a lower interest rate. This can free up cash for other financial goals or help you manage your budget more effectively.

3. Debt Consolidation

If you have multiple debts, refinancing can allow you to consolidate them into a single loan. This can simplify your finances and help you stay organized by having only one monthly payment to track. Consolidating debt can also potentially reduce your overall interest costs.

4. Improved Loan Terms

Refinancing allows you to negotiate better loan terms, such as a lower interest rate, a shorter loan term, or more favorable repayment schedules. If you’re looking to pay off your debt faster or want more flexibility in your payments, refinancing can provide the opportunity to improve your loan terms.

Risks of Debt Refinancing

1. Closing Costs and Fees

Refinancing typically comes with closing costs, which can include appraisal fees, origination fees, and transaction costs. These costs can eat into the savings you might gain from refinancing, so it’s essential to consider them when deciding whether to refinance.

2. Extended Repayment Terms

If you refinance to a longer loan term, you may lower your monthly payments, but you could end up paying more in interest over the life of the loan. Make sure to weigh the short-term savings against the long-term costs before making a decision.

3. Impact on Credit Score

Refinancing can affect your credit score, especially if you close old accounts or open new ones. However, if you manage the refinancing process carefully, such as by making timely payments and maintaining low credit utilization, your credit score should recover over time.

4. Penalty Fees

In some cases, refinancing may trigger penalty fees if you pay off your old loan early. Be sure to check your original loan agreement for any prepayment penalties before refinancing.

When is the Best Time to Refinance?

The timing of your refinance can make a significant difference in the savings you achieve. The best time to refinance is when interest rates are low or when your credit score has improved. Additionally, if your home has appreciated in value or you’ve paid down a significant portion of your debt, it could be an ideal time to refinance.

Other factors to consider include the state of the economy, your personal financial situation, and your long-term financial goals. If you’re unsure, it can be helpful to consult a financial advisor to determine if refinancing aligns with your financial strategy.

Conclusion: Is Refinancing Right for You?

Debt refinancing can be a great way to reduce monthly payments, lower interest rates, and access home equity, but it’s essential to weigh the benefits against the costs. By understanding how refinancing works, the types of options available, and the potential risks, you can make an informed decision that aligns with your financial goals.

Evaluate your current financial situation, compare refinancing offers, and consult with a financial advisor if needed. Refinancing can be a powerful tool when used strategically, allowing you to make the most of your financial resources.