Mortgage refinancing can be an excellent financial strategy for homeowners looking to reduce their monthly payments, lower their interest rates, or access the equity in their homes. Whether you’re considering refinancing to reduce costs or consolidate debt, understanding the refinancing process, the different types of refinances, and when it’s the best time to refinance is essential for making the right decision. In this article, we’ll explore the basics of mortgage refinancing, the types of refinancing options, the benefits, and the best time to refinance to help you maximize your savings and financial security.

What is Mortgage Refinancing?

Mortgage refinancing is the process of replacing your current mortgage with a new loan, typically with different terms. The goal of refinancing is to improve your financial situation, whether that’s lowering your interest rate, adjusting your loan term, or tapping into your home’s equity.

When you refinance, you essentially pay off your existing mortgage with the new loan and continue making payments based on the updated terms. Refinancing can help you achieve various goals, such as lowering your interest rate, shortening your loan term, or accessing cash for home improvements or debt consolidation. However, it’s important to carefully consider the costs, like closing fees, before deciding to refinance.

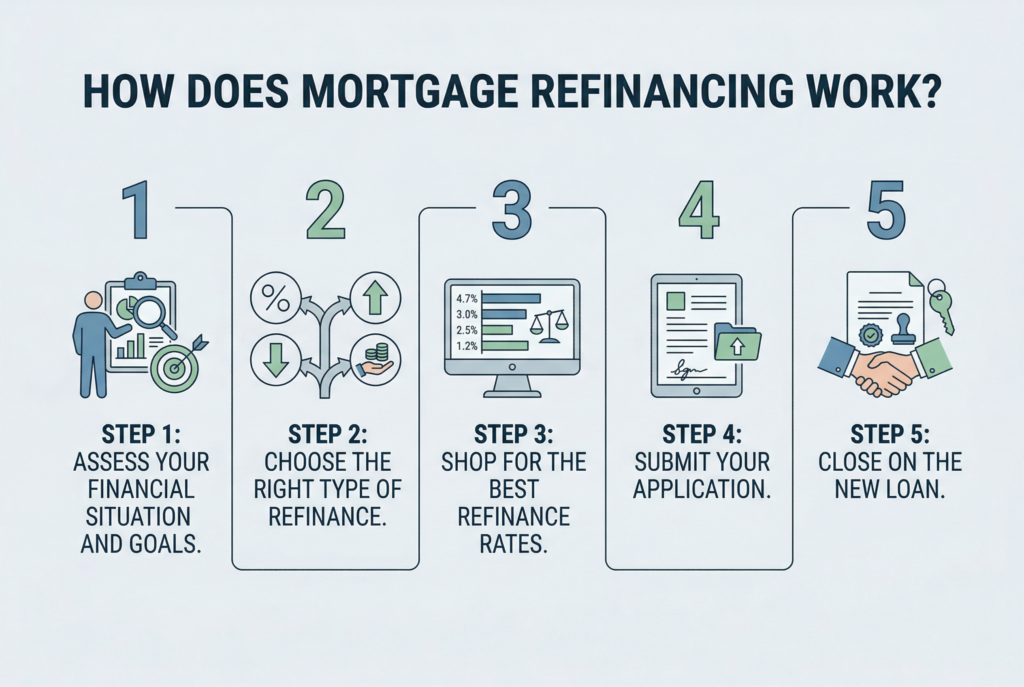

How Does Mortgage Refinancing Work?

Step 1: Assess Your Financial Situation and Goals

Before you refinance, it’s essential to evaluate why you want to refinance and what you hope to achieve. Some common reasons for refinancing include:

- Lowering your interest rate

- Reducing your monthly payments

- Paying off your loan faster

- Accessing cash from your home’s equity for debt consolidation

- Switching from an ARM to a fixed-rate mortgage

This initial assessment will guide your decision-making process and determine the type of refinancing that best suits your needs.

Step 2: Choose the Right Type of Refinance

There are several types of refinancing options, each with its own benefits and drawbacks. The type of refinance you choose will depend on your goals, financial situation, and long-term plans.

Rate-and-Term Refinance

This is the most common type of refinancing. It involves changing the interest rate and/or loan term of your existing mortgage without borrowing additional money. This option is ideal if you want to lower your interest rate or shorten your loan term to pay off the mortgage faster.

Cash-Out Refinance

With a cash-out refinance, you take out a new mortgage for more than you owe on your current loan and receive the difference in cash. This is a popular option for homeowners looking to tap into their home’s equity for home improvements, debt consolidation, or large purchases.

Cash-In Refinance

In contrast to a cash-out refinance, a cash-in refinance involves paying down a portion of your mortgage to reduce the loan balance. This option can help reduce your loan-to-value (LTV) ratio, potentially eliminating the need for mortgage insurance and improving your loan terms.

Streamlined Refinance

Some loan types, such as FHA loans or VA loans, offer streamlined refinancing options, which are faster and involve less paperwork. Streamlined refinancing is an excellent option for homeowners with FHA or VA loans who want to lower their rates or change their loan terms without much hassle.

Step 3: Shop for the Best Refinance Rates

Once you’ve chosen the type of refinance that fits your needs, it’s time to shop around for the best mortgage rates. Just like with your original mortgage, comparing rates from different lenders can help you secure the best deal. Online refinance calculators are useful tools that allow you to estimate how different interest rates and terms will affect your monthly payment and the total cost of the loan.

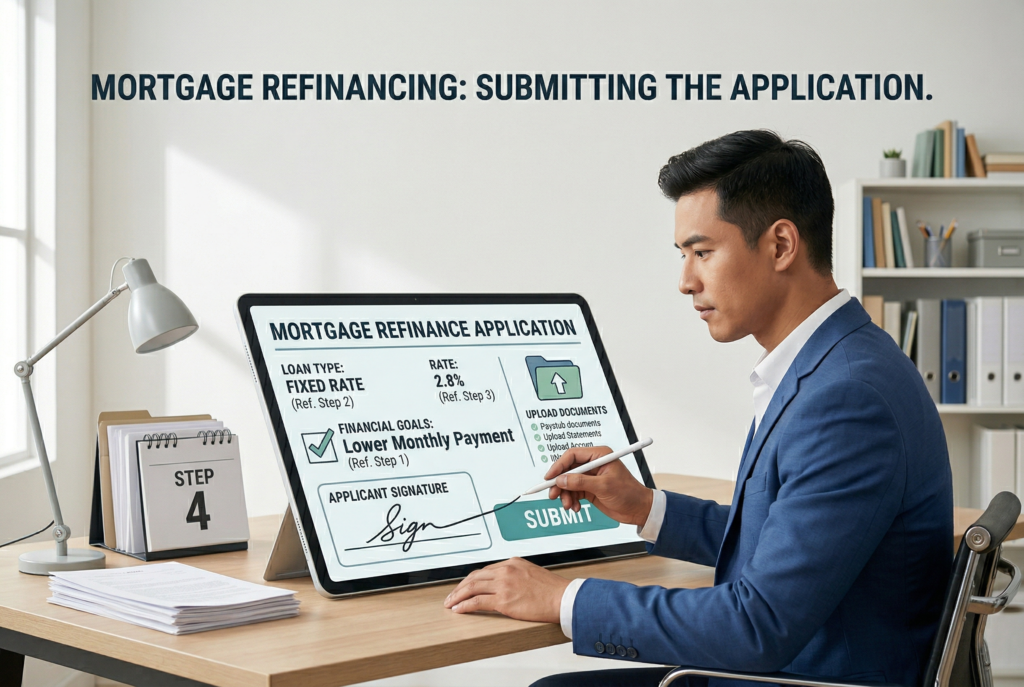

Step 4: Submit Your Application

After choosing a lender and refinancing option, you’ll need to submit a loan application. Be prepared to provide financial documentation, including proof of income (pay stubs, tax returns), credit score (to determine your interest rate), home equity (to evaluate the value of your property), and current mortgage information. Lenders will review these documents to assess your eligibility and determine the terms of the new loan.

Step 5: Close on the New Loan

Once your application is approved, you’ll go through a closing process similar to when you first bought your home. You’ll sign the loan documents, and the new lender will pay off your old mortgage. Depending on the terms of your refinance, you may need to pay closing costs, which can include appraisal fees, title insurance, inspection fees, and loan origination fees. These costs can typically be rolled into the new loan amount or paid upfront.

Why You Should Consider Refinancing: Key Benefits

Lower Interest Rates

One of the most popular reasons to refinance is to secure a lower interest rate. If interest rates have dropped since you took out your mortgage or if your credit score has improved, refinancing can help you reduce the amount you pay in interest over the life of the loan, ultimately lowering your monthly payments.

Shorten Your Loan Term

If you can afford to make higher monthly payments, refinancing to a shorter loan term, such as 15 years instead of 30 years, can save you money in the long run. Although your monthly payment will increase, you’ll pay off the loan faster and pay significantly less in interest over the life of the mortgage.

Access Home Equity

Through a cash-out refinance, you can access the equity in your home to fund projects like home renovations or pay off high-interest debt. This is a great option if you need cash for significant expenses but don’t want to take on additional debt in the form of credit cards or personal loans.

Change Your Loan Type

Refinancing also gives you the opportunity to switch from an adjustable-rate mortgage (ARM) to a fixed-rate mortgage. If you’re worried about your interest rate rising in the future, a fixed-rate mortgage can provide stability and predictability for your monthly payments. Conversely, if you expect interest rates to decrease, you might consider switching to an ARM to take advantage of lower rates.

When is the Best Time to Refinance?

1. Interest Rates Have Dropped

If interest rates are significantly lower than your current rate, refinancing can allow you to lock in savings. Ideally, you should aim for a 1% drop in your interest rate, as this can lead to substantial savings over the life of the loan. Keep an eye on the market, and use a refinance calculator to see how much you could save.

2. Your Credit Score Has Improved

If your credit score has improved since you first took out your mortgage, refinancing can help you qualify for better terms. A higher credit score can lower your interest rate, making it a great time to refinance if you’re looking to save money.

3. You Want to Pay Off Your Loan Faster

If you’re looking to pay off your mortgage faster and have the ability to afford higher monthly payments, refinancing to a shorter loan term can help you save on interest and eliminate debt sooner. This is ideal for those who are financially stable and want to accelerate their homeownership.

4. You Need Cash for Home Improvement or Debt Consolidation

If you’ve built up equity in your home, a cash-out refinance could be a good option to access that equity for major expenses, such as home improvements or paying off high-interest debt. Be mindful of the risks of taking out too much equity, as it can impact your financial stability.

Conclusion: Is Refinancing Right for You?

Mortgage refinancing can be an excellent financial strategy if used correctly. Whether you’re looking to lower your interest rate, access home equity, or change the terms of your loan, refinancing offers several opportunities to improve your financial situation. However, it’s important to consider the costs, potential risks, and timing before making a decision.

By understanding the refinancing process, evaluating your financial goals, and shopping around for the best rates, you can make an informed decision about whether refinancing is the right choice for you. Always weigh the pros and cons, and consider speaking with a financial advisor or mortgage professional to ensure that refinancing aligns with your long-term financial plans.