Online lenders have changed how people borrow money by making the lending process faster, more convenient, and easier to access from anywhere. Instead of visiting a bank branch, borrowers can compare offers, submit an application, upload documents, and often receive a decision entirely online. For people who value speed and flexibility, digital lending platforms have become a major part of today’s borrowing landscape.

What Are Online Lenders?

Online lenders are financial companies that provide loans through digital platforms rather than relying mainly on physical branches. Some are financial technology firms built specifically for online borrowing, while others are traditional lenders that now offer fully digital applications and account management.

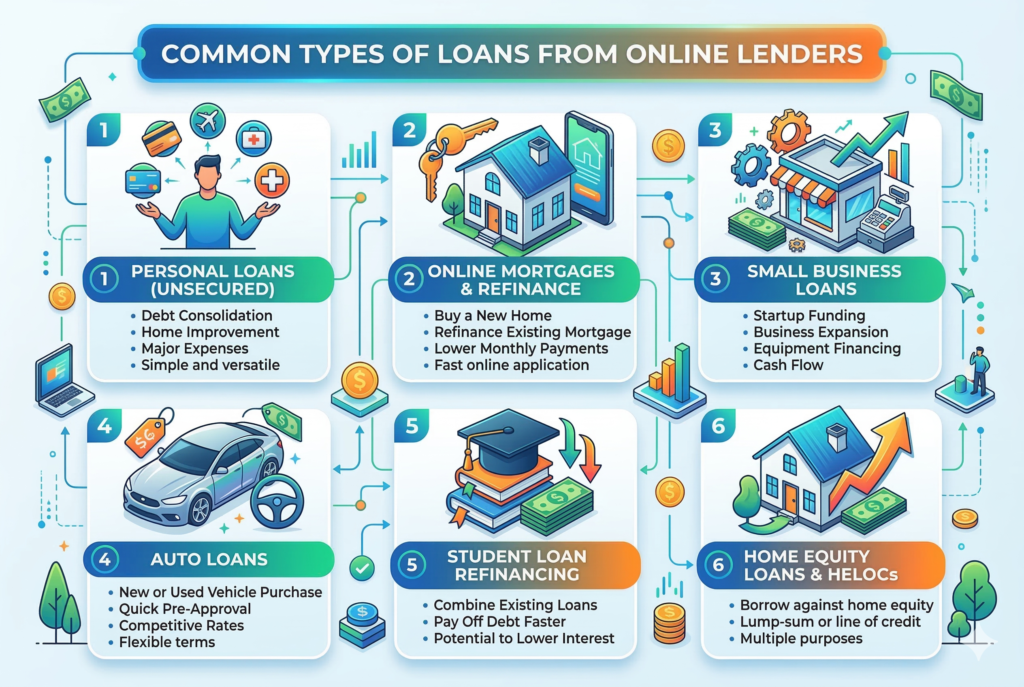

These lenders may offer several types of financing, including personal loans, business loans, auto refinancing, student loan refinancing, and in some cases mortgages or home improvement loans. Their main appeal is convenience. Borrowers can usually start the process on a phone or laptop, review rates, and move forward without in-person appointments.

In many cases, online lenders use automated systems to review applications, assess risk, and verify information. That automation is one reason approval decisions can come faster than with more traditional lending channels. A faster process can help save time, but approval isn’t guaranteed, and each loan offer needs careful review. The details still matter.

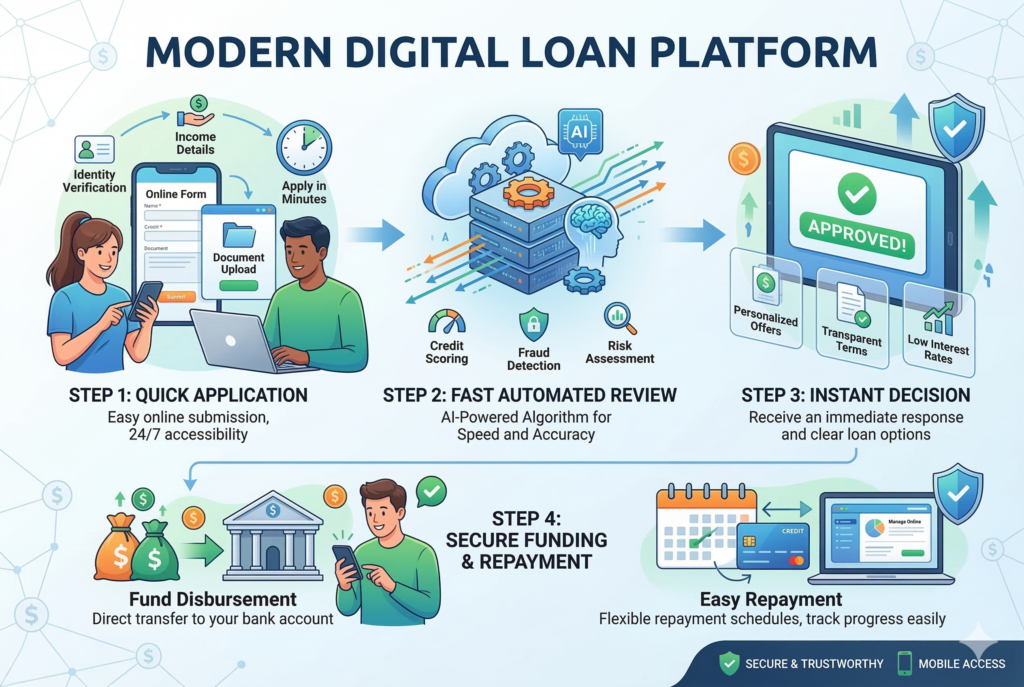

How Digital Loan Platforms Work

A digital loan platform typically starts by asking for basic information such as income, employment status, credit profile, loan purpose, and desired loan amount. Some platforms let borrowers check potential rates through prequalification, which can provide an estimated offer before submitting a full application.

Once a borrower moves ahead, the lender may request more documentation. This can include proof of identity, bank statements, pay stubs, tax records, or employment verification. After review, the lender may approve, deny, or ask for additional information before making a final decision.

If the loan is approved, the borrower receives a loan agreement that outlines the interest rate, repayment term, monthly payment, fees, and any penalties or special conditions. After acceptance, funds are often sent by direct deposit. Depending on the lender and the borrower’s financial profile, funding may happen quickly, sometimes within one business day, though timing varies. This process appeals to people who want more control and visibility. Instead of waiting for branch appointments or phone callbacks, they can often track the application online and review documents on their own schedule.

Why Online Lenders Often Offer Faster Approval

One of the biggest reasons people consider online lenders is speed. Traditional loan processes can involve manual paperwork, branch visits, and longer underwriting timelines. Digital lenders reduce much of that friction.

Automated verification tools help speed up identity checks, income review, and risk analysis. Many online platforms are designed to handle large volumes of applications efficiently, which allows them to respond faster than lenders that rely heavily on manual review. Some also use advanced technology to evaluate borrowers using a broader mix of data points.

For borrowers facing urgent expenses such as medical bills, emergency repairs, moving costs, or debt consolidation needs, that speed can be valuable. A faster approval process may help them access funds before a financial problem becomes worse. Still, speed shouldn’t be the only factor. Quick funding is useful, but borrowers also need to evaluate total borrowing cost, repayment terms, lender reputation, and whether the loan truly fits their financial situation.

Flexible Borrowing Options and Loan Structures

Another reason online lenders stand out is flexibility. Many digital platforms offer a wider range of loan sizes, repayment terms, and qualification models than borrowers expect. Some cater to people with strong credit who want competitive rates, while others serve borrowers with fair or limited credit histories.

Flexibility can show up in several ways. A borrower may be able to choose from multiple repayment periods, which affects both monthly payment size and total interest cost. Some platforms offer secured and unsecured loan options. Others focus on niche uses such as weddings, home upgrades, medical financing, or consolidating existing debt.

This flexibility can be helpful, but it can also make comparison more important. A longer loan term may lower the monthly payment, yet it can increase the total amount paid over time. A lender that advertises easy approval may charge much higher rates or additional fees. Borrowers need to look beyond convenience and review the full picture.

Types of Loans Commonly Offered by Online Lenders

Many online lenders specialize in personal loans, which are often used for debt consolidation, emergency expenses, large purchases, or planned costs that borrowers don’t want to place on a credit card. These loans are usually unsecured, meaning they don’t require collateral, though approval and rate terms depend heavily on creditworthiness.

Some online lenders also provide small business funding, which may help entrepreneurs cover inventory, equipment, marketing, or short-term operating costs. Others focus on refinancing, helping borrowers replace existing loans with new terms that may better fit their budget. You’ll also find online platforms for installment loans, lines of credit, and specialized financing products. The variety is one reason digital lending has grown so quickly. Borrowers aren’t limited to one standard format, and that creates more room to find a product aligned with specific needs.

Benefits of Using an Online Lender

The most obvious benefit is convenience. Borrowers can compare loan offers without visiting multiple institutions, and that saves time. Many platforms are available around the clock, which helps people apply outside traditional banking hours.

Another advantage is transparency, at least with reputable lenders. Many digital platforms clearly show estimated rates, repayment examples, and loan amounts during the shopping process. This makes it easier to compare offers before committing.

Online lenders may also be more accessible for borrowers who live far from bank branches or prefer managing finances digitally. For people comfortable with online banking, electronic signatures, and mobile document uploads, the experience can feel much more efficient. There’s also a broader market effect. Because borrowers can compare lenders more easily online, competition can encourage better offers, clearer pricing, and more specialized loan products. That doesn’t guarantee the lowest cost, but it often gives borrowers more choices than they’d have by relying on one local institution alone.

Risks and Drawbacks Borrowers Shouldn’t Ignore

Despite the convenience, online lenders aren’t automatically the best option for everyone. Some charge high APR, origination fees, late fees, or other costs that make the loan more expensive than it first appears. Others market heavily to borrowers who need fast cash, knowing urgency can lead people to overlook the fine print.

There’s also the issue of legitimacy. Not every website offering a loan is trustworthy. Borrowers need to be careful with personal information and watch for warning signs such as guaranteed approval, pressure tactics, upfront payment demands, or vague company details. A legitimate lender should clearly disclose rates, terms, fees, and contact information. Another drawback is the lack of face-to-face support. Some borrowers prefer speaking with someone directly, especially when making a major financial decision. While digital service can be efficient, it may not feel as reassuring for people who want hands-on guidance.

How to Compare Online Loan Offers Wisely

Comparing online loan offers takes more than looking at the advertised rate. Borrowers should review the full loan terms, including APR, monthly payment, repayment period, total repayment cost, origination fee, and any penalties.

It’s also wise to check whether a lender offers prequalification, because that can help borrowers compare estimated terms without committing to a hard credit inquiry right away. Reading customer reviews, checking lender credentials, and understanding how support works are also important steps.

Borrowers should ask a practical question before accepting any offer: does this loan solve a real financial need without creating a larger one later? A fast approval can feel like a solution at the moment, but the long-term payment obligation deserves equal attention.

Who Might Benefit Most from Online Lenders?

Online lenders can be a strong fit for borrowers who want a streamlined application process, need funds relatively quickly, or prefer digital financial tools. They may also appeal to people comparing multiple lenders at once, especially for debt consolidation or planned expenses.

They can be useful for borrowers with solid credit who are looking for competitive rates, but they may also serve people whose financial profiles don’t fit a traditional bank’s narrow lending model. Even so, suitability depends on the specific lender, loan product, and repayment terms.

For many households, the best use of an online loan is strategic rather than impulsive. Borrowing works best when it supports a clear plan, whether that means consolidating high-interest debt, covering a necessary expense, or financing a cost with predictable repayment.

Conclusion

Online lenders have made borrowing faster and more flexible by moving much of the loan process onto digital platforms. They can offer quick applications, fast decisions, convenient funding, and a wide range of borrowing options for different financial needs. At the same time, borrowers shouldn’t assume speed equals value. The smartest approach is to compare offers carefully, review fees and repayment terms, and choose a lender with strong transparency and credibility. When used thoughtfully, online lending can be a practical tool that gives borrowers more access, more convenience, and more control over how they finance important expenses.