Finding your apartment broken into or your car window smashed is frightening. After the shock, the next question usually comes fast: will renters insurance cover stolen items, or are you stuck replacing everything yourself?

In many cases, renters insurance theft coverage can help. Standard renters insurance usually covers stolen personal belongings under personal property coverage, whether the theft happens inside your apartment or away from home. However, the payout depends on your deductible, policy limits, replacement cost versus actual cash value coverage, and special limits for high-value items such as jewelry or electronics.

How Renters Insurance Theft Coverage Works

Renters insurance covers your personal belongings, not the building itself. Your landlord’s insurance protects the structure, but your renters policy protects items you own, such as clothing, furniture, electronics, bikes, small appliances, books, and household goods. If someone breaks into your apartment and steals your laptop, camera, TV, or clothes, your personal property coverage may reimburse you after your deductible. For example, if $2,000 worth of belongings are stolen and you have a $500 deductible, your payout may start around $1,500 before depreciation or policy limits are applied.

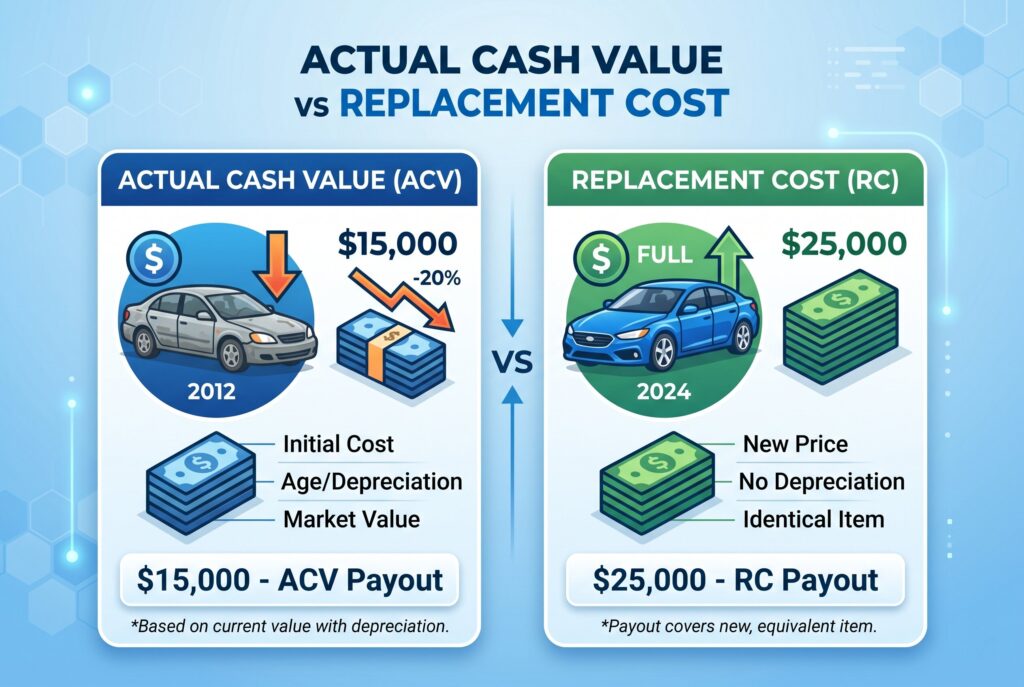

Actual Cash Value vs Replacement Cost

The biggest payout difference is actual cash value vs replacement cost. Actual cash value pays what the item was worth at the time of theft after depreciation. Replacement cost pays the cost to buy a similar new item, up to your policy limits. If your five-year-old laptop is stolen, actual cash value may pay far less than what a new laptop costs today. Replacement cost coverage usually costs more, but it’s often worth it if you own electronics, furniture, bikes, or work equipment you couldn’t easily replace out of pocket.

Car Break-Ins vs Car Theft

Does Renters Insurance Cover Car Break Ins?

Yes, renters insurance may cover belongings stolen from your car. If someone breaks your window and steals your laptop, backpack, phone charger, jacket, or suitcase, those items may fall under off-premises personal property coverage. However, your auto insurance, not renters insurance, would usually handle damage to the vehicle itself, such as broken glass or a damaged door lock. You may need two claims if both the car and belongings were damaged or stolen.

Does Renters Insurance Cover Car Theft?

No. Renters insurance doesn’t cover the theft of the car itself. If your whole vehicle is stolen, you need comprehensive auto insurance. This distinction matters because many renters assume “theft coverage” means any theft. Renters insurance protects your belongings. Auto insurance protects the vehicle.

High-Value Items: The Sublimit Trap

Some items have special theft limits, even if your total personal property limit is much higher. These limits are called sublimits.

Item Type | Common Theft Limit Concern |

|---|---|

Jewelry and watches |

|

Cash |

|

| |

| |

Collectibles |

|

Electronics |

|

If you own expensive jewelry, firearms, watches, musical instruments, collectibles, or a high-end bike, ask about scheduled personal property coverage. This endorsement can raise the limit for specific valuables.

Does Renters Insurance Cover Burglary?

Yes, renters insurance often covers burglary if someone breaks into your apartment and steals covered belongings. You will usually need proof of the loss, such as a police report, photos, receipts, serial numbers, or a home inventory. Burglary damage to your personal belongings may be covered, but damage to the building, like a broken apartment door, may be handled by the landlord or building owner. Your policy mainly follows what you own.

What Renters Insurance Doesn’t Cover After a Theft

Your Roommate’s Belongings

Your policy usually covers your belongings, not your roommate’s. Unless your roommate is named on your policy, they may need their own renters insurance. This is one of the most common apartment insurance cover theft misunderstandings. Sharing a lease doesn’t always mean sharing insurance coverage.

Cash Beyond the Policy Limit

Renters insurance may cover stolen cash, but the limit is usually low. Keeping large amounts of cash at home is risky because proving the amount can be difficult and reimbursement may be capped.

Theft You Can’t Document

Insurers need evidence. If you can’t show that you owned the item or that it was stolen, your claim may become harder. Receipts, photos, bank statements, app purchase history, product boxes, and serial numbers all help.

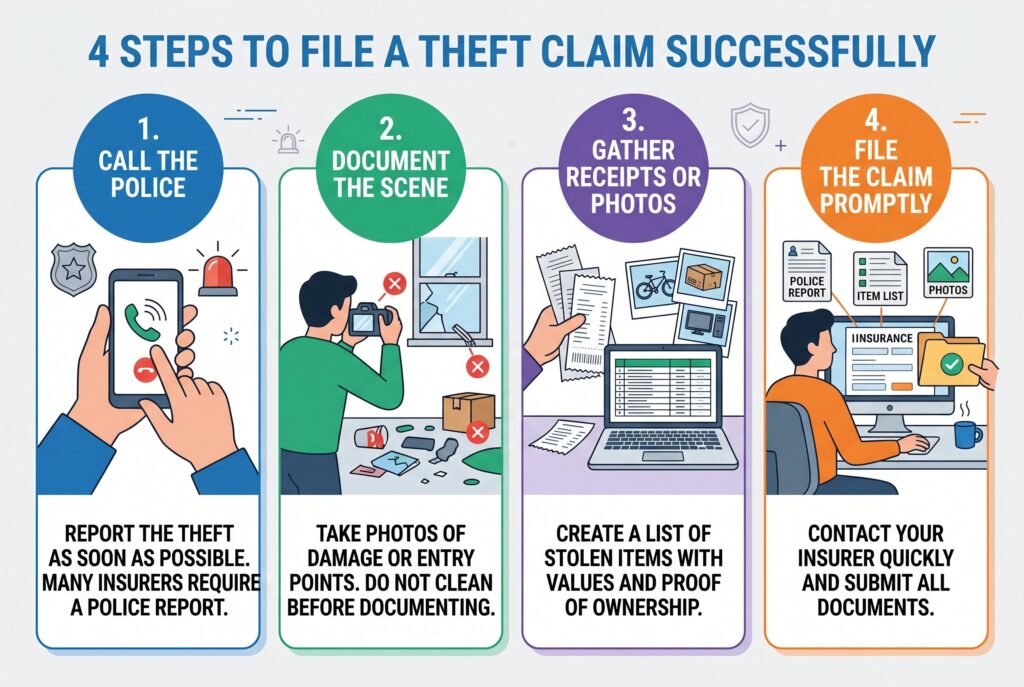

4 Steps to File a Theft Claim Successfully

1. Call the Police

Report the theft as soon as possible. Many insurers require a police report before paying a theft claim, especially for burglary, stolen electronics, bikes, cash, or valuables.

2. Document the Scene

Take photos of broken locks, damaged windows, emptied drawers, missing bike locks, or car break-in damage. Don’t clean everything up before documenting it.

3. Gather Receipts or Photos

Create a list of stolen items with estimated value, purchase dates, brand names, model numbers, and serial numbers if available. Photos from your phone, emails, and online receipts can help prove ownership.

4. File the Claim Promptly

Contact your insurer quickly and submit the police report, item list, photos, and supporting documents. Ask whether your claim will be paid at actual cash value first and replacement cost later after you buy replacements.

Final Thoughts

Renters insurance can be one of the most valuable protections after theft, but only if you understand the limits before something happens. The answer for “will renters insurance cover stolen items” is often yes, but the details matter. It may cover stolen items from your apartment, car, storage unit, or while traveling, but it doesn’t cover a stolen car, your roommate’s belongings, or every high-value item at full value. Review your personal property limit, deductible, off-premises coverage, and sublimits now. It’s important to remember that theft coverage is strongest when your policy matches what you actually own.