Buying your first car can feel exciting, but it can also become expensive fast if you walk into a dealership without a plan. As a first-time car buyer, the biggest mistake isn’t choosing the wrong color or trim. It’s focusing only on the monthly payment and ignoring the full cost of ownership.

A smart first-time car buyer guide starts with two rules. Your car payment should stay under 10% of your take home pay, and your total car costs should ideally stay under 20%. Total costs include insurance, fuel, maintenance, registration, repairs, parking, and loan interest. If those numbers don’t work, the car isn’t affordable yet.

First-time car buyer programs can help if you have limited credit, no credit, or a short employment history. These programs may come from automakers, credit unions, banks, or dealerships, and they often look at income, job stability, school status, and down payment rather than only your credit score. Before you fall in love with a vehicle, know your budget, get preapproval, compare new and used options, and negotiate the out the door price instead of the monthly payment.

Why First-Time Car Buyers Often Overpay

Many first-time buyers overpay because they start shopping before they understand the numbers. A dealership may ask, “What monthly payment are you looking for?” That sounds helpful, but it can lead you into a deal that looks affordable on the surface and expensive underneath.

A low monthly payment can hide:

- A longer loan term

- A higher interest rate

- Extra dealer add-ons

- Rolled-in taxes and fees

- Negative equity risk

For a first-time car buyer, the goal is not just to get approved. The goal is to buy a car you can afford after insurance, fuel, maintenance, registration, repairs, parking, and loan interest are included.

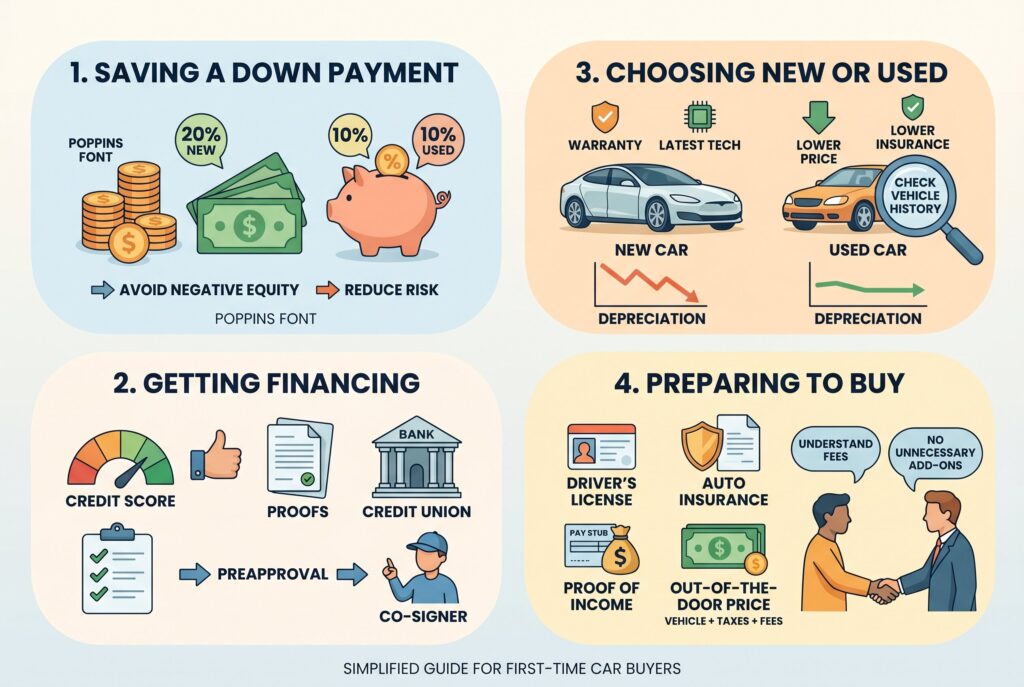

Step 1: The Brutal Math of How Much Down Payment for a Car

Many first-time buyers wonder how much down payment they need for a car. A good rule is 20% down for a new car and at least 10% down for a used car. For example, a $25,000 new car would ideally require a $5,000 down payment, while a $15,000 used car would need at least $1,500 down.

A down payment does more than help you get approved. It reduces your loan balance and lowers the risk of negative equity, which occurs when you owe more than the car is worth. While zero-down financing may seem attractive, it often leads to higher monthly payments, more interest, and greater financial risk. The best approach is to put down as much as you can without draining your emergency savings. Even a modest down payment can make your loan more manageable and affordable.

Step 2: Securing a First Time Car Buyer Program

A first-time car buyer program can help people with limited or no credit history qualify for financing. These programs are often available through automakers, credit unions, and banks, and may consider factors like income, employment stability, and down payment rather than focusing solely on credit scores. To improve your approval chances, prepare documents such as proof of income, pay stubs, proof of address, and a valid driver’s license. If you have a thin credit file, a co-signer may also help. Before visiting a dealership, consider getting auto loan preapproval. Preapproval gives you a clear loan budget, estimated APR, and stronger negotiating power when comparing financing offers.

Step 3: New vs Used: Escaping the Depreciation Trap

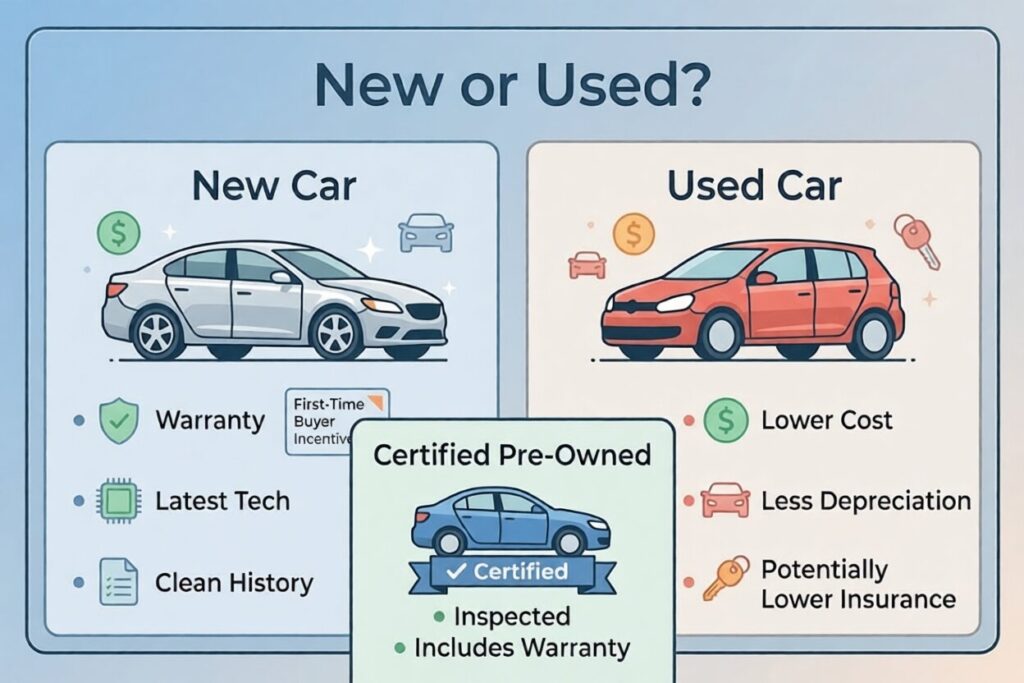

For most first-time buyers, a used car is often the better financial choice. Used vehicles typically cost less, have lower insurance premiums, and avoid the steep depreciation that affects new cars during their first few years. A certified pre-owned vehicle can offer a balance of affordability and added protection through inspections and limited warranty coverage. Before buying a used car, review the vehicle history report, verify the title and VIN, check maintenance records, and consider an independent mechanic inspection. Taking these steps can help you avoid costly surprises after purchase.

Step 4: What Do You Need to Buy a Car?

Before visiting a dealership, make sure you have the required documents, including your driver’s license, proof of insurance, proof of income, proof of residence, and a preapproval letter if applicable. If you’re trading in a vehicle, bring the title, registration, and loan payoff information. When it’s time to discuss financing, focus on the out-the-door price rather than the monthly payment. The out-the-door price includes the vehicle cost, taxes, registration, and dealer fees, giving you a clearer picture of what you’ll actually pay. Be cautious with add-ons such as extended warranties, service contracts, or paint protection, as they can significantly increase the total cost of the purchase.

New or Used: What Should a First-Time Car Buyer Choose?

A new car may feel safer because it comes with a warranty, newer technology, and a clean vehicle history. Some new vehicles may also qualify for promotional financing or first-time buyer incentives. However, new cars usually lose value quickly, especially during the first few years. For a first-time car buyer, that can be risky if your down payment is small or your loan term is long.

A used car is often the smarter financial choice because it usually costs less, may have lower insurance premiums, and has already gone through the steepest part of depreciation. A certified pre-owned vehicle can be a good middle ground. It may cost less than a new car while still offering inspection standards and warranty protection.

Conclusion

Your first car doesn’t need to be your dream car. It needs to be reliable, affordable, insurable, and realistic for your income. A good first time car buyer doesn’t rush because a salesperson says the deal ends today. They calculate total cost, compare lenders, save a down payment, use first time car buyer programs wisely, and walk away when the math doesn’t work.

Before signing, ask yourself one final question: can I afford this car even after insurance, fuel, repairs, and emergencies? If the answer isn’t clear, pause. A better deal, a better car, or a better loan will come. The goal is simple. Buy transportation that moves your life forward without trapping your future in debt.