Getting married often means combining finances, sharing responsibilities, and looking for ways to reduce household expenses. When it comes to car insurance for married couples, the short answer is yes, marriage can often lower your insurance costs. Industry data consistently shows that married drivers are generally viewed as lower risk than single drivers. As a result, many insurers apply a married driver discount that can reduce premiums by approximately 5% to 10%, with average annual savings often reaching around $149 per year compared to single, divorced, or widowed drivers.

The savings can become even larger when couples combine policies through a joint car insurance arrangement and add an auto and renters insurance bundle or homeowners coverage. However, combining policies isn’t always the smartest financial move. If one spouse has multiple accidents, serious traffic violations, poor credit, or a DUI history, a joint policy could increase costs for both partners. Understanding when to combine coverage and when to stay separate is the key to protecting your household budget in 2026.

The Algorithm: Why Do Married Drivers Pay Less?

Many drivers wonder why insurance companies seem to favor married people when calculating premiums. The answer comes down to risk assessment.

Insurance companies don’t create rates based on assumptions. They rely on decades of claims data. Historical data suggests that married drivers tend to file fewer claims, engage in fewer risky driving behaviors, and maintain more stable financial habits than single drivers. While every individual is different, insurance pricing models focus on trends across large populations. Because of these patterns, insurers often classify married policyholders as a lower risk group. Once your marital status changes from single to married, many carriers automatically reevaluate your profile and may offer lower premiums.

This doesn’t mean every married person will instantly receive cheaper coverage. Age, driving record, location, vehicle type, annual mileage, credit history in eligible states, and previous claims still play major roles. However, marital status often serves as another positive factor within the overall pricing formula. For many households, the combination of a married driver discount and policy consolidation creates meaningful savings over time.

Car Insurance After Marriage: What Should You Update?

One common mistake newlyweds make is assuming marriage automatically updates their insurance records. It doesn’t. Car insurance after marriage requires active updates. If you recently got married, there are several areas that deserve immediate attention.

- First, notify your insurance company about your marital status change. Many insurers can reassess rates and determine whether discounts now apply.

- Second, review vehicle ownership. If both spouses regularly drive the same cars, a shared car insurance policy may provide better value and simpler management.

- Third, evaluate whether combining policies makes financial sense. Some couples save significantly by merging coverage, while others benefit from maintaining separate policies.

- Finally, review other insurance products. An auto and renters insurance bundle may unlock additional discounts that aren’t available when policies remain with separate providers.

The goal is creating the most efficient protection strategy for your household.

Unmarried Couples: Can You Still Get a Joint Policy?

A common misconception is that only married couples can share insurance coverage. In reality, many insurers also offer options for car insurance for unmarried couples and domestic partners. Most companies focus on practical living arrangements rather than legal relationship status. If two people share a residence and regularly drive each other’s vehicles, they may qualify for a shared policy structure.

Typically, insurers look for two primary conditions.

- First, both individuals must reside at the same address. This same address car insurance requirement helps insurers evaluate vehicle usage patterns and household risk.

- Second, both drivers must have a legitimate insurable interest in the vehicles or regularly operate them.

For cohabiting couples, domestic partner car insurance can provide many of the same advantages that married couples enjoy, including simplified billing, consolidated management, and potential multi vehicle discounts. However, eligibility requirements vary by state and insurer, so couples should verify specific rules before making changes.

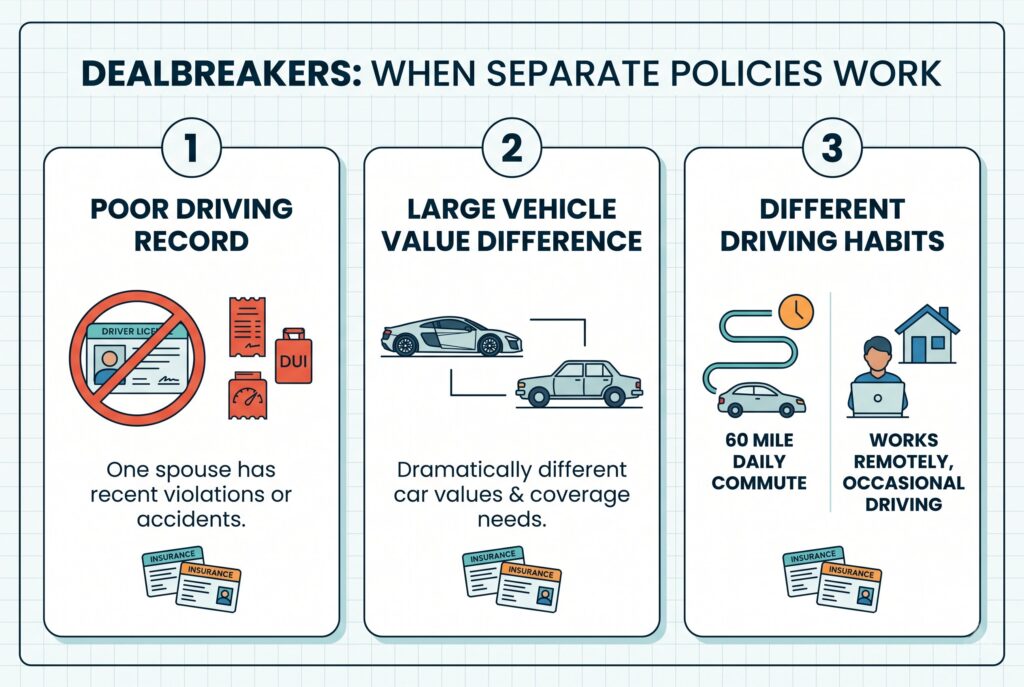

The Dealbreakers: When Keeping Separate Policies Makes More Sense

Many articles focus exclusively on savings. The reality is more nuanced. Sometimes separate car insurance policies for married couples produce better financial results than combining everything under one account.

One Partner Has a Poor Driving Record

This is the most common dealbreaker. If one spouse recently received a DUI, accumulated multiple speeding tickets, or caused several at fault accidents, combining policies may expose the lower risk spouse to significantly higher premiums. In these situations, maintaining separate coverage can sometimes protect the stronger driver’s favorable pricing.

Large Vehicle Value Differences

Imagine one spouse drives an older sedan worth $6,000 while the other owns a luxury performance vehicle worth $90,000. The insurance needs are dramatically different. The higher value vehicle may require extensive comprehensive and collision coverage, increasing the total household premium. Depending on the insurer, combining these vehicles under one policy may not generate enough savings to offset the added costs.

Different Driving Habits

One spouse may commute 60 miles daily while the other works remotely and drives only occasionally. These usage patterns can affect pricing significantly. Separate policies sometimes provide more accurate risk based pricing.

Risk Isolation: Understanding the Excluded Driver Option

One of the most overlooked tools in household insurance planning is the excluded driver designation. An excluded driver is a person specifically removed from coverage under a policy. In certain states, insurers allow policyholders to exclude a high risk spouse or household member. For example, if your partner has a history of serious violations, you may be able to request that they be listed as an excluded driver on your policy. This strategy can help preserve lower rates for the primary policyholder. However, there is a major restriction.

If an excluded driver operates the insured vehicle and causes an accident, the insurer will generally deny coverage for that loss. Because of this, excluded driver arrangements require careful planning and strict compliance. State rules, marital status insurance regulations and excluded driver laws vary considerably, so professional guidance is essential before making this decision.

Maximizing Savings Beyond Marriage

Marriage alone isn’t the only path to lower premiums. Couples should also explore multi policy opportunities. Many insurers offer significant discounts through bundle renters and auto insurance programs. Others provide additional savings when homeowners, umbrella policies, motorcycles, boats, or recreational vehicles are added to the relationship.

The best approach is conducting a complete insurance audit after moving in together or getting married.

- Review every vehicle.

- Review every driver.

- Review every deductible.

- Review every discount.

The cumulative effect of multiple small adjustments can often generate larger savings than marital status alone.

Conclusion

Car insurance for married couples can absolutely provide lower rates, but combining policies shouldn’t be an automatic decision. Marriage often unlocks discounts because insurers view married drivers as statistically lower risk. Joint policies, shared car insurance policy structures, and auto and renters insurance bundle opportunities can all contribute to meaningful long term savings.

At the same time, every household has unique risks. A spouse with a poor driving record, significant claims history, or expensive vehicle can completely change the financial equation. Before combining coverage, review both driving records carefully, compare joint and separate quotes, understand excluded driver options where available, and evaluate all available discounts. The smartest couples don’t simply merge policies because they’re married. They analyze the numbers, understand the risks, and build an insurance strategy that protects both their vehicles and their household finances for years to come.