Many drivers concern what age does car insurance go down and expect retirement to bring the cheapest rates of their life. The truth is more complicated. Car insurance for seniors usually follows a U-shaped pattern. Drivers in their 50s and early 60s often enjoy some of the lowest premiums because they have decades of experience, stable driving habits, and fewer risky behaviors. Average full coverage rates may sit around $2,274 to $2,425 per year for many drivers in this age range.

After age 70, however, senior car insurance can start rising again. Insurers may view older drivers as higher risk because vision, reaction time, injury severity, and medical costs can change with age. That doesn’t mean every senior is unsafe. It means insurance pricing is based on broad risk patterns, not only your personal confidence behind the wheel.

The best response isn’t to accept higher bills quietly. Auto insurance for seniors can still be reduced through defensive driving discounts, low mileage programs, pay per mile insurance, mature driver discounts, bundling, and smarter coverage choices.

The Senior Rebound: Why Do Rates Jump at Age 70?

If you have a clean driving record after 40 years on the road, a sudden premium increase can feel unfair. You may wonder, does car insurance increase with age even when you haven’t had accidents? In many cases, yes.

Insurance companies price policies using large pools of claims data. While experienced drivers are often safer through middle age, the risk curve can shift after 70. Older drivers may drive more carefully, but accidents can become more expensive when they happen. Injuries may be more serious, recovery may take longer, and medical payments may cost more. That added claim severity can push premiums upward.

This is why car insurance rates for seniors often remain attractive around ages 55 to 65, then rise as drivers enter their 70s and 80s. The change isn’t usually instant on your birthday. It often appears at renewal when the insurer recalculates your risk profile. Still, age is only one factor. Your ZIP code, vehicle type, mileage, credit history where allowed, claim record, coverage limits, and deductible can all matter. A 72 year old who drives 4,000 miles a year in a safe sedan may pay less than a 62 year old with recent accidents and a high value SUV.

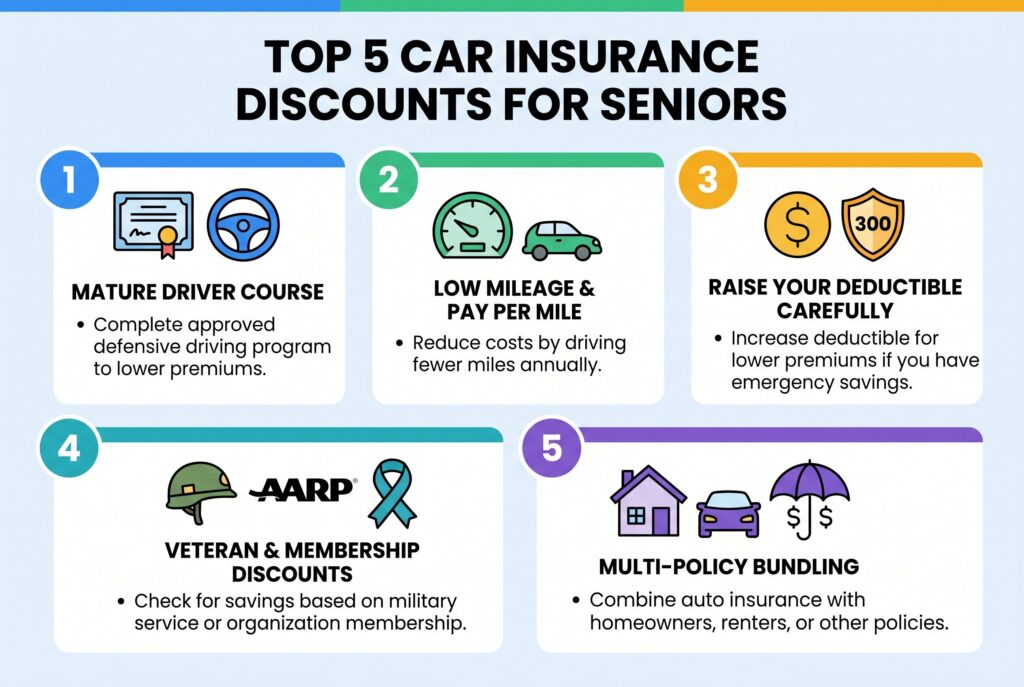

Top 5 Car Insurance Discounts for Seniors

1. Mature Driver Course

A mature driver discount is one of the most practical savings tools for older drivers. Many states and insurers reward seniors who complete an approved defensive driving course. Programs like AARP Smart Driver may help refresh safe driving habits and can sometimes reduce premiums for several years. These courses often cover reaction time, road scanning, medication awareness, night driving, intersection safety, and how to adjust driving habits as your body changes. Even confident drivers can benefit because the course proves to the insurer that you’re actively managing risk.

2. Low Mileage and Pay Per Mile Insurance

Retirement changes how you use your car. If you no longer commute daily, you shouldn’t be priced like someone driving through rush hour every morning. Low mileage car insurance can reward seniors who drive fewer miles.

Pay per mile insurance may be even better for some retirees. With this model, your premium is partly based on how much you actually drive. If you only use the car for groceries, medical appointments, church, family visits, or short errands, a mileage based plan can cut costs significantly. Before switching, review privacy rules and tracking requirements. Some programs use a device or app to measure mileage and sometimes driving behavior. The savings can be real, but you should understand what data is collected.

3. Raise Your Deductible Carefully

Raising your deductible can lower your premium, but it should be done with discipline. Moving from a $500 deductible to a $1,000 deductible may reduce your bill, but it also means you need enough emergency savings to cover the higher out of pocket cost after a claim. This strategy works best for seniors with stable savings and a low claim history. It isn’t ideal if paying $1,000 suddenly would create financial stress.

4. Veteran and Membership Discounts

Some seniors qualify for veteran car insurance discounts, retired military discounts, government employee savings, or membership based discounts. If you served in the military, worked in public service, belong to a senior organization, or are part of a professional association, ask directly. Insurers don’t always apply discounts automatically. A five minute call can reveal savings that have been sitting unused for years.

5. Multi Policy Bundling

Bundling remains one of the strongest ways to reduce senior driver insurance costs. If you have homeowners, renters, condo, umbrella, motorcycle, or life insurance, ask whether placing multiple policies with one company lowers your total bill. The key is comparing the final combined price. A bundle is only useful if both the auto policy and the other policy remain competitive.

Trimming the Fat: Do You Still Need Full Coverage?

As cars age, many seniors start looking for ways to reduce insurance costs. One area worth reviewing is your coverage. If you’re driving an older vehicle that has been paid off, full coverage may not always provide enough value to justify the extra cost. Collision coverage pays for damage to your car after a crash. Comprehensive coverage pays for non collision events such as theft, vandalism, hail, fire, or falling objects. These protections are valuable, but they become less efficient when the vehicle value drops.

A common rule of thumb is this: if the annual cost of collision and comprehensive coverage is more than about 10% of the car’s current value, consider whether keeping them makes sense. For example, if your car is worth $4,000 and extra physical damage coverage costs $600 per year, you may be paying heavily for limited potential recovery.

That doesn’t mean you should cut everything. Liability coverage protects your assets if you injure someone or damage property. Medical payments or PIP may also matter depending on your state, health coverage, and financial situation. Seniors with retirement savings should be especially careful not to carry liability limits that are too low.

Conclusion

Senior car insurance should never be left on autopilot. Loyalty doesn’t always produce the best price, and insurers don’t all rate age, mileage, vehicles, or discounts the same way.

Review your policy every year before renewal. Ask about a defensive driving course discount, low mileage savings, pay per mile insurance, mature driver discount, bundling, veteran discounts, and deductible options. Then compare at least three quotes using the same coverage limits so you can judge the real value. The goal isn’t simply finding cheap car insurance for seniors. It’s finding coverage that protects your income, your vehicle, your health, and your retirement savings without wasting money. With the right strategy, getting older doesn’t have to mean losing control of your insurance bill.