The requirements for buying a car vary depending on whether you’re paying cash, financing the purchase, or trading in an existing vehicle. For most dealership purchases, you’ll need four core items: a valid driver’s license, proof of auto insurance, a payment method, and proof of income if you’re financing. These documents help the dealer confirm your identity, prepare the sale contract, verify that the vehicle can legally leave the lot, and prove to a lender that you can repay the loan.

However, the checklist gets longer if you’re self-employed, using a co-signer, buying from a private seller, purchasing out of state, or trading in a car that still has a loan. Preparing everything before you leave home can save hours at the dealership and prevent the frustrating moment when a missing utility bill, title, or insurance card delays your keys.

The Core Documents Needed to Buy a Car

A Valid Driver’s License

Your driver’s license is typically the first document a dealership will request. Beyond proving your identity, it confirms that you’re legally permitted to operate a motor vehicle. Most dealers require a current, government-issued license that matches the name on the purchase contract and financing application.

An expired license can create problems even if you’re otherwise qualified to buy the car. Some lenders may refuse to finalize financing until a valid license is provided, while others may require additional verification documents. If you’ve recently moved and the address on your license is outdated, be prepared to provide supplementary proof of residence, such as a utility bill, lease agreement, or recent bank statement.

It’s also important to understand that a driver’s license and a state-issued identification card are not always treated the same way. While an ID card may verify identity, it does not demonstrate driving privileges, which can complicate the transaction depending on the dealership and lender.

Proof of Auto Insurance

In most states, you cannot legally drive a newly purchased vehicle without insurance coverage. For that reason, dealerships usually require proof of insurance before releasing the vehicle. Many buyers assume their existing policy automatically covers a newly purchased car, but coverage rules vary by insurer. Some companies provide a temporary grace period, while others require immediate notification before coverage becomes effective. Contacting your insurance provider before visiting the dealership can prevent unexpected delays on delivery day.

If you’re financing the vehicle, insurance requirements become even more important. While state law may only require liability coverage, lenders generally require collision and comprehensive insurance as well. These additional protections help secure the lender’s financial interest in the vehicle until the loan is paid off. As a result, buyers should factor insurance costs into their overall vehicle budget before committing to a purchase.

Proof of Income and Financial Stability

Anyone applying for an auto loan should expect to provide documentation showing a reliable source of income. Lenders want reassurance that the borrower can comfortably manage the monthly payment throughout the life of the loan.

For traditional employees, recent pay stubs are usually sufficient. However, lenders may request additional documentation if income varies significantly from month to month or if employment has recently changed. Self-employed applicants often face stricter verification standards because their income is less predictable. In these situations, lenders may review tax returns, bank statements, or business records to establish a consistent earnings history.

One common mistake is assuming that income alone guarantees approval. Lenders also evaluate factors such as employment stability, existing debt obligations, and overall financial profile. A borrower with moderate income but strong financial management may receive better terms than someone earning more but carrying substantial debt.

Preparing Your Payment Method

Even after choosing a vehicle and securing approval, you’ll still need an acceptable method of payment to finalize the transaction. The payment process varies from one dealership to another, which is why confirming payment policies beforehand can save time and frustration.

Most dealerships readily accept cashier’s checks, certified funds, wire transfers, and financing proceeds from approved lenders. Personal checks, however, are not always accepted, especially for large purchases. Some dealers also limit the amount that can be charged to a credit card or apply processing fees for large transactions. If you’re planning to make a down payment, verify exactly how the dealership wants those funds delivered before arriving to complete the purchase. A simple phone call can prevent last-minute complications that delay registration, financing, or vehicle delivery.

The Financing Hurdle: Proving You Can Pay

Financing adds another layer of paperwork. If you already have a pre-approved loan from a bank or credit union, bring the approval letter, lender contact information, loan terms, and any blank check or funding instructions they provided. This gives you negotiating power because you aren’t fully dependent on dealer financing.

If you’re using dealer financing, bring your proof of income. For most employees, two recent pay stubs may be enough. If you’re self-employed, bring three to six months of bank statements, recent tax returns, and possibly profit and loss records. The goal is to show stable income, not just occasional deposits. You’ll also need proof of residence. A utility bill, lease agreement, mortgage statement, bank statement, or government letter can help verify your address. The name and address should match your application whenever possible.

If you need a co-signer car loan, your co-signer should be present or ready to sign electronically. They’ll usually need their own driver’s license, proof of income, proof of residence, Social Security number, and credit authorization. A co-signer isn’t just a character reference. They become legally responsible if you don’t pay.

The Trade In Puzzle: Unlocking Max Value

If you’re trading in a car, the dealership needs proof that you have the legal right to transfer it. The most important document is the vehicle title. If the car is paid off, the title should show you as the owner with no active lien. If the title is missing, replace it before shopping because the trade in process can slow down dramatically without it. Bring vehicle registration as well. Registration helps confirm that the car is linked to you and legally recorded with the state. If the registration is expired, tell the dealer upfront.

If the car still has a loan, bring payoff information. This includes the lender name, account number, payoff amount, and lender contact details. The dealer needs this information to pay off the remaining balance and calculate your trade equity. Maintenance records can help your value. Receipts for oil changes, tires, brakes, battery replacements, and major repairs show that the vehicle was cared for. Bring all keys, key fobs, the owner’s manual, wheel lock keys, and any accessories that came with the car. Small details can affect the final offer.

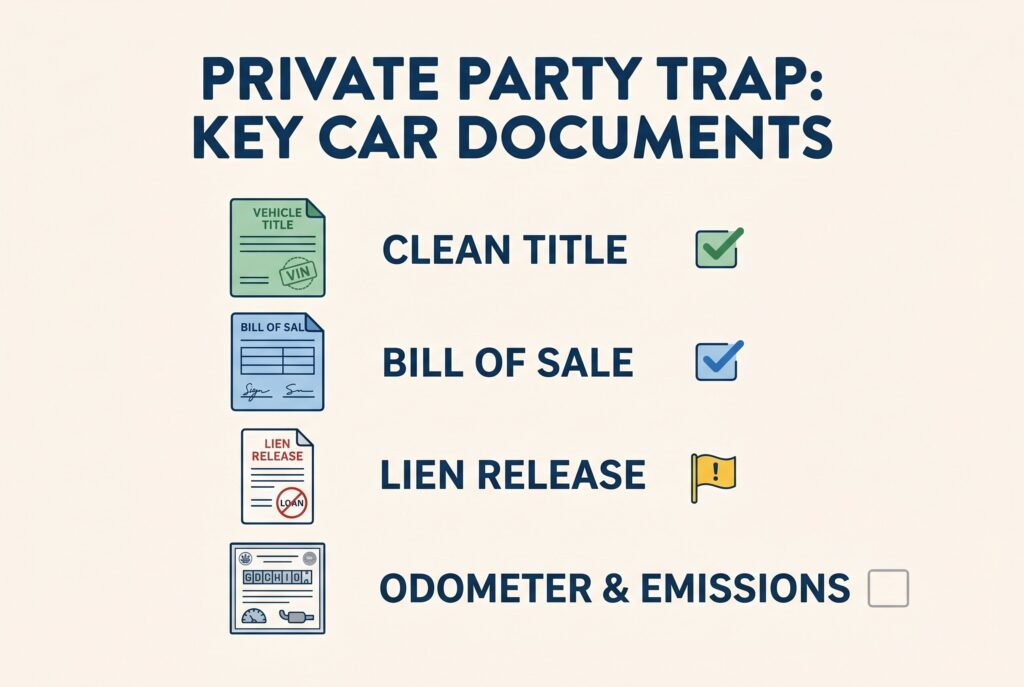

Private Party Trap: Documents Needed When Buying a Used Car

Vehicle Title

The vehicle title is the most important document in a private car sale. It proves who legally owns the vehicle and allows ownership to be transferred to the buyer. Before moving forward, make sure the seller’s name on the title matches the name on their government-issued ID. The VIN listed on the title should also match the VIN on the vehicle, usually found on the dashboard, driver-side door frame, or registration documents.

Be cautious if the seller says the title is missing, held by another person, or still with a bank. These situations may indicate that the seller does not have full legal authority to sell the vehicle. A clean title gives you stronger protection because it shows that the vehicle is not currently branded as salvage, rebuilt, flood-damaged, or subject to another serious ownership issue. If anything about the title looks altered, incomplete, or inconsistent, it is safer to pause the transaction and verify the information with your local DMV.

Bill of Sale

A private bill of sale creates a written record of the transaction between the buyer and seller. This document is especially important in a private-party purchase because it helps prove the sale price, sale date, and terms of the agreement.

A strong bill of sale should include the full names and addresses of both parties, the vehicle year, make, model, VIN, odometer reading, purchase price, date of sale, and signatures from both buyer and seller. It should also clearly state whether the vehicle is being sold “as is.” In most private sales, “as is” means the buyer accepts the vehicle in its current condition and the seller is not responsible for repairs after the sale. Do not rely only on a verbal agreement. If the seller promises to fix something, include that promise in writing before payment is made. Otherwise, it may be difficult to enforce later.

Lien Release

If the vehicle was ever financed, ask whether there is a lien on the title. A lien means a lender or financial institution may still have a legal claim to the car. If the loan has already been paid off, the seller should be able to provide a lien release showing that the lender no longer has an ownership interest in the vehicle. This document matters because an unresolved lien can prevent you from transferring the title into your name. In some cases, you could pay for the car and still be unable to register it properly. If the seller says the loan is paid off but cannot provide proof, contact the DMV or lienholder before completing the purchase.

Odometer Disclosure and State-Specific Documents

Many private used car sales also require an odometer disclosure statement. This document confirms the mileage at the time of sale and helps protect buyers from odometer fraud. Some states include the odometer disclosure directly on the title, while others require a separate form.

Depending on where you live, you may also need an emissions certificate, safety inspection report, temporary registration, smog check, or state-specific transfer form. These requirements vary widely, so check your local DMV website before meeting the seller. Knowing the rules in advance can help you avoid buying a vehicle that cannot be registered right away.

Before paying, make sure the title, bill of sale, VIN, odometer reading, lien status, and state-required forms all match. In a private sale, careful document review is one of your best protections against ownership problems, hidden liens, and registration delays.

Used Car Shopping Checklist: Red Flags to Avoid

- The VIN on the title doesn’t match the VIN on the vehicle. Always compare the VIN listed on the title, registration, and vehicle itself. Any mismatch could indicate title fraud, theft, or clerical errors that may complicate ownership transfer.

- The seller refuses to show a valid government-issued ID. The seller’s name should match the name listed on the vehicle title. If they cannot verify their identity, proceed with caution.

- The seller is pushing for a rushed transaction. Be wary of anyone pressuring you to make an immediate decision, skip paperwork, or pay before verifying ownership details.

- The asking price is dramatically below market value. While good deals exist, prices that seem too good to be true often come with hidden problems such as title issues, undisclosed damage, or scams.

- The title is missing, incomplete, or signed incorrectly. Never assume title issues can be fixed later. Missing signatures, altered information, or blank sections can delay or prevent registration.

- The seller is using an open title. An open title occurs when the vehicle owner never properly transferred ownership into their name before reselling it. This practice, known as title jumping, is illegal in many states and can create significant registration problems for the buyer.

- The seller claims the title is being held by a bank but cannot provide documentation. If there is an active lien, request proof of the loan status and obtain a lien release before completing the purchase.

- The seller only wants cash and refuses secure payment methods. While cash is common in private sales, reluctance to use a bank, cashier’s check, or documented payment method may be a warning sign.

- The seller refuses a vehicle inspection or history check. Honest sellers are usually willing to allow an independent mechanic inspection and provide the VIN for a vehicle history report.

- The odometer reading appears inconsistent with the vehicle’s condition or records. Excessive wear, missing maintenance records, or mileage discrepancies may indicate odometer fraud.

To protect yourself, never pay for a vehicle until ownership has been verified. Avoid relying solely on photos or screenshots of documents, as they can be altered or outdated. Whenever possible, meet the seller in a safe public location and complete the transaction at a DMV office, bank, credit union, or title agency where documents can be reviewed and verified before funds change hands.

Conclusion

If you’re still wondering what do you need to buy a car, the answer ultimately depends on how you’re paying, where you’re buying, and whether you’re trading in another vehicle. However, most buyers will need a valid driver’s license, proof of insurance, an accepted payment method, and additional financial documents if financing is involved.

Understanding what you need to buy a car before you visit a dealership or meet a private seller can help you avoid delays, reduce stress, and prevent costly mistakes. Buyers who prepare their paperwork in advance are often able to complete the transaction more quickly and negotiate with greater confidence.

Whether you’re purchasing a new vehicle, financing a used car, or completing a private-party sale, knowing exactly what you need to buy a car puts you in a stronger position throughout the process. Create a folder with all required documents, verify the seller’s requirements beforehand, and keep copies of every document you sign. A little preparation today can make the entire car-buying experience faster, safer, and far more enjoyable.