Money decisions don’t usually happen in calm, quiet moments. They show up when you’re juggling rent or a mortgage, wondering if you’re saving “enough,” switching jobs, planning for kids, or lying awake at night thinking, “Am I missing something important?”

That’s where the right financial advisor can make a real difference by helping you make sense of what you already earn, save, and worry about.

Through this article, you’ll find the top U.S. financial advisory firms in 2025 through a practical, human lens. Instead of ranking firms by size alone, we focus on who each firm is actually good for, how they work, what they typically cost, and when they make sense for real people living real lives.

Why Choosing the Right Financial Advisor Matters More Than Ever

Financial advice in 2025 goes far beyond picking investments. Most people need guidance on balancing saving, spending, and debt, planning for major expenses like housing, childcare, or elder care, understanding taxes and retirement accounts, and avoiding costly mistakes during major life transitions.

The challenge is that many “best advisor” lists focus on assets under management or brand size. A firm managing trillions of dollars isn’t automatically a better fit than a smaller one. What matters most is alignment: advice that matches your goals, values, and financial reality.

How We Evaluated These Firms (Without the Marketing Spin)

Rather than relying on rankings or promotional lists, this article uses industry analytics and competitor gap analysis to focus on one essential question: which firms truly help people make better financial decisions at different stages of life? In evaluating firms, we looked at fee transparency (fee-only versus commission-based models), accessibility through reasonable minimums and advice options, the breadth of planning beyond investing alone, consistency and trust through fiduciary responsibility and reputation, and how well each firm serves common life situations.

Top U.S. Financial Advisory Firms to Know in 2025

1. Fidelity Investments

Fidelity works well for people whose finances aren’t static, like households that want flexibility. You might start with digital guidance, then later want a dedicated advisor as your income or responsibilities grow.

Why It Stands Out

It offers multiple levels of advice, ranging from robo-style investing to personalized one-on-one planning. It also excels in retirement planning, tax-aware strategies, and workplace plan integration, making it a strong fit for both beginners and more experienced investors.

Good To Know

Fees and service quality can vary significantly depending on the tier you select. In most cases, the best overall experience tends to begin once your assets move beyond entry-level thresholds.

2. Vanguard Personal Advisor Services

Best For

Vanguard appeals to people who don’t want complexity, or sales pressure. The philosophy is steady, long-term, and low-cost.

Advantages

It offers very competitive advisory fees and follows a long-term, evidence-based investing philosophy. It’s especially well-suited for retirement-focused households that value consistency and disciplined planning.

Disadvantages

Customization may be more limited compared to boutique advisory firms, and the approach works best for individuals who are comfortable with a structured, process-driven planning model rather than highly personalized strategies.

3. Charles Schwab Wealth Advisory

Advantages

Charles Schwab has a strong nationwide presence and offers a solid balance between automated tools and human oversight. It’s a good option for people looking to consolidate multiple accounts and simplify their financial picture.

Disadvantages

Full-service planning typically comes with higher minimums, and the quality of the experience can vary depending on the advisor and location.

Best For

Schwab blends digital tools with access to financial professionals, making it a good fit for people who want guidance without constant meetings.

4. Facet Wealth

Facet flips the traditional advisor model. Instead of charging a percentage of your assets, they use a flat annual fee, something many people find easier to understand, which makes it especially suitable for young professionals. However, Facet brings best value only if you actively use planning services, and its investment management is optional.

Features

It uses a flat-fee model with no assets-under-management pressure and pairs clients with a dedicated CFP professional. It’s especially well-suited for planning around career decisions, equity compensation, and long-term family goals.

5. Edward Jones

With thousands of local offices across the U.S., Edward Jones places a strong emphasis on personal relationships and face-to-face guidance. It offers a familiar, traditional advisory experience that appeals to clients who value ongoing, in-person support.

It remains popular for one reason: accessibility. If you value face-to-face meetings and long-term relationships, this model still resonates. Edward Jones’s fees may be higher than digital-first firms, and the investment approach often leans more conservative, prioritizing long-term stability over aggressive growth.

6. J.P. Morgan Wealth Management

Best For

If your checking, credit cards, and savings already live under one roof (Chase), J.P. Morgan can offer convenience and integrated planning.

Pros

It offers easy access through Chase branches, provides a wide range of financial services under one roof, and works well for people who value coordination across their banking and investment accounts.

Cons

The best experience typically requires higher account balances, and the advice can feel less flexible compared to working with an independent advisor.

7. Independent Fee-Only RIAs (Registered Investment Advisors)

Not every great advisor works at a national brand. Many independent RIAs specialize in deep planning and long-term relationships. So if you want personalized and conflict-free advice, it is a good choice for you.

Independent advisors are often 100% fiduciary and fee-only, offering a high level of customization and ongoing, personalized guidance. They can be a strong fit for families, business owners, and those with more complex finances, but quality varies significantly, making careful vetting essential, and they may not offer the same flashy technology platforms as larger firms.

8. Merrill (Bank of America)

Merrill is suitable for clients with growing assets who want structured planning. It combines traditional wealth management with digital tools through Bank of America. However, you should consider if you’re moving into more complex financial territory.

It combines integrated banking and investing with robust planning capabilities designed for higher-balance households. It’s supported by an established advisory infrastructure that delivers consistency and scale.

9. Vanguard Digital Advisor

This is a robot-advisor, offering guidance without the cost of a dedicated advisor, so it is best for hands-off investors getting started.

Vanguard Digital Advisor has low minimums that make it accessible. Automated portfolio management removes day-to-day complexity. And a simple goal-based structure keeps investing easy to understand and maintain.

10. Betterment Premium

Betterment blends robo-advising with access to CFP professionals, so it is one of the best options for digital-first users who still want human input. It offers a simple, intuitive platform paired with strong tax-efficient investing. At higher service tiers, you can connect with human advisors when questions get more complex.

How to Choose the Right Firm for Your Life

Instead of asking “Which firm is the biggest?” ask:

- Do I want ongoing guidance or occasional check-ins?

- Am I paying for advice, or just investment management?

- Do I prefer digital tools, human meetings, or both?

- Will this advisor still make sense if my income or goals change?

A good advisor should grow with you, not lock you into a model that only works at one stage of life.

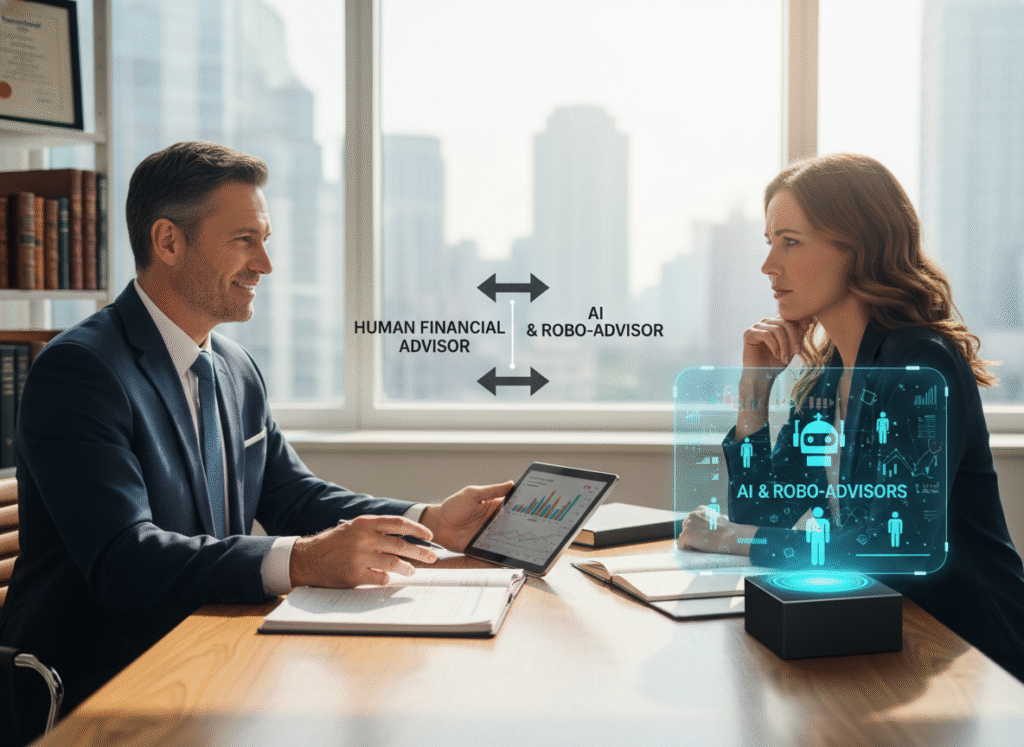

Human Financial Advisors vs. AI & Robo-Advisors: What’s the Real Difference in 2025?

If you’re researching financial advisory firms in 2025, you’ve probably noticed something else popping up everywhere: AI-driven financial advice. Robo-advisors, automated portfolios, and “AI financial planners” promise low fees, instant answers, and hands-off investing.

So between human financial advisors and AI-powered tools, which one is better? The honest answer: it depends on what kind of help you actually need.

What AI and Robo-Advisors Do Well

Robo-advisors work best when your finances are relatively straightforward, you’re looking for low-cost portfolio management, and you’re comfortable making decisions without ongoing conversations. They’re ideal if your primary need is help with the mechanics of investing rather than personalized financial planning.

Typical strengths include automated portfolio rebalancing, tax-loss harvesting, and goal-based investing models, along with lower fees, lower minimums, and 24/7 access without appointments. For early-stage investors or anyone who prefers a true “set it and forget it” approach, robo-advisors can be a solid starting point.

Where AI Falls Short

AI-based tools tend to struggle when life changes suddenly, such as during job loss, divorce, or illness, and when financial decisions involve complex trade-offs rather than clear formulas. They’re also less effective when you’re unsure about your goals or when emotions, family dynamics, or debt-related stress influence decision-making.

While an algorithm can rebalance a portfolio, it can’t talk you through a market panic, help couples navigate different money values, assess emotional readiness for risk, or adjust plans around real-life uncertainty.

What Human Financial Advisors Do Better

Human advisors bring something AI can’t replicate: judgment shaped by experience and real conversation. They’re especially valuable when you’re planning for retirement, children, or homeownership, managing multiple accounts or shared financial goals, or looking for help deciding a plan.

A human advisor can ask better follow-up questions, adapt strategies as your life changes, explain why certain decisions matter, and coordinate taxes, investments, insurance, and estate planning. Most importantly, they help translate complex trade-offs into clear, confident choices.

The Hybrid Reality: Where 2025 Is Headed

Some financial advisory firms blend AI technology with human expertise by using AI for analytics and automation while relying on advisors for planning, judgment, and personal guidance. This hybrid approach combines digital tools with direct advisor access, allowing firms to customize advice instead of applying one-size-fits-all templates, often resulting in lower costs, faster execution, more personalized strategies, and better emotional support during uncertain times.

Final Thoughts: The Best Advisor Is the One You’ll Actually Use

The “best” financial advisory firm isn’t the one with the flashiest name or the biggest assets under management. It’s the one that explains things clearly, charges fees you actually understand, helps you make decisions with confidence, and adapts as your life changes. When financial advice feels approachable and genuinely aligned with your goals, money becomes less stressful, and a lot more useful in everyday life.