Buying a home doesn’t usually happen when life is neat and perfectly timed.

Maybe rent keeps climbing faster than your paycheck. Maybe you’ve finally stabilized your income, but your savings aren’t where you hoped they’d be. Or maybe you’ve spent years fixing your credit and still feel locked out of “real” homeownership.

This is exactly the space where FHA loans live. For millions of Americans, FHA loans quietly make buying a home possible when other doors stay closed.

This guide walks through FHA loans the way real people experience them, with clarity, context, and honest trade-offs, so you can decide whether this path actually makes sense for your life.

What Is an FHA Loan (and Why It Exists)

An FHA loan is a mortgage insured by the Federal Housing Administration (FHA), an agency within the U.S. Department of Housing and Urban Development (HUD). The government doesn’t lend you the money directly, instead, a private lender issues the loan, and the FHA insures a portion of it. This insurance reduces the lender’s risk if a borrower defaults, which is why FHA loans often have more flexible credit and down payment requirements than conventional mortgages.

Originally created during the Great Depression to make homeownership more accessible, FHA loans still serve that mission today. They’re especially popular with first-time homebuyers, buyers with limited savings, people rebuilding credit, younger households early in their careers, and families who value stability and affordability over having a “perfect” financial profile.

How FHA Loans Work in Everyday Terms

At a practical level, FHA loans work much like any other mortgage. You borrow money from a bank or lender and repay it over time, typically across 15 or 30 years. Your monthly payment usually includes principal and interest, along with property taxes, homeowners insurance, and FHA-specific mortgage insurance.

What sets FHA loans apart is their flexibility. Borrowers can choose fixed-rate or adjustable-rate options, select 15- or 30-year terms, and take advantage of features like seller contributions of up to 6% of the purchase price and gifted down payments. FHA loans also allow higher debt levels and are more forgiving of past credit issues, making them accessible to buyers who might not qualify elsewhere.

FHA Loan Requirements (What Actually Determines Approval)

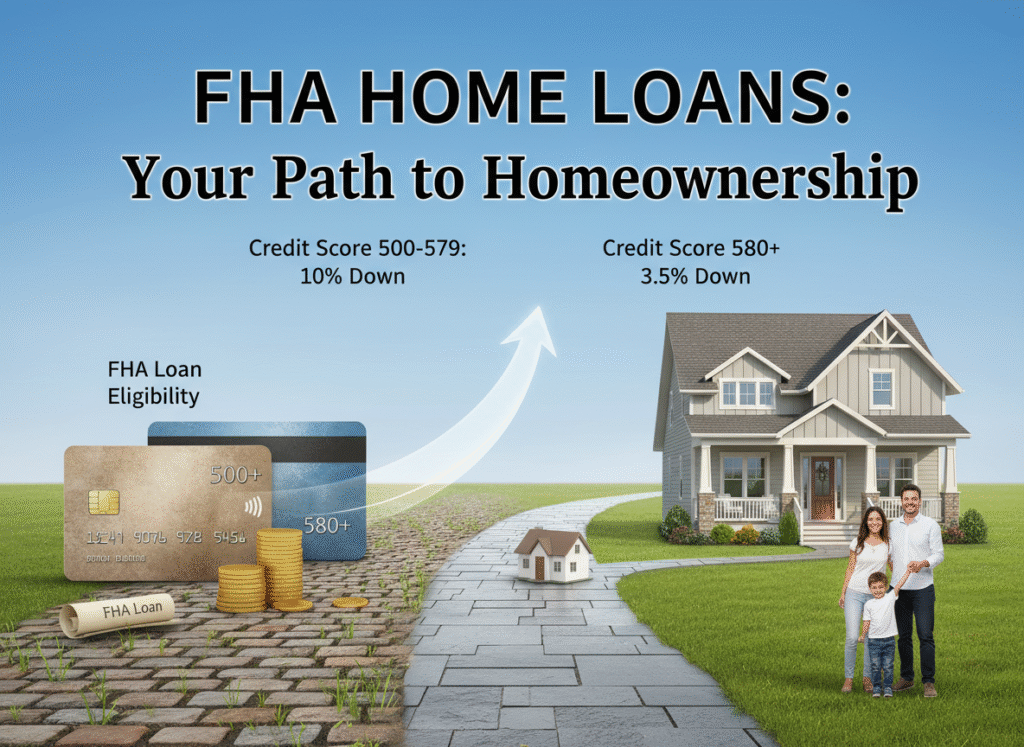

Credit Score Requirements

FHA loans are known for their credit flexibility, but approval isn’t one-size-fits-all. The FHA sets minimum credit score tiers: borrowers with scores of 580 or higher can qualify with as little as 3.5% down, while scores between 500 and 579 typically require a 10% down payment. Scores below 500 are generally not eligible for FHA financing.

There’s an important nuance many buyers miss. While the FHA establishes the baseline rules, individual lenders can impose higher standards. In practice, many lenders prefer scores in the 600–620+ range, especially in competitive or higher-risk markets. Even so, FHA loans remain one of the few mainstream mortgage options where less-than-perfect credit doesn’t automatically lead to rejection. Past bankruptcies, foreclosures, or collections don’t disqualify you by default. What matters most is how well you’ve recovered and how you’ve managed credit recently.

Down Payment Rules (and Where the Money Can Come From)

The minimum down payment is 3.5% with qualifying credit and 10% for lower credit scores. Unlike conventional loans, FHA allows down payment funds from several sources, including personal savings, family gifts, employer assistance, approved down payment assistance programs, and certain government or nonprofit grants. Remember, all gifted funds must be documented because lenders will want a paper trail confirming the money is truly a gift, not a loan in digest.

Debt-to-Income Ratio (DTI): Why FHA Is More Forgiving

Your debt-to-income (DTI) ratio compares your monthly debt payments to your gross monthly income. For FHA loans, general benchmarks are around 31% for housing costs and about 43% for total debt, but these aren’t hard caps. FHA guidelines often allow higher ratios when borrowers have stable income, cash reserves, a solid employment history, or other compensating factors. Because of this flexibility, FHA loans can be a good fit for buyers managing student loans, car payments, or ongoing childcare expenses.

Income Limits (A Common Misunderstanding)

Here’s the thing: there are no FHA income limits. You don’t have to be “low income” to qualify. You simply need to earn enough to cover your monthly mortgage, manage your other debts, and demonstrate consistency. High earners with limited savings often qualify just as easily as moderate earners.

FHA Mortgage Insurance (MIP): The Cost of Flexibility

Every FHA loan includes mortgage insurance premiums (MIP), which is the biggest trade-off borrowers need to understand upfront. FHA mortgage insurance protects the lender, not the borrower, and it comes in two parts: an upfront premium and an ongoing annual premium.

The upfront MIP equals 1.75% of the loan amount and is usually rolled into the loan balance rather than paid out of pocket. In addition, borrowers pay annual MIP in monthly installments, typically ranging from about 0.15% to 0.75% of the loan amount, depending on the size of the down payment, loan term, and total loan amount.

How long you pay MIP depends on how much you put down. If your down payment is less than 10%, mortgage insurance lasts for the life of the loan. With 10% or more down, MIP ends after 11 years. Because of this structure, many buyers use FHA loans as a stepping stone, then refinancing into a conventional loan later to eliminate mortgage insurance once their equity and credit improve.

FHA Loan Limits

FHA loans come with borrowing limits that vary by county. For 2025, limits generally range from $524,225 in lower-cost areas and up to $1,209,750 in high-cost markets.

Table 1: 2025 FHA Loans Limits

| Property type | Low-cost area limit | High-cost area limit | Special exception areas limits |

|---|---|---|---|

| One-unit | $524,225 | $1,209,750 | $1,814,625 |

| Two-unit | $671,200 | $1,548,975 | $2,323,450 |

| Three-unit | $811,275 | $1,872,225 | $2,808,325 |

| Four-unit | $1,008,300 | $2,326,875 | $3,490,300 |

| Source: U.S. Department of Housing and Urban Development | |||

Property Requirements and FHA Appraisals

FHA loans include stricter appraisal standards than many other mortgage types. As part of the process, an FHA-approved appraiser evaluates the home’s market value and also checks for basic safety, livability, and structural soundness. This includes making sure essential systems like the roof, heating, plumbing, and electrical components are functioning properly. If the appraiser identifies problems that don’t meet FHA standards, those issues typically need to be repaired before closing, which can affect both negotiations with the seller and the overall closing timeline.

Types of FHA Loans

- FHA 203(b)-standard purchase loan: The most common FHA loan, used for buying or refinancing a primary residence.

- FHA 203(k)-renovation loan: Combines purchase and renovation costs into one mortgage. It’s helpful in competitive markets where fixer-uppers are more available.

- FHA 203(h)-disaster recovery loan: For buyers rebuilding after federally declared disasters. It often allows no down payment.

- FHA energy-efficient mortgage (EEM): Adds funds for energy upgrades like insulation or solar improvements.

- FHA HECM (reverse mortgage): For homeowners 62+ converting home equity into income. It’s useful in specific retirement scenarios, but not universally appropriate.

FHA vs. Conventional Loans: A Realistic Comparison

| FHA loans | Conventional loans |

|---|---|

|

|

Who FHA Loans Are Best For

An FHA loan can be a smart option if you’re buying your first home, have decent but imperfect credit, or haven’t saved a large down payment. They’re also appealing if you want predictable approval criteria and plan to refinance later once your credit, income, or home equity improves.

However, FHA loans may not be ideal if you already have excellent credit and substantial savings, since conventional loans can offer lower long-term costs. They’re also not designed for second homes or investment properties, and they’re a poor fit if avoiding mortgage insurance altogether is a top priority.

How First-Time Buyers Qualify (Step-by-Step)

- Review your credit and debt

- Estimate a realistic monthly payment

- Gather income and asset documents

- Compare FHA-approved lenders

- Get preapproved before shopping

- Choose an FHA-eligible property

- Budget for insurance and closing costs

- Close and plan for the long term

Final Thoughts: FHA Loans Aren’t Easy, They’re Accessible

FHA loans don’t remove responsibility. They don’t guarantee approval. And they aren’t the cheapest option in every scenario. However, they offer a real path forward. For renters, they’re ready to stop waiting. For families, they can build stability gradually. For buyers who need a practical entry point, not perfection. When used carefully, an FHA loan can be a helpful starting line.

Related Articles

Private Mortgage Insurance (PMI) Explained: What It Costs, How It Works, and How to Avoid It