Freelancing offers the freedom to work on your own terms, but it also comes with the responsibility of managing your own taxes. Unlike traditional employees, freelancers face a unique set of tax requirements, from income reporting to self-employment tax. Understanding how to properly calculate your taxes and take advantage of tax-saving opportunities is essential to avoid surprises at tax time and minimize your tax liability.

In this guide, we’ll walk you through the key tax rules for freelancers, explain the most common tax deductions available, and provide simple steps to help you lower your tax bill. By the end of this article, you’ll have the knowledge and tools you need to manage your freelance taxes with confidence.

What You Need to Know About Freelance Taxes

As a freelancer, you’re considered self-employed, which means you’re responsible for paying both income tax and self-employment (SE) tax. SE tax includes contributions to Social Security and Medicare and is set at a rate of 15.3%. This is typically split between an employer and employee for traditional workers, but as a freelancer, you’re responsible for paying the full amount.

The IRS requires freelancers to file Schedule C with their tax return to report their business income and expenses. Freelancers also need to track their income using 1099-NEC forms, which clients send if they’ve paid $600 or more during the tax year.

Understanding these requirements and ensuring you stay compliant will make filing taxes easier and help you avoid penalties.

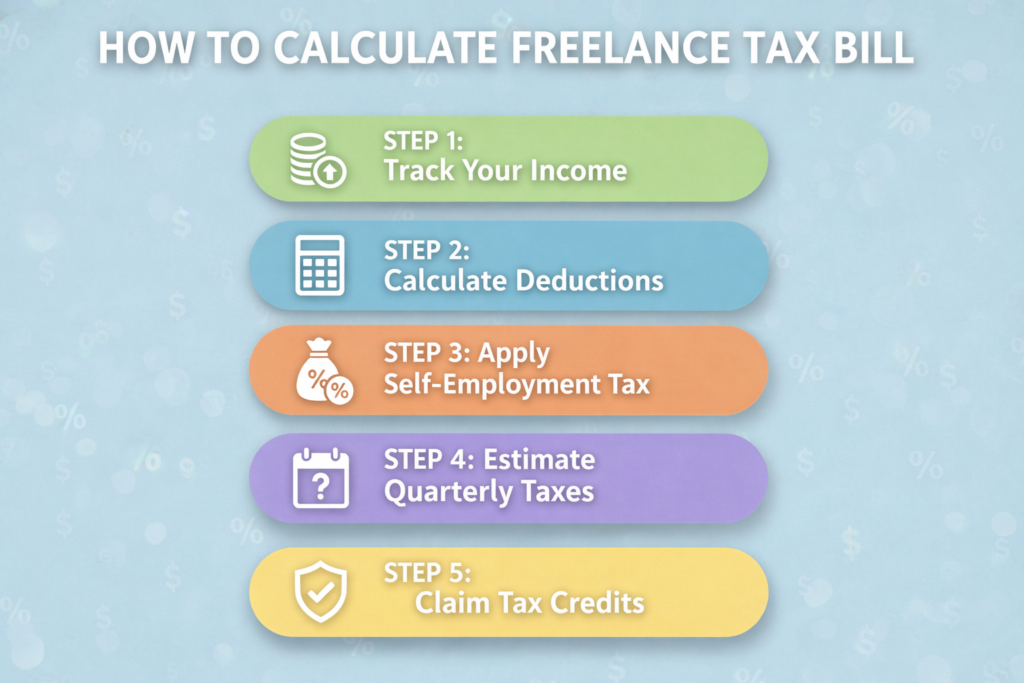

Step-by-Step: How to Calculate Your Freelance Tax Bill

Step 1: Track Your Income

Freelancers typically receive income through 1099-NEC forms from clients, as well as other payments (such as Venmo or PayPal). All income needs to be reported, even if a client doesn’t send you a 1099 form. Keeping track of all income is crucial to ensure accurate tax reporting.

For example, if you earned $40,000 in freelance income and received $10,000 through a third-party payment processor like PayPal (without receiving a 1099 form), you must report all $50,000 on your tax return.

Step 2: Calculate Deductions

As a freelancer, you can deduct business expenses from your taxable income. These expenses can reduce the amount of income that is subject to tax, thus lowering your tax bill. Common freelance deductions include:

- Home office deduction: If you work from home, you can deduct a portion of your rent, mortgage, utilities, and other related costs. The space must be used regularly and exclusively for business purposes.

- Business equipment and supplies: Any equipment or supplies you use for your freelance work (such as a computer, printer, office supplies, or software) can be deducted.

- Travel and meals: Business travel expenses, including transportation, lodging, and meals, are deductible. Note that only 50% of meal expenses are deductible.

- Education: Courses, certifications, or books related to your profession can be deducted if they improve your skills or qualifications.

Step 3: Apply Self-Employment Tax

As a freelancer, you’re required to pay the full self-employment tax. This tax is calculated at 15.3% on your net earnings from self-employment. However, you can deduct the employer portion of the self-employment tax when calculating your adjusted gross income (AGI). This effectively reduces your taxable income and, in turn, your overall tax bill.

For example, if your net earnings from freelancing are $50,000, you’ll pay $7,650 in self-employment tax (15.3% of $50,000). However, you can deduct half of this amount ($3,825) from your taxable income when calculating your AGI.

Step 4: Estimate Quarterly Taxes

Freelancers don’t have an employer to withhold taxes from their paychecks, so it’s essential to set aside money throughout the year to cover your tax liability. The IRS requires freelancers to pay estimated quarterly taxes if you expect to owe $1,000 or more in tax for the year.

Estimated tax payments are due in April, June, September, and January. You can use Form 1040-ES to calculate and pay your estimated taxes. This proactive step helps you avoid penalties for underpayment and spreads your tax liability throughout the year.

Step 5: Claim Tax Credits

In addition to deductions, freelancers may qualify for tax credits that directly reduce the amount of tax they owe. Some of the most common credits for freelancers include:

- The Earned Income Tax Credit (EITC): If you meet certain income and filing status requirements, you may be eligible for this credit, which can reduce your tax liability or increase your refund.

- Child Tax Credit: If you have qualifying children, you can claim up to $2,000 per child, depending on your income.

Tax credits are often more valuable than deductions because they directly reduce your tax bill dollar-for-dollar.

Common Deductions for Freelancers

Freelancers can claim a variety of deductions that help reduce their taxable income.

The home office deduction is one of the most beneficial for freelancers who work from home. You can deduct part of your rent or mortgage, utilities, and other home-related expenses. To qualify, the space must be used exclusively and regularly for business purposes. If you run your business from a spare room in your house, you can claim that portion of your rent or mortgage.

Another important deduction is business expenses. This includes any equipment you use in your freelance work, such as computers, printers, and office supplies. If you purchase software or subscriptions for your business (like accounting software or design tools), those are deductible as well.

You can also deduct travel and meals related to business trips. When you travel for work, expenses like flights, hotel accommodations, transportation, and meals can be deducted. However, keep in mind that only 50% of meal expenses are deductible.

Health insurance premiums are another area where freelancers can save money. If you’re self-employed, you can deduct the cost of your health insurance premiums, reducing your taxable income. This is particularly beneficial for freelancers who buy their own health insurance.

Using Tax Software vs. Hiring a Professional

While many freelancers choose to file their taxes using tax software like TurboTax or H&R Block, others may prefer to work with a tax professional to navigate the complexities of their freelance tax situation.

Tax Software

It can simplify the filing process by guiding you through each step, helping you claim deductions, and calculating your self-employment tax. Many software options are designed specifically for freelancers and small business owners, making them a great choice for those with straightforward tax situations.

Tax Professional

If your freelance income is substantial or you have more complex tax situations, working with a tax professional may be the best option. They can help you identify additional deductions, optimize your tax strategy, and ensure compliance with all tax laws.

Final Thoughts: Take Control of Your Freelance Taxes

Managing your taxes as a freelancer may seem complex, but with the right knowledge and tools, you can navigate the process with confidence. By keeping track of your income, deductions, and quarterly payments, and by taking advantage of tax credits and retirement contributions, you can lower your tax liability and avoid common pitfalls.

With the right planning and organization, you can not only stay compliant with the IRS but also maximize your refund and improve your financial future. Whether you choose to use tax software or hire a professional, taking the time to understand your freelance tax responsibilities will set you up for success every tax season.