Missing the tax deadline can feel frightening, especially if you know you owe money. Many people freeze because they think filing without payment will make things worse. In reality, doing nothing is usually the most expensive choice.

So, what happens if you don’t file taxes? The IRS can charge IRS penalties, add interest, prepare a substitute for a return, hold refunds, and eventually begin collection actions. The longer you wait, the more the problem grows. The good news is that unfiled tax returns can usually be fixed. The key is understanding the difference between failure-to-file, failure-to-pay, and accruing interest on taxes.

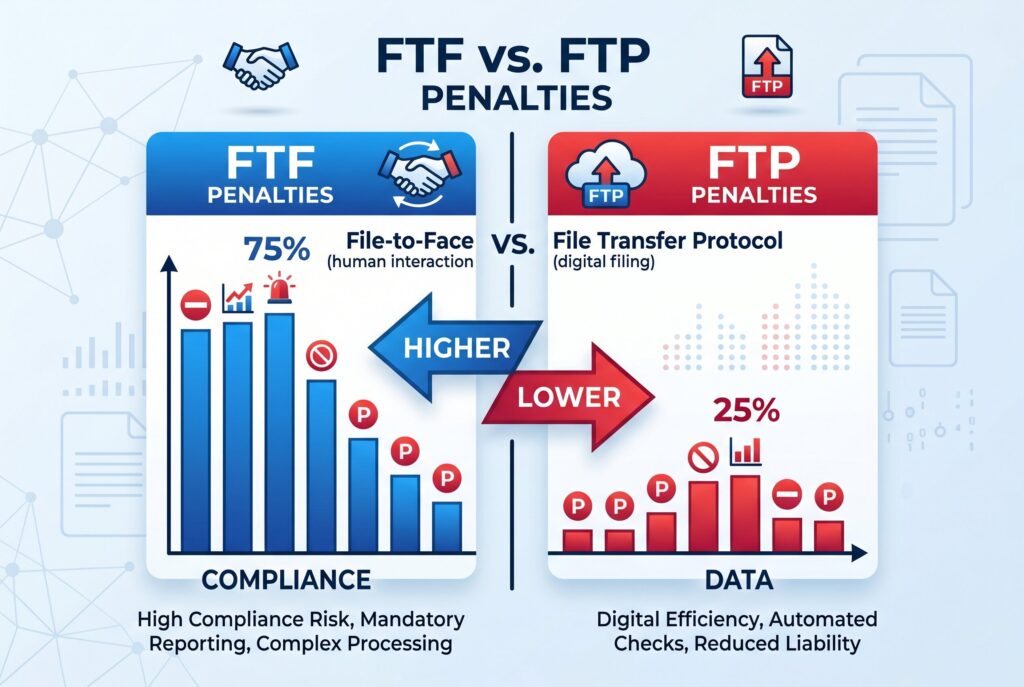

The Two Heavy Hitters: FTF vs. FTP Penalties

The IRS treats not filing and not paying as two separate problems. This distinction matters because the failure-to-file penalty is usually much harsher than the failure-to-pay penalty.

Rule 1: Not Filing Costs More than Not Paying

If you don’t file and don’t pay, the IRS generally charges both penalties. However, the failure-to-file penalty is reduced by the failure-to-pay penalty for the same month. That usually creates a combined monthly penalty of 5% for the first five months, made up of 4.5% for failure-to-file and 0.5% for failure-to-pay. The IRS says the total combined penalty can reach 47.5% of the unpaid tax.

Failure-to-file Penalty

The failure-to-file penalty applies when your return is late and tax is unpaid. It’s generally 5% of unpaid tax for each month or part of a month the return is late, up to 25%. For returns required to be filed in 2026, if the return is more than 60 days late, the minimum penalty is the smaller of $525 or 100% of the tax due.

Failure-to-pay Penalty

The failure-to-pay penalty applies when you file but don’t pay the full balance by the deadline. It’s generally 0.5% of unpaid tax per month or part of a month, up to 25%. This is why filing as soon as possible is often the smartest first move, even if you can’t pay everything immediately.

Accruing IRS Interest: The Cost of Money Over Time

Penalties aren’t the only cost. The IRS also charges interest on unpaid taxes. For individual overpayments and underpayments, the IRS announced a 7% annual rate for the first quarter of 2026, compounded daily. This daily compounding matters. A tax bill that feels manageable in April can become much more painful after months of penalties and interest. The IRS interest rate can also change quarterly, so taxpayers should treat any example as an estimate, not a permanent rate.

Penalties by the Numbers: Real World Scenarios

Scenario A: The “I forgot” Return

Imagine you owed $2,000, missed the deadline, but filed and paid one month later. Your late filing penalty and late payment penalty may apply, plus interest. The dollar amount may still hurt, but acting quickly keeps the damage contained.

Scenario B: The “I can’t pay, so I won’t file” Return

Now imagine you owed $2,000 and ignored the return for five months. The failure-to-file penalty can climb quickly, and the failure-to-pay penalty continues while the balance remains unpaid. Interest keeps running too. This is the worst strategy because it combines the most expensive IRS penalties with time. If you can’t pay, file anyway. Filing stops the heavier late filing penalty from growing.

IRS Criminal Prosecution: When Is It a Reality?

Most late tax situations are civil, not criminal. A person who forgets, misunderstands the rules, or can’t afford to pay usually isn’t treated the same as someone who intentionally hides income. That said, IRS criminal prosecution can become a reality when there is willful failure to file taxes, tax evasion, false documents, hidden income, or a repeated pattern of intentional noncompliance. “Willful” generally means intentional conduct, not an honest mistake. If you have years of unfiled tax returns, large unpaid balances, business payroll tax issues, or IRS notices you’ve ignored, it’s wise to speak with a qualified tax professional.

Other Major Consequences Beyond the Cash

Infinite Statute of Limitations

The normal statute of limitations for IRS assessment generally depends on a filed return. If no return is filed, the clock may not start. That means the statute of limitations for non-filing can remain open much longer than taxpayers expect.

Loss of Tax Refund and Credits

If you were due a refund, you may not face a late filing penalty, but waiting can still cost you. Refund claims generally expire after a limited period, often three years from the original due date. Missing that window can mean permanent loss of tax refund. Unfiled returns can also prevent you from claiming credits such as the Earned Income Tax Credit or Child Tax Credit for eligible years.

Difficulty Qualifying for Loans

Mortgage lenders, auto lenders, and business lenders often ask for recent tax returns. If you can’t provide them, loan approval may become harder, even if your income is strong.

The SFR: A substitute for a return

If you don’t file, the IRS may create a substitute for a return, often called an SFR. This is rarely favorable. The IRS may use income records it has, but the return may not include deductions, credits, filing choices, or business expenses you could have claimed. That can create a much higher unpaid taxes penalty and tax balance than necessary.

How to Fix It: A Step by Step Recovery Plan

Rule 1: File Immediately

The most important step in how to fix unfiled tax returns is to file as soon as possible. Don’t wait until you can pay. Filing helps stop the failure-to-file penalty from growing and gives you a real number to work with. Gather W-2s, 1099s, bank records, business income records, and expense documentation. If documents are missing, request wage and income transcripts from the IRS.

Rule 2: Communicate With the IRS

Once returns are filed, you may have options. An installment agreement can let you pay over time. An Offer in Compromise may settle tax debt for less than the full amount in limited cases. Currently Not Collectible status may pause collection if you can’t afford basic living expenses. Penalty relief may also be possible if you qualify for first-time penalty abatement or reasonable cause relief.

Conclusion

Ignoring the IRS doesn’t make a tax problem disappear. It usually makes it more expensive. The late filing penalty, failure-to-pay penalty, IRS interest rate, substitute for a return risk, and possible loss of refund can turn a simple missed deadline into a serious financial problem. The best first step is simple: file the return, even if you can’t pay today. Then review payment options, ask for penalty relief when appropriate, and build a plan before the IRS builds one for you.