What is accrued interest? Accrued interest is the hidden number that can make your credit card balance grow, your loan payoff amount change, or your savings account earn money before the next statement arrives. In simple terms, accrued interest is interest that has been earned or incurred but hasn’t yet been paid or received. Understanding it matters because interest usually builds daily, not just monthly.

Interactive Tool: The Accrued Interest Calculator

To estimate accrued interest, you need four numbers:

- Principal: the amount borrowed, saved, or invested

- Annual interest rate: the APR or stated yearly rate

- Time period: the number of days interest has been building

- Day count: usually 365 days, though some products may use 360

Example inputs:

- Principal: $3,000

- Annual interest rate: 20%

- Time period: 10 days

- Day count: 365

Result: $16.44 in accrued interest

This kind of calculator is useful for checking credit card balances, loan payoff quotes, savings deposits, and short-term interest estimates.

Accrued Interest Calculator

The Formula: How to Calculate Accrued Interest

The standard accrued interest calculation is:

Here’s a credit card example:

You carry a $3,000 balance at 20% APR for 10 days.

That means roughly $16.44 of interest accrues over those 10 days.

This formula works best for simple daily interest estimates. Real products may have extra details, such as compounding frequency, fees, promotional rates, grace periods, or different day-count conventions. Still, the core idea remains the same: the larger the balance, the higher the rate, or the longer the time period, the more interest accrues.

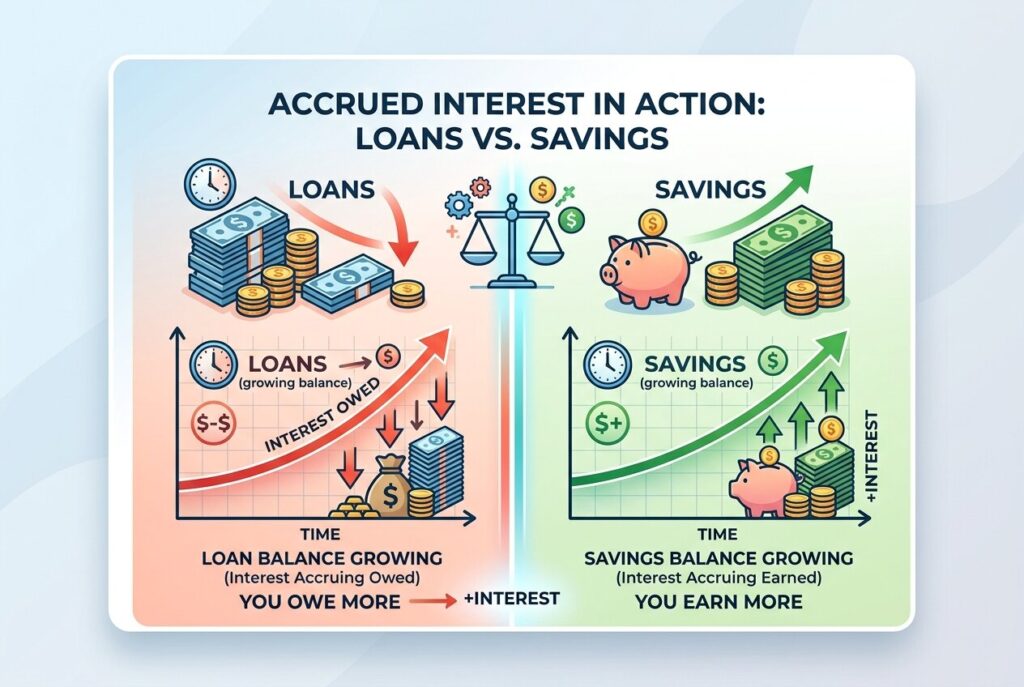

Accrued Interest in Action: Loans vs. Savings

Accrued Interest on Loans

Accrued interest on loans is interest that builds between payment dates. Auto loans, mortgages, personal loans, and student loans often accrue interest daily. That means your exact payoff amount may change depending on the date you pay.

For example, if your loan accrues $5 per day in interest, paying five days earlier may save about $25. That may sound small, but over months or years, earlier or extra payments can reduce total interest cost. This is why making biweekly payments or paying more than the minimum can help. You reduce the principal sooner, which gives future interest less balance to build on.

Accrued Interest on Savings

Savings interest works from the opposite side. Instead of owing interest, you earn it. A bank may calculate interest daily based on your account balance but only deposit it monthly. During the month, that interest has accrued even though you haven't received it yet. For savers, higher balances, higher rates, and longer holding periods usually mean more accrued interest. If interest is later added to your balance, it can begin earning more interest too.

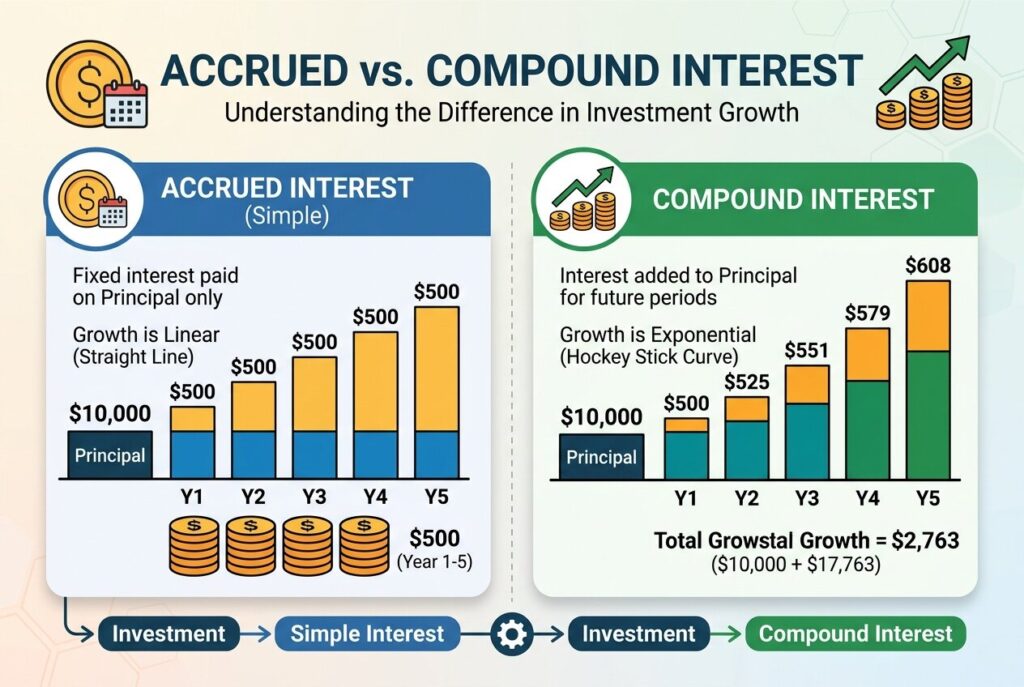

Accrued vs. Compound Interest: What’s the Difference?

Accrued vs compound interest is a common point of confusion. Accrued interest is the interest that builds during a period before it’s paid or added to the account. Compound interest happens when accrued interest is added to the principal, and future interest is calculated on the new, larger balance. For a saver, compounding can help wealth grow faster because you earn interest on interest. For a borrower, compounding can make debt grow faster because you may pay interest on unpaid interest.

Example: If you earn $10 in interest and it sits unpaid, that is accrued interest. If the $10 is added to your $1,000 balance and you now earn interest on $1,010, that is compound interest.

The Accounting Perspective

In accrual accounting, businesses record interest when it’s earned or incurred, even if cash hasn't moved yet. This creates more accurate financial statements because income and expenses are matched to the period they belong to.

For a borrower, accrued interest creates an expense and a liability.

Journal entry:

Debit Interest Expense

Credit Interest Payable

For a lender, accrued interest creates income and an asset.

Journal entry:

Debit Interest Receivable

Credit Interest Income

For example, if a company lends money and earns $500 of interest by the end of the month but hasn't received payment yet, it still records the $500 as interest income. The unpaid amount appears as interest receivable until cash is collected. This accounting treatment helps show the real financial position of the business, not just the cash balance.

3 Strategies to Minimize Accrued Interest Costs

1. Make More Frequent Payments

More frequent payments reduce the time interest has to accrue. Biweekly loan payments can lower the principal faster than one monthly payment, especially if the extra timing leads to one additional payment over the year. Even small extra principal payments can reduce future interest because the next day’s interest is calculated on a lower balance.

2. Use the Grace Period Strategy

Credit cards often have a grace period for purchases if you pay the statement balance in full by the due date. When you do that, purchase interest may not accrue at all. The key is paying the statement balance, not just the minimum payment. Paying only the minimum leaves a balance, and that balance can continue accruing interest. Cash advances and balance transfers may follow different rules, so read the terms before assuming a grace period applies.

3. Avoid Deferred Interest Traps

Some store cards and promotional financing offers advertise “0% interest” for a set period. But certain deferred interest plans still track interest in the background. If the balance isn't fully paid by the deadline, all that previously hidden interest may be added at once. That can turn a good deal into an expensive mistake. Before using promotional financing, confirm whether it’s true 0% APR or deferred interest.

Conclusion

Accrued interest isn't just a monthly statement detail. It’s a daily event that affects loans, credit cards, savings accounts, investments, and business accounting. Borrowers should monitor how quickly interest builds, while savers and lenders should understand when earned interest becomes payable.

The main takeaway is simple: time matters. A few extra days can increase what you owe or what you earn. Use the accrued interest formula to audit your own loan, credit card, or savings statement before small daily amounts become large financial surprises.

Related Articles

- How Interest Rates Work: What You Need to Know for Everyday Banking

- Car Loan Interest Rates Explained: How They Work and Key Factors That Affect Your APR

- 10 Smart Strategies to Make the Most of Your Savings Account Interest

- Personal Loan Refinancing: How to Lower Your Interest Rate and Reduce Monthly Payments

- How to Pay Off High-Interest Debt Faster and Save Money on Interest Charges

- What Is Simple Interest? Formula & Free Calculator