What is simple interest? Simple interest is interest calculated only on the original principal amount, not on interest that has already built up. The math is simple, but understanding it matters in real life. A simple interest loan can affect how much you pay for a personal loan, auto loan, student loan, or bond investment. This guide explains the simple interest formula clearly, with examples you can actually use.

Interactive Tool: The Simple Interest Calculator

A simple interest calculator helps you test different loan or savings scenarios instantly. You enter the principal, annual rate, and time period, then the calculator shows total interest and total repayment. This is useful because small changes in rate or time can make a big difference. A $10,000 loan at 6% for 5 years costs $3,000 in interest. The same loan for 3 years costs only $1,800. The principal and rate are the same, but time changes the final cost.

2026 Simple Interest Calculator

Use this simple interest calculator to test loan or savings scenarios instantly. Enter the principal, annual interest rate, and time period to calculate total interest and total repayment.

Simple Interest = Principal × Annual Rate × Time

Total Repayment = Principal + Simple Interest

Average Interest Per Year = Total Interest ÷ Time

Note: This calculator uses simple interest only. It does not include compounding, fees, amortization, changing balances, or payment timing.

The Simple Interest Formula: Step-By-Step Examples

The simple interest formula is:

I = P × r × t

Example 1: The Personal Loan

Suppose you take out a $10,000 simple interest loan at a 6% annual rate for 5 years.

I = 10,000 × 0.06 × 5

Total interest = $3,000

Total repayment = $13,000

That means you repay the original $10,000 principal plus $3,000 in interest.

Example 2: The Time Trap

The most common mistake is using months as if they were years. If a loan lasts 6 months, t is not 6. It’s 0.5 because 6 months equals half a year.

For a $10,000 loan at 6% for 6 months:

I = 10,000 × 0.06 × 0.5

Total interest = $300

Using t = 6 would give the wrong result and make the interest look far too high.

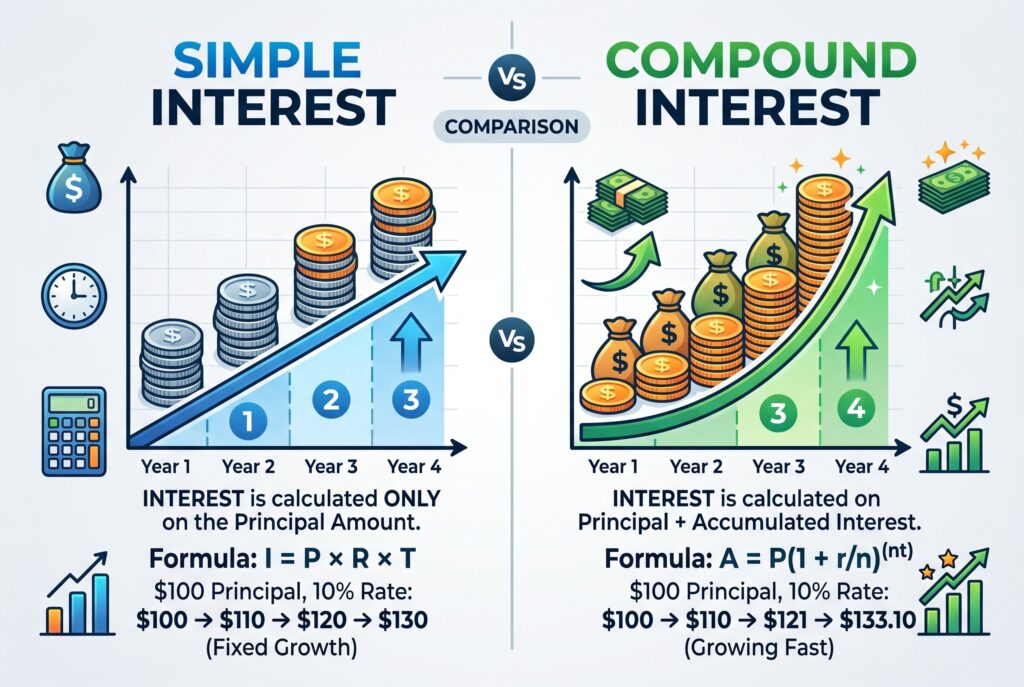

Simple Interest Vs. Compound Interest

Simple interest is steady. You pay or earn interest only on the original principal. The base amount doesn’t grow unless new money is added or principal is repaid. Compound interest is different. It adds interest to the balance, then future interest is calculated on the new larger amount. This creates “interest on interest.”

For borrowers, simple interest is usually easier to understand and may cost less than compound interest if payments are made on time. For savers and investors, compound interest can be more powerful because your earnings can grow faster over time. A simple way to remember it: simple interest grows in a straight line, while compound interest can grow faster as time passes.

What Is Accrued Interest?

What is accrued interest? Accrued interest is interest that has built up over time but hasn’t been paid yet. It can apply to loans, bonds, student loans, and other financial products. For example, a bond may pay interest every six months. During those six months, the interest gradually accrues. The investor doesn’t receive it every day, but the amount is still building until the coupon payment date.

Accrued interest also matters for borrowers. If interest builds daily on a loan, the amount owed may increase between payment dates. That is why payment timing can affect total interest, especially on daily simple interest loans.

Where Is Simple Interest Actually Used?

Simple interest appears most often in loans and debt products where interest is calculated on principal. Many auto loans and personal loans use daily simple interest. This means interest accrues each day based on the outstanding principal balance. Paying early can help because it reduces the principal sooner. Once the principal drops, future interest charges also drop. Paying late can do the opposite because more interest has time to accrue before the principal is reduced.

Bonds can also use simple interest through coupon payments. A corporate or municipal bond may pay a fixed interest amount based on face value and coupon rate. It’s important to be careful with mortgages and credit cards. Mortgages usually involve amortization schedules, and credit cards often use daily compounding or average daily balance methods. They shouldn’t be treated as basic simple interest products unless the agreement clearly says so.

Simple Interest Loan: What Borrowers Should Check

Before signing a simple interest loan, review the agreement carefully. Check the principal, interest rate, term, payment schedule, fees, and whether interest is calculated daily or annually. Also compare the interest rate with APR. A simple interest rate shows the interest calculation, but APR may include fees and other borrowing costs. If one loan has a lower interest rate but high fees, it may not be cheaper overall. Borrowers should also ask whether extra payments go directly toward principal. If they do, early payments can reduce the total interest paid.

Conclusion

Simple interest is one of the easiest finance formulas to learn, but it has real-world power. The formula for simple interest helps you estimate borrowing costs, bond payments, and basic investment returns. Before taking any loan, check whether it uses simple interest, compound interest, or an amortized structure. That detail changes your repayment strategy. If it’s a simple interest loan, paying early and reducing principal faster can directly lower the total interest you pay.