What is a simple interest loan? It is a loan where interest is calculated on the remaining principal balance, not on interest that has already built up. These days, understanding simple interest can help borrowers save real money on auto loans and personal loans. If you know how interest accrues daily, you can use early payments, extra payments, and smarter timing to reduce the total cost of borrowing.

The Daily Math: How Interest Is Calculated

The basic simple interest formula is:

Interest = Principal × Rate × Time

But lenders often calculate simple interest daily. They divide the annual percentage rate by 365 to get a daily interest rate. Then they multiply that daily rate by your current principal balance.

For example, imagine a $20,000 auto loan with a 6% annual rate.

Daily rate = 0.06 / 365 = 0.00016438

Daily interest = $20,000 × 0.00016438 = about $3.29 per day

If 30 days pass before your next payment, about $98.70 of interest has accrued. The rest of your monthly payment reduces principal. Once principal falls, the next month’s daily interest becomes lower.

The Early Payoff Simulator

An early payoff simulator helps you see how extra payments change the loan. For example, adding just $50 per month to a simple interest loan can reduce principal faster. That means less daily interest accrues in future months. This matters most early in the loan, when the principal balance is highest. Extra payments made early usually save more interest than extra payments made near the end. Before doing this, confirm that your lender applies extra money to principal and doesn’t charge a prepayment penalty.

The Trap: Late Payments Cost You More

Simple interest can help disciplined borrowers, but late payments can work against you. Because interest accrues daily, paying 5 days late gives the loan 5 extra days to build interest.

That means a larger part of your next payment goes toward interest instead of principal. If less principal is paid down, the next month starts with a higher balance than expected. Then future interest is calculated on that higher balance. This is why autopay can be useful. Paying on time keeps the loan schedule working as planned. Paying early can improve it. Paying late can slowly increase the total cost.

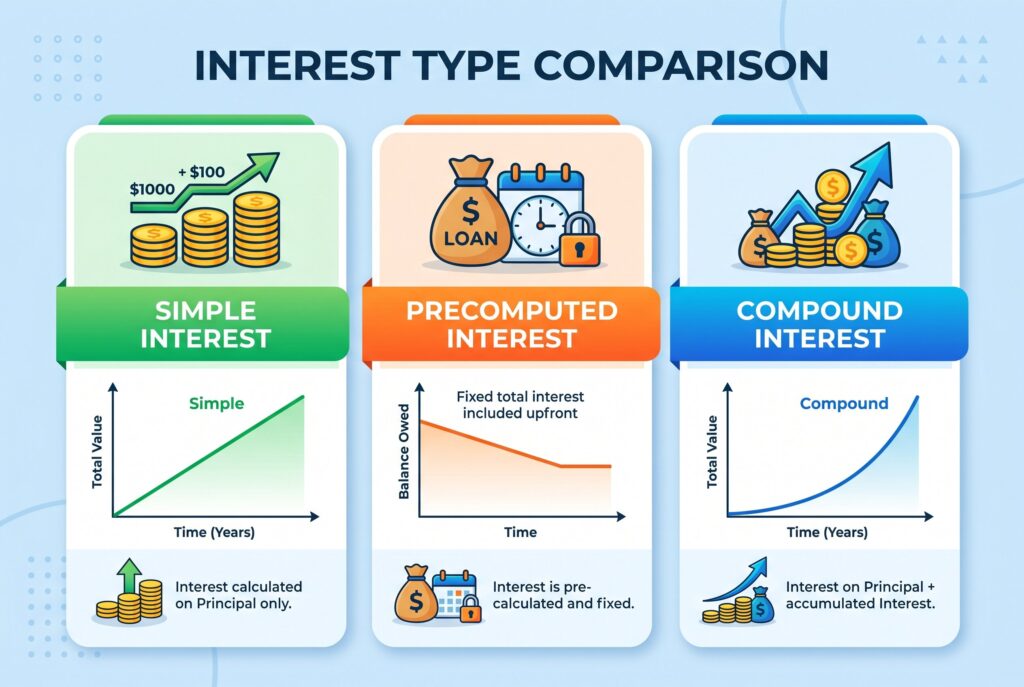

Simple Interest Vs. Precomputed Interest Vs. Compound Interest

| Loan Type | How Interest Works | Best For |

| Simple Interest | Interest is based on current principal | Borrowers who may pay early |

| Precomputed Interest | Interest is calculated upfront and spread across payments | Less flexible borrowers |

| Compound Interest | Interest can earn or charge more interest | Savers, not borrowers |

Simple interest is usually borrower-friendly when you make early or extra payments. Since interest is tied to the current principal balance, reducing principal faster can reduce total interest.

Precomputed interest is different. The lender calculates the total interest at the start of the loan and builds it into the payment schedule. Paying early may not save as much interest. Compound interest is powerful for savings because you earn interest on interest. But for debt, it can be expensive because the balance can grow faster if unpaid interest is added back into what you owe.

Simple Interest Auto Loan: Why It Matters

A simple interest auto loan is one of the most common places borrowers see this structure. Your car payment usually covers interest first, then principal. Since interest accrues daily, the timing of your payment affects how much goes to each part.

If you pay before the due date, fewer days of interest have accrued. More of your payment may reduce principal. If you pay after the due date, more interest has accrued, so less of the payment reduces the loan balance. This is why borrowers trying to pay off loans early should focus on principal reduction. Even small extra payments can help if they are applied correctly.

Simple Interest Loan Pros And Cons

A simple interest loan is easier to understand than many other loan structures. The math is transparent, and borrowers can often save money by paying early.

The main advantage is control. If your loan has no prepayment penalty, extra principal payments can reduce total interest. This makes simple interest helpful for borrowers with steady income or occasional extra cash. The downside is that late payments can hurt. Interest keeps accruing every day, so missing due dates can increase the cost. Also, simple interest doesn’t mean the loan is automatically cheap. APR, fees, term length, and lender rules still matter.

Questions To Ask Before You Sign

Before accepting any loan, ask the lender direct questions. Is this a simple interest loan? Is interest calculated daily? Are extra payments applied to principal? Is there a prepayment penalty? Are there origination fees or other charges?

These questions matter because two loans with the same interest rate can behave differently. A borrower-friendly loan should make it easy to pay down principal early without penalties. Also compare APR, not just the stated interest rate. APR can include fees and gives a clearer view of borrowing cost.

Conclusion

Simple interest can be a smart structure for auto loans and personal loans because it rewards faster principal repayment. The key is payment timing. Pay early, pay extra when possible, and confirm the lender applies extra money to principal. Before signing, ask two questions: Is this a simple interest loan? Is there a prepayment penalty? Those answers can determine whether paying off the loan early will actually save you money.