Understanding tax brackets is essential if you want to keep more of what you earn and avoid costly mistakes. Many people misunderstand how federal income taxes work, which can lead to unnecessary stress, poor financial decisions, or fear of earning more. Once you see how the system is structured, it becomes much easier to plan strategically and confidently.

How Federal Income Tax Brackets Work in the United States

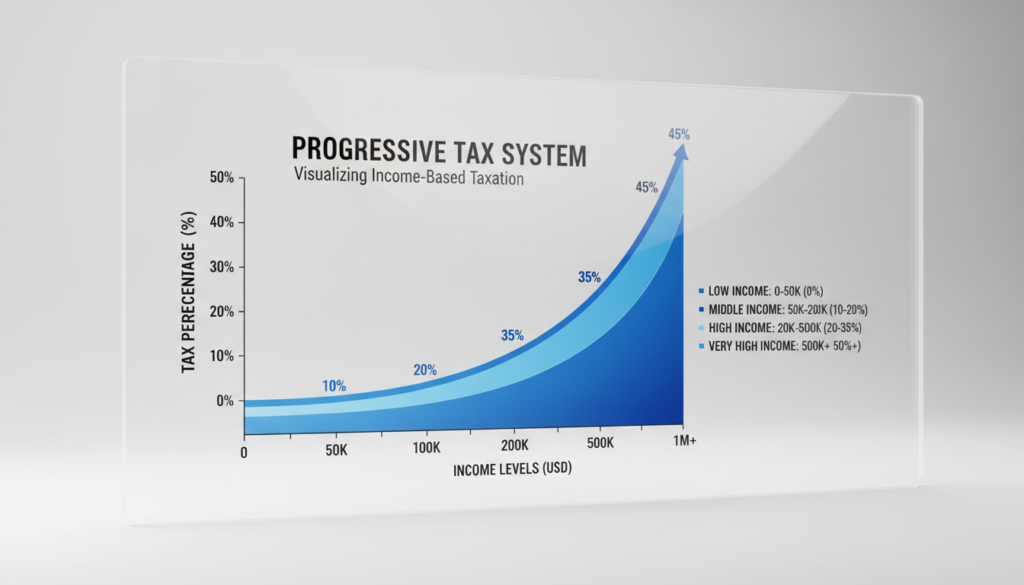

The federal income tax system is progressive. That means your income is taxed in layers, with different portions taxed at different rates. A common misconception is that if you move into a higher tax bracket, all of your income gets taxed at that higher rate. That isn’t how it works.

Instead, each bracket applies only to the income within that range. For example, if your income crosses into a higher bracket, only the dollars above that threshold are taxed at the higher rate. The rest of your income remains taxed at the lower rates. This structure encourages income growth without penalizing people for earning more. You won’t take home less money simply because you moved into a higher bracket.

Marginal Tax Rate vs. Effective Tax Rate

Two terms often cause confusion: marginal tax rate and effective tax rate. Your marginal tax rate is the rate applied to your last dollar of taxable income. If you’re in the 22 percent bracket, that doesn’t mean you pay 22 percent on everything. It means the top portion of your income falls into that bracket. Your effective tax rate is the average percentage of your total taxable income that you pay in taxes. Because of the progressive system, your effective rate is typically lower than your marginal rate. Understanding this difference is crucial when evaluating raises, bonuses, or additional income streams. A higher marginal rate doesn’t mean the entire amount is taxed at that rate.

Taxable Income Isn’t the Same as Gross Income

Another key concept is taxable income. Your tax bracket is based on taxable income, not your total earnings. Taxable income is calculated after subtracting adjustments, deductions, and certain contributions. For many households, this includes:

- The standard deduction or itemized deductions

- Pre tax retirement contributions

- Health Savings Account contributions

- Certain above the line deductions

Because of these adjustments, your taxable income may be significantly lower than your salary. This distinction matters when planning year end strategies, retirement contributions, or charitable giving.

Standard Deduction vs. Itemized Deductions

Most taxpayers use the standard deduction, which reduces taxable income by a fixed amount based on filing status. Others choose itemized deductions if their eligible expenses exceed the standard deduction. Itemized deductions may include mortgage interest, state and local taxes within limits, charitable contributions, and certain medical expenses. Choosing between standard and itemized deductions can directly affect which tax bracket your taxable income falls into. However, itemizing doesn’t always produce a better outcome. It depends on your individual situation and the current tax rules in place.

Filing Status and Its Impact on Tax Brackets

Your filing status plays a major role in determining your tax brackets. The most common categories include:

- Single

- Married filing jointly

- Married filing separately

- Head of household

Each status has different income thresholds for each tax bracket. Married couples filing jointly often benefit from wider bracket ranges compared to single filers, though that isn’t always advantageous in every scenario. Choosing the correct filing status is essential. Filing incorrectly can lead to overpaying taxes or facing penalties.

How Raises, Bonuses, and Side Income Affect Your Taxes

Many people hesitate to accept overtime, bonuses, or freelance income because they believe it’ll push them into a higher tax bracket and wipe out the benefit. That’s a misunderstanding of how marginal tax rates function. Only the portion of income that exceeds a bracket threshold is taxed at the higher rate. You still keep the majority of additional earnings.

However, additional income can have secondary effects. It may impact:

- Eligibility for certain tax credits

- Student loan repayment calculations

- Healthcare premium subsidies

- Medicare premium brackets later in life

That’s why proactive planning matters. While earning more is generally positive, understanding the broader implications helps you avoid surprises.

Tax Credits vs. Tax Deductions

Tax credits and tax deductions both reduce your tax bill, but they function differently. A deduction reduces your taxable income. A credit directly reduces the amount of tax you owe. Because of that, credits are typically more powerful on a dollar for dollar basis.

Common credits include the Child Tax Credit, the Earned Income Tax Credit, and education related credits. Some credits are refundable, meaning you can receive money back even if your tax liability is zero. Understanding the difference between credits and deductions can help you evaluate tax planning opportunities more effectively.

How State Income Taxes Fit Into the Picture

Federal tax brackets are only part of the equation. Many states also impose income taxes, each with its own structure. Some states use progressive systems similar to federal brackets. Others use flat rates, and a few don’t tax income at all. If you’re considering relocating, especially near retirement or for a job opportunity, state income taxes can materially affect your net income. Property taxes, sales taxes, and local taxes also play a role in your overall tax burden. Evaluating your full tax environment rather than focusing solely on federal brackets gives you a clearer financial picture.

Retirement Accounts and Their Influence on Tax Brackets

Retirement contributions can be one of the most effective ways to manage your tax bracket.

Traditional 401(k) and IRA contributions reduce taxable income in the year they’re made. This may keep you within a lower bracket or reduce the amount taxed at a higher marginal rate. Roth contributions don’t provide an upfront deduction, but qualified withdrawals in retirement are generally tax free. Choosing between traditional and Roth contributions often depends on your current bracket versus your expected future bracket.

For higher earners, tax bracket management can also influence decisions about Roth conversions, capital gains harvesting, and charitable strategies.

Capital Gains and How They’re Taxed Differently

Not all income is taxed at ordinary income tax rates. Long-term capital gains and qualified dividends are subject to separate tax brackets, which are often lower than ordinary income brackets. This creates planning opportunities. Selling appreciated investments in a year when your taxable income is lower may allow you to pay reduced capital gains rates. However, capital gains income can also affect eligibility for credits or increase Medicare premiums in later years. Coordinating investment decisions with overall tax planning is essential.

Common Misunderstandings About Tax Brackets

Several persistent myths create confusion around income taxes:

First, earning more money won’t cause you to take home less overall. The progressive system prevents that scenario.

Second, moving into a higher bracket doesn’t retroactively increase taxes on income already earned.

Third, withholding from your paycheck isn’t the same as your actual tax liability. A large refund doesn’t mean you paid less in taxes. It means you overpaid throughout the year.

Clearing up these misconceptions helps you make rational decisions rather than emotional ones.

Conclusion: Understanding Tax Brackets Leads to Smarter Financial Decisions

Tax brackets aren’t designed to punish success. They’re structured to apply progressively, meaning you’re only taxed at higher rates on the portion of income that exceeds certain thresholds. Once you understand the difference between marginal tax rates and effective tax rates, taxable income and gross income, and tax credits versus tax deductions, the system becomes far less intimidating.

For households across the country, tax awareness is a key part of financial planning. Whether you’re evaluating a raise, contributing to retirement accounts, or preparing for a major life change, understanding how the income tax system really works allows you to make informed decisions. Completely eliminating taxes isn’t the objective. The focus is on applying the rules wisely, limiting avoidable tax burdens, and shaping your strategy so it supports your long term financial goals.

Related Articles

- How to File Your Taxes in the U.S.: Step-by-Step Beginner’s Guide for Easy Filing

- Income Tax Calculation Explained: Simple Steps to Estimate What You Owe in the U.S.

- Freelancer Tax Guide: Key Rules, Deductions, and Simple Steps to Lower Your Tax Bill

- 10 Best Tax Software of 2026 for Easy Filing, Accurate Returns, and Maximum Refunds