Understanding income tax payable is a critical component of managing your business finances and ensuring you meet your tax obligations on time. This concept is not only essential for corporate financial reporting but also plays a vital role in cash flow management and tax strategy. This article explains what income tax payable is, how it’s calculated, and most importantly, how businesses can take steps to reduce their tax liabilities effectively.

What Is Income Tax Payable?

Income tax payable refers to the amount of tax that a business owes to the government, typically due within the year. It’s classified as a current liability on a company’s balance sheet, meaning it’s an amount that is expected to be paid within the next 12 months. This is separate from income tax expense, which represents the amount of tax that the business recognizes as part of its net income, but may not be due immediately.

Essentially, income tax payable reflects the exact amount that the company has to pay to the tax authorities, based on the taxable income calculated after all allowable deductions and credits. It’s a short-term financial obligation that businesses must be aware of to ensure their cash flow remains healthy.

How Is Income Tax Payable Calculated?

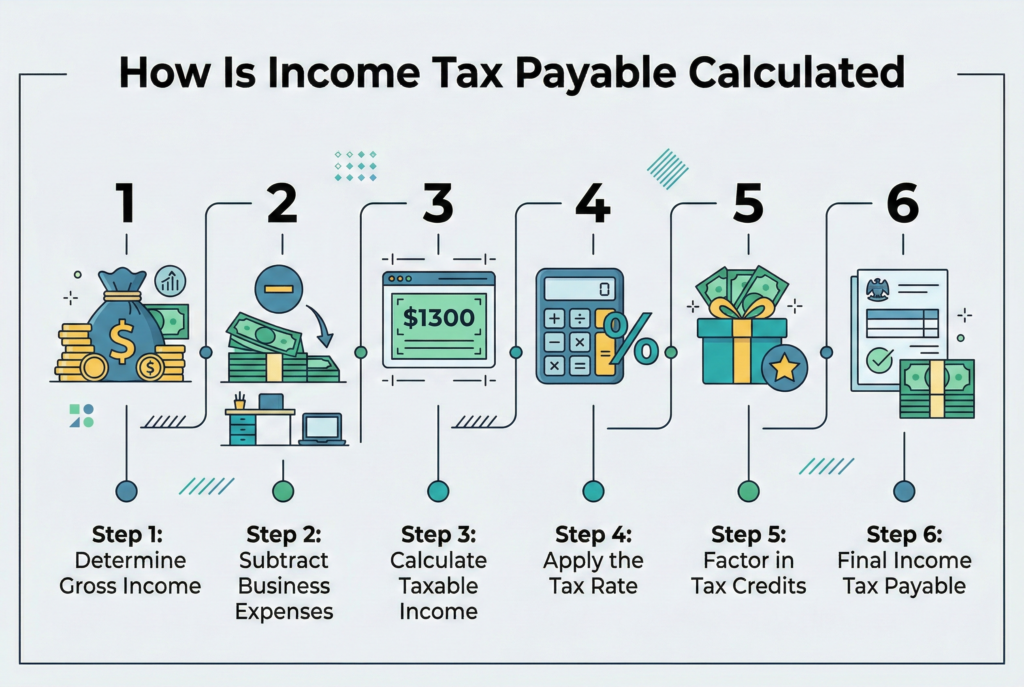

Step 1: Determine Gross Income

The first step is to calculate the gross income for the tax year. This includes all revenue earned from the business’s operations, excluding any expenses or deductions.

Step 2: Subtract Business Expenses

The business then subtracts deductible business expenses from its gross income. These may include operating costs, payroll, interest, depreciation, and other allowable deductions that reduce the total taxable income.

Step 3: Calculate Taxable Income

After deducting expenses, the taxable income is the amount that is subject to tax. This figure represents the business’s net income after all deductions are made.

Step 4: Apply the Tax Rate

The taxable income is then multiplied by the applicable corporate tax rate. In the U.S., this can range depending on the business’s revenue and structure. The tax rate may also be progressive depending on the total income, with higher rates applied to larger income brackets.

Step 5: Factor in Tax Credits

If the business qualifies for any tax credits, such as those for energy-efficient investments or R&D, these can reduce the total tax payable dollar-for-dollar.

Step 6: Final Income Tax Payable

The final amount owed is the income tax payable: the balance due to the IRS after accounting for tax credits and other adjustments.

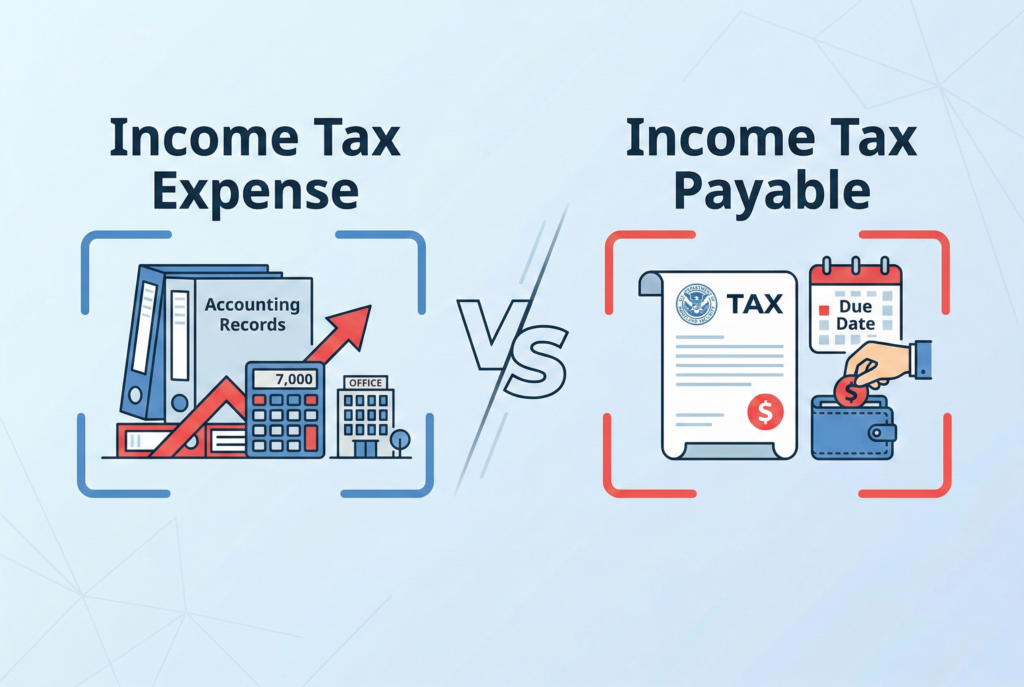

Income Tax Payable vs. Income Tax Expense

It’s crucial to distinguish between income tax payable and income tax expense. Though related, they refer to different aspects of tax accounting:

- Income Tax Payable: This is the actual liability the business must pay to the IRS within the current year. It’s recorded as a current liability on the balance sheet.

- Income Tax Expense: This is the expense recognized in the income statement, reflecting the business’s tax obligations for a given period. However, it may not match the actual amount paid because of timing differences between when tax is recognized and when it’s actually paid.

Understanding the difference between these two concepts is vital for accurate financial reporting. While income tax payable represents what you owe in the near term, income tax expense accounts for the total tax burden on your business for a given period.

How to Reduce Income Tax Payable: Practical Tips for Businesses

While businesses cannot avoid paying taxes, there are many ways to reduce income tax payable through careful planning, smart strategies, and taking full advantage of the tax laws.

Maximize Business Deductions

Ensure that all eligible expenses are deducted, including costs for supplies, wages, marketing, and operational costs. Keeping detailed records and receipts is essential for substantiating these deductions.

Take Advantage of Tax Credits

Explore available tax credits for things like energy-efficient improvements, hiring certain employees, or investing in research and development (R&D). These credits directly reduce the taxes owed, rather than just lowering taxable income.

Contribute to Retirement Plans

Contributions to employee retirement plans, like a 401(k) or IRA, can reduce taxable income. By funding these plans, businesses can lower their current-year tax burden while also providing benefits for their employees.

Defer Income or Accelerate Expenses

Consider deferring income to the next year or accelerating expenses into the current year to manage the taxable income. This strategy can be especially useful at the end of a tax year when trying to reduce the tax liability.

Use Net Operating Losses (NOL)

If your business had a loss in previous years, you can apply those losses to offset taxable income in the current year through the net operating loss carryforward or carryback provisions.

Invest in Tax-Advantaged Accounts

Consider utilizing tax-advantaged accounts, such as Health Savings Accounts (HSAs) or business savings plans, which allow businesses to make tax-deferred contributions that reduce their taxable income.

Regularly Consult a Tax Professional

One of the most effective ways to manage income tax payable is by consulting with a tax advisor or financial planner. Professionals can help ensure you’re taking advantage of all available deductions and credits, avoiding errors, and ensuring compliance with the tax laws.

Final Thoughts: Effective Management of Income Tax Payable

By understanding how income tax payable works and applying strategies to reduce it, businesses can not only improve their financial standing but also have more control over their cash flow. Careful planning, awareness of tax credits, and using expert advice are essential for minimizing the amount owed while remaining compliant with the IRS.

Ultimately, by managing taxes effectively, businesses can allocate more resources toward growth and investment, building a strong financial foundation for long-term success. Regularly reviewing tax strategies and staying informed on tax laws is key to ensuring your business thrives financially.