Bond funds can play an important role in a well-rounded investment portfolio, especially for investors who want income, diversification, or a way to reduce overall portfolio volatility. While stocks often get more attention for long-term growth, bond funds are widely used in retirement accounts, taxable portfolios, and income-focused strategies because they offer a different balance of risk and return.

What Are Bond Funds?

A bond fund is an investment fund that pools money from many investors and uses that money to buy a collection of bonds. Instead of purchasing one individual bond at a time, investors buy shares of the fund and gain exposure to a diversified basket of fixed-income securities.

These funds may hold government bonds, corporate bonds, municipal bonds, mortgage-backed securities, or a mix of several bond types. Some bond funds focus on short-term debt, while others invest in intermediate-term or long-term bonds. Certain funds concentrate on higher-quality bonds, while others seek higher yields by taking on more credit risk.

The main appeal is convenience. A single bond fund can provide diversified fixed-income exposure that would be harder for many individual investors to build on their own.

How Bond Funds Work

Bond funds work by collecting money from investors and allocating it across many bonds based on the fund’s investment objective. The fund manager or index methodology decides which bonds to buy, how long to hold them, and how the portfolio should be adjusted over time.

As the bonds inside the fund pay interest, that income is typically passed through to shareholders in the form of regular distributions. The share price of the fund, often called the net asset value for mutual funds, also changes as bond prices move up or down.

This is an important distinction. A bond fund doesn’t behave exactly like owning a single bond to maturity. With an individual bond, you generally know the face value and maturity date in advance, assuming the issuer doesn’t default. A bond fund has no single maturity date because it usually keeps buying and selling bonds within the portfolio. That means the fund’s value fluctuates continuously based on interest rates, credit conditions, and market demand.

Why Investors Use Bond Funds

Many investors use bond funds because they can provide steady income and help balance a portfolio that would otherwise be heavily concentrated in stocks. Bonds often respond differently from equities, which can make them useful for diversification.

For someone nearing retirement, already retired, or simply looking for a smoother investment experience, bond funds may offer a level of stability that stock funds don’t. They can also help investors keep part of their portfolio in assets that tend to be less volatile than stocks, though they aren’t risk-free.

Another reason investors choose bond funds is accessibility. Buying a wide range of individual bonds can require more capital, more research, and more ongoing management. A bond fund simplifies the process by packaging that exposure into one investment.

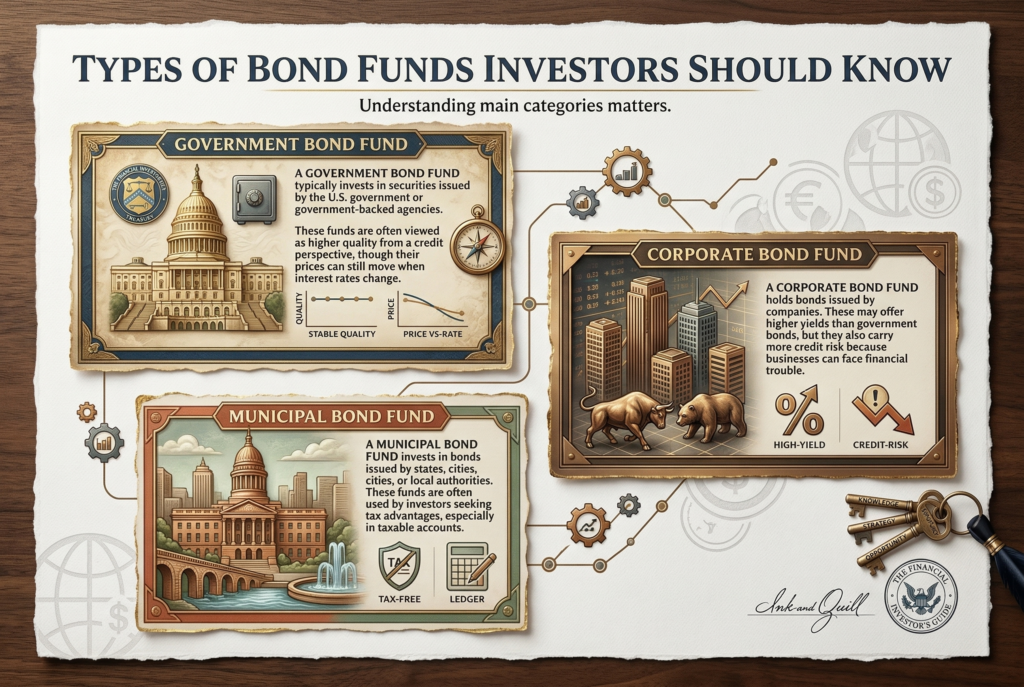

Types of Bond Funds Investors Should Know

Not all bond funds are the same, and understanding the main categories matters when choosing one.

A government bond fund typically invests in securities issued by the U.S. government or government-backed agencies. These funds are often viewed as higher quality from a credit perspective, though their prices can still move when interest rates change.

A corporate bond fund holds bonds issued by companies. These may offer higher yields than government bonds, but they also carry more credit risk because businesses can face financial trouble.

A municipal bond fund invests in bonds issued by states, cities, or local authorities. These funds are often used by investors seeking tax advantages, especially in taxable accounts.

There are also short-term bond funds, intermediate-term bond funds, and long-term bond funds. The main difference is maturity profile. Longer-term funds tend to be more sensitive to interest rate changes, while short-term funds generally carry less rate sensitivity.

Some investors also use high-yield bond funds, sometimes called junk bond funds. These funds invest in lower-rated bonds that offer higher income potential but also come with higher default risk and often more stock-like behavior during market stress.

Key Benefits of Bond Funds

One of the biggest advantages of bond funds is diversification. A single fund can hold dozens or even hundreds of bonds, which reduces the impact of any one issuer running into trouble. That can be especially valuable in corporate or high-yield bond categories.

Another major benefit is income. Bond funds generally make regular interest-based distributions, which can appeal to retirees or other investors who want cash flow from their portfolio. Even for investors who reinvest distributions, that income can contribute to long-term total return.

Bond funds can also support risk management. While they can decline in value, they’ve often been used to lower the overall volatility of a mixed stock-and-bond portfolio. That balance can help investors stay committed to their strategy during uncertain markets.

Professional management is another benefit. The fund manager handles credit analysis, trading, sector allocation, and portfolio adjustments. For investors who don’t want to research individual bonds, that can save time and improve convenience.

The Main Risks of Bond Funds

Even though bond funds are often seen as more conservative than stock funds, they still involve meaningful risks.

One of the biggest is interest rate risk. When interest rates rise, bond prices usually fall. This can cause bond fund values to decline, sometimes more than investors expect. Funds with longer average maturities are generally more sensitive to rate changes.

There’s also credit risk, which is the risk that a bond issuer won’t make interest payments or repay principal as expected. This is especially important in corporate bond funds and high-yield bond funds.

Another concern is inflation risk. If inflation stays high, the income produced by bonds may lose purchasing power over time. Even if a bond fund pays regular distributions, those payments may not stretch as far in real-world spending terms.

Bond funds also carry liquidity and market risk. In stressful markets, lower-quality bonds may become harder to sell at favorable prices, which can pressure fund performance.

Perhaps the most common misunderstanding is assuming bond funds can’t lose money. They absolutely can. Their prices move with the market, and some periods can be challenging, particularly when interest rates rise quickly or credit conditions worsen.

Bond Funds vs. Individual Bonds

Investors often compare bond funds with individual bonds, and each has different strengths. An individual bond has a set maturity date and face value. If the issuer remains financially sound and the bond is held to maturity, the investor usually knows what to expect in terms of principal repayment. That structure can feel more predictable.

A bond fund, by contrast, doesn’t mature. It owns many bonds and replaces holdings over time. This means the fund offers diversification and convenience, but it doesn’t provide the same certainty of principal repayment on a fixed date.

For many investors, bond funds are easier to use because they allow instant diversification and professional management. Individual bonds may appeal more to those who want to build a ladder or match specific maturity dates to future spending needs. Neither option is automatically better. It depends on the investor’s goals, time horizon, and interest in managing fixed-income holdings directly.

How Interest Rates Affect Bond Funds

Understanding interest rates is essential when evaluating bond funds. Bond prices and interest rates typically move in opposite directions. When new bonds are issued with higher yields, older bonds with lower yields usually become less attractive, and their prices fall.

This relationship affects bond funds every day. If rates rise, a fund’s share price may decline. If rates fall, bond prices often rise, which can support fund performance. The degree of sensitivity depends a lot on duration, a measure of how responsive a bond or bond fund is to changes in interest rates. Funds with longer duration generally experience larger price swings when rates change. That’s why two bond funds can behave very differently even if both are labeled fixed income.

For investors, this means the yield alone doesn’t tell the whole story. A fund offering more income may also be taking on more interest rate risk, more credit risk, or both.

How to Choose the Right Bond Fund

Choosing the right bond fund starts with understanding what role you want it to play in your portfolio. If you’re looking for stability and lower volatility, a short-term or high-quality bond fund may be more appropriate than a high-yield fund. If income is the main goal, you may be willing to accept more credit risk in exchange for a higher yield.

Pay attention to the fund’s holdings, average duration, credit quality, and category. A fund labeled bond fund can still vary significantly in risk depending on what it owns.

It’s also important to look at the expense ratio. Fees reduce returns, and in bond investing, where expected returns may be lower than stocks, costs matter even more. A high expense ratio can take a noticeable bite out of income.

You should also consider whether the fund is actively managed or index-based, how it has behaved in different market environments, and whether it overlaps with fixed-income exposure you already have elsewhere.

Who Might Benefit Most From Bond Funds

Bond funds can be useful for a wide range of investors. People nearing retirement often use them to reduce portfolio volatility and generate income. Retirees may use them as part of a withdrawal strategy or as a cushion against stock market downturns.

Younger investors can also benefit from bond funds, especially if they want a more balanced portfolio or need money for medium-term goals that don’t fit an all-stock strategy. Even growth-oriented investors often use some fixed-income allocation to manage risk and improve diversification.

The right percentage depends on age, goals, time horizon, and tolerance for fluctuations. Bond funds aren’t only for conservative investors. They’re a tool that can be adjusted to fit many different financial situations.

Conclusion

Bond funds can be a valuable part of an investment portfolio because they offer income, diversification, and a practical way to access the fixed-income market without buying individual bonds one by one. They can help balance risk, support retirement planning, and provide a steadier counterweight to stock exposure. At the same time, they aren’t risk-free. Interest rate risk, credit risk, inflation risk, and fund costs all matter when evaluating options. By understanding how bond funds work and choosing one that matches your goals, time horizon, and risk tolerance, you can use them more effectively as part of a thoughtful long-term investment strategy.