Tax breaks can make a meaningful difference in how much you owe each year, but many people aren’t fully sure what counts as one or how to use them wisely. In simple terms, a tax break is any legal provision that reduces your taxable income or directly lowers your tax bill. Once you understand the main types and where they apply, it becomes much easier to make smarter financial decisions and keep more of your money.

What Are Tax Breaks?

A tax break is a broad term for a tax benefit that helps reduce the amount of tax you owe. Some tax breaks lower your taxable income, while others reduce your tax bill dollar for dollar. That distinction matters because not all tax savings work the same way.

For example, a tax deduction reduces the amount of income the government taxes. A tax credit reduces the actual amount of tax you owe. There are also exclusions, exemptions in limited contexts, and special tax-advantaged accounts that can lower your overall tax burden in different ways.

That’s why the phrase tax breaks covers more than one concept. It’s a practical umbrella term that includes several tools built into the tax code to encourage certain financial behaviors, support families, promote education, homeownership, retirement savings, healthcare planning, and small business activity.

How Tax Breaks Work

The easiest way to understand tax breaks is to think of them in two categories. The first category lowers the income that gets taxed. These include things like certain deductions, adjustments to income, and contributions to eligible accounts. If your taxable income goes down, the amount of tax calculated on that income may also go down.

The second category lowers your final tax bill directly. This is where tax credits come in. Credits are often more valuable than deductions because they reduce the tax owed itself rather than only shrinking the income used to calculate it. For example, if a deduction reduces your taxable income by $1,000, your actual savings depend on your tax bracket. But if you qualify for a $1,000 credit, that usually cuts your tax bill by the full $1,000. This is one reason people often misunderstand how to lower taxes. They may hear about a tax break and assume every option works the same way, when in reality the structure of the benefit can greatly affect how much it helps.

Main Types of Tax Breaks

Tax Deductions

A tax deduction reduces the portion of your income subject to tax. Some deductions are available even if you don’t itemize, while others only help if you choose to itemize on your tax return.

One of the biggest decisions for many taxpayers is whether to take the standard deduction or itemize deductions. The standard deduction is simpler and often more beneficial for people whose deductible expenses don’t add up to more than that amount. Itemizing may make sense if you have enough qualifying expenses, such as mortgage interest, charitable donations, or certain medical expenses, to exceed the standard deduction.

There are also above-the-line deductions, sometimes called income adjustments. These can include eligible contributions to certain retirement accounts, health savings account contributions, student loan interest in qualifying cases, and some self-employment-related deductions. These benefits can reduce adjusted gross income, which may also improve eligibility for other tax advantages.

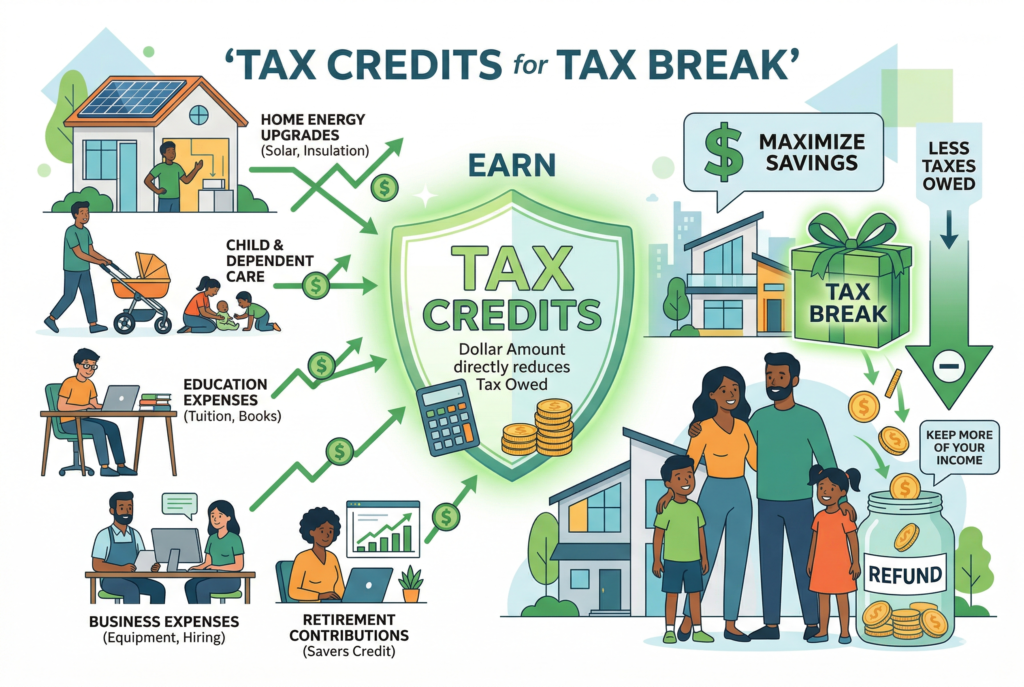

Tax Credits

Tax credits are often the most powerful type of tax break because they directly reduce how much tax you owe. Some are nonrefundable, which means they can reduce your bill to zero but not below it. Others are refundable, meaning you may still receive money back even if your tax liability is already reduced to zero.

Common credits may apply to children, education expenses, dependent care, energy-efficient home improvements, or lower- to moderate-income workers who qualify under specific rules. The value of a credit depends on eligibility requirements, income limits, filing status, and the exact structure of the credit. Because credits can be highly valuable, they’re worth reviewing carefully each tax year. Missing one can mean paying more than necessary.

Tax-Advantaged Accounts

Some of the most useful tax breaks come from accounts designed to reward long-term planning. Retirement accounts such as traditional IRAs and employer-sponsored plans may offer tax benefits either now or later, depending on the account type. Health savings accounts can also provide strong tax advantages for eligible individuals with qualifying health plans.

These accounts matter because they can support multiple goals at once. You may be preparing for retirement or medical costs while also lowering current taxable income. In many cases, that’s more effective than looking for last-minute deductions near tax filing season.

Tax Exclusions and Special Rules

Not every tax break shows up as a deduction or credit. Some income may be excluded from taxation under specific rules, and some employer-provided benefits may receive favorable tax treatment. This area can become more technical, but the key point is simple: sometimes tax savings come from income not being fully taxed in the first place. That’s another reason tax planning works best when you look at your full financial picture instead of chasing one isolated deduction.

Who Benefits Most from Tax Breaks?

Almost every taxpayer can potentially benefit from tax breaks, but the specific opportunities vary depending on income, family structure, and financial goals.

Working families often focus on credits tied to children, childcare, education, and earned income. Homeowners may look more closely at mortgage-related deductions and property-tax-related rules where applicable. Students and parents paying for college may find value in education-related tax benefits. Self-employed workers often have access to business deductions and retirement planning opportunities that employees don’t use in the same way.

People saving for retirement may gain from traditional retirement contributions, while those with eligible health plans may benefit from HSA tax advantages. In other words, the best tax breaks depend less on what sounds popular and more on how your finances are structured.

Easy Ways to Lower Your Tax Bill Legally

One of the simplest ways to reduce taxes is to review whether you’re taking the right deduction path. Many people automatically accept the standard deduction, which is often the right choice, but some could save more by itemizing. Another smart move is contributing to eligible retirement accounts before the tax deadline when allowed. This can reduce taxable income while strengthening long-term savings.

If you have access to a Health Savings Account, using it strategically may also lower taxes. For eligible taxpayers, HSAs can offer tax-deductible contributions, tax-deferred growth, and tax-free withdrawals for qualified medical expenses.

Families should also take time to review available tax credits instead of only focusing on deductions. Credits tied to dependents, education, or care expenses may offer bigger savings than expected. For self-employed individuals, keeping accurate records is essential. Business-related deductions can be valuable, but only if expenses are documented properly.

Waiting until tax season to sort through everything often leads to missed opportunities. It’s also wise to plan before year-end instead of after the calendar turns. Many of the best tax-saving moves happen before December 31, not during filing season when fewer options remain.

Conclusion

Tax breaks are one of the most practical tools for lowering your tax bill, but they work best when you understand the differences between deductions, credits, and other tax-saving opportunities. Some reduce taxable income, some directly reduce taxes owed, and others reward long-term choices involving retirement, healthcare, education, or family expenses.

The most effective approach is to look at tax planning as part of a broader financial strategy. When you use the right tax deductions, claim eligible tax credits, and take advantage of tax-advantaged accounts where appropriate, you put yourself in a stronger position not just at tax time, but throughout the year. Done carefully, these legal tax breaks can help you keep more of what you earn and make your money work harder for your future.