Do you pay taxes on CD interest? Yes, and that is exactly why using a CD interest calculator before opening a CD matters more than most people think. Many savers focus only on APY, but your real return depends on how interest is taxed, when it is reported, and whether you may need access to your money before maturity.

A simple certificate calculator can show you how much your CD might grow. But if you want to make smarter decisions, you also need to understand after tax returns, not just the headline numbers. That is what separates a good savings plan from a great one.

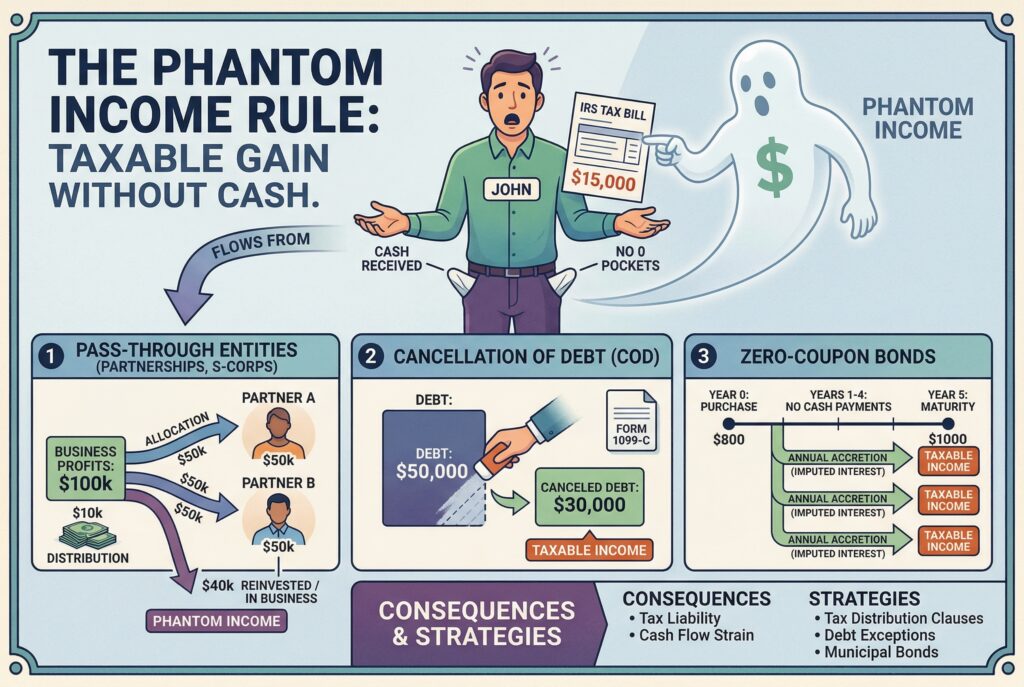

The Phantom Income Rule: Taxes Before Maturity

One of the most important things to understand is that CD interest is usually taxed in the year it is earned, not just when the CD matures. This often surprises people. Your money may still be locked in the CD, but the interest credited during the year is still considered taxable income. That is why many savers feel like they are paying taxes on money they haven’t actually received yet.

So, how does a CD account work in this situation? A CD earns interest based on its rate and compounding schedule. As long as that interest is credited or available to you, it becomes taxable, even if you leave it untouched. This matters even more with long term CDs. A five year CD doesn’t mean you only deal with taxes at the end. It often creates a tax obligation every year along the way.

How to Report CD Taxes: 1099 INT and Form 1040

Once your CD starts earning interest, reporting becomes straightforward. If you earn more than $10 in interest during the year, your bank will typically send you a Form 1099 INT. This form shows the amount of interest you earned and must report on your tax return.

You’ll include this interest as ordinary income on your Form 1040. For most people, this is the main step. There is no complex process, but it’s important to report it correctly every year. Understanding this reporting flow helps you avoid surprises and ensures that your projected returns from a CD interest calculator match what you actually keep after taxes.

The Math Behind the Returns: APR Formula and Percent Yield

If you want to fully understand your earnings, it helps to know how the numbers work.

APR Formula

The basic APR formula is:

This formula gives you a simple estimate, but CDs usually involve compounding, which means your actual return is better reflected by APY.

How to Calculate Percent Yield

To understand how to calculate percent yield, divide the interest earned by your original deposit and convert it into a percentage. For example, if you invest $10,000 and earn $450 in a year, your yield is 4.5%. Over time, compounding increases your total return, which is why a certificate calculator or CD interest calculator is useful for longer terms.

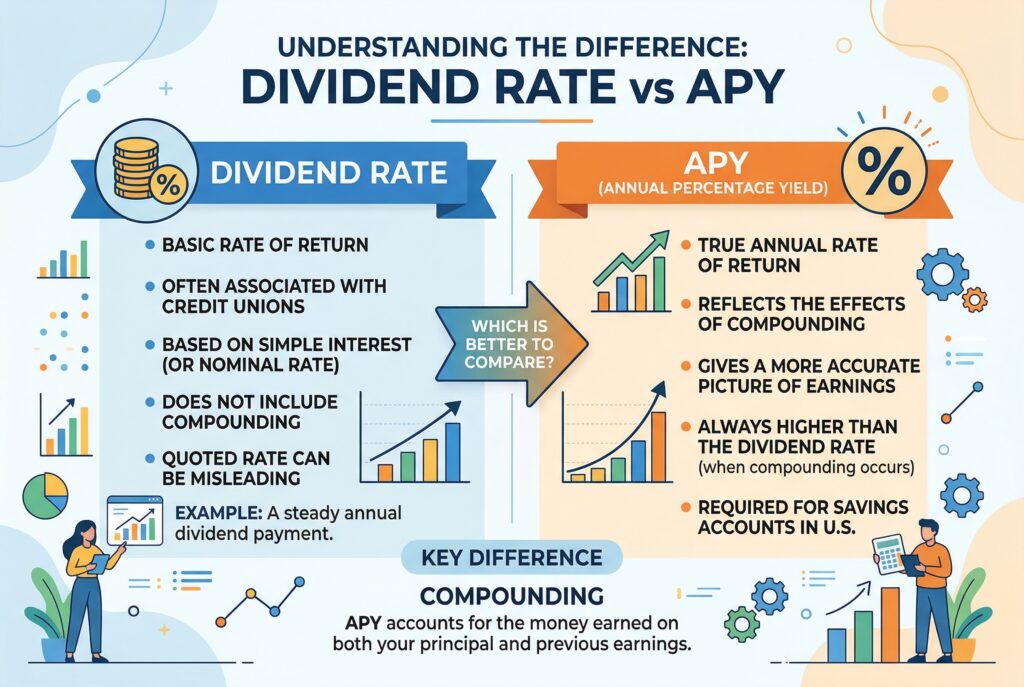

Dividend Rate vs APY

Many savers confuse dividend rate vs APY. The dividend rate is the base interest rate. APY includes compounding, which shows your true annual return. When comparing CDs, APY is usually the better number to focus on. However, for tax purposes, what matters is the actual interest credited, not just the advertised rate.

Tax Deductions: How Early Withdrawal Penalties Help

Breaking a CD early usually comes with a penalty, but there is one small advantage. In many cases, an early withdrawal penalty can be deducted as an adjustment to income. This means it may reduce your taxable income for that year. That doesn’t make early withdrawal a good strategy. It still reduces your overall return. But if you are forced to withdraw early, the penalty may have some limited tax benefit instead of being a complete loss.

How to Defer or Avoid CD Taxes Legally

If you want to reduce the impact of taxes, the best option is to use tax advantaged accounts. Holding a CD inside a Traditional IRA allows you to defer taxes until withdrawal. A Roth IRA can allow qualified earnings to be tax free. Other options, such as education focused accounts, may also provide tax benefits depending on how funds are used. For many savers, the difference is significant. A CD in a regular account creates yearly tax friction. A CD in the right account structure can improve long term results.

Strategic Comparison and Cash Allocation: CD vs Money Market

Understanding taxes is important, but your overall cash strategy matters just as much. When comparing CD vs money market accounts, the key difference is simple. A CD offers fixed returns with limited access. A money market account offers flexibility with variable returns. A balanced approach often works best. One effective strategy is to allocate around 60% of your savings into CDs for stability and 40% into a liquid account for flexibility.

This helps you avoid breaking a CD just to access cash or pay taxes. It also gives you a mix of predictable growth and accessible funds. You can use a money market calculator or money market account calculator to estimate how the liquid portion of your savings may perform.

Beyond a Single Term: Try a CD Ladder Calculator

If you want more flexibility without giving up the benefits of CDs, laddering is a strong strategy. A CD ladder calculator helps you divide your savings across multiple CDs with different maturity dates. Instead of locking everything into one term, you create a schedule where part of your money becomes available regularly. This reduces risk, improves liquidity, and allows you to adapt if interest rates change over time.

Where to Find the Best CD Rates Today

After understanding how taxes work, the next step is choosing the right CD. Don’t focus only on the highest APY. Look at term length, penalties, minimum deposit requirements, and how the CD fits your financial goals. Many savers compare options like Keybank CD rates, Becu CD rates, Associated Bank CD rates, and Schwab CD rates to get a better sense of the market. The best rate isn’t always the best choice. The right account is the one that matches your timeline, liquidity needs, and tax strategy.

Conclusion

So, do you pay taxes on CD interest? Yes, and in most cases, that tax is applied every year as the interest is earned. But the real takeaway goes further. A CD interest calculator helps you estimate growth. A certificate calculator helps you plan your timeline. A tax aware strategy helps you keep more of what you earn. When you combine smart planning, proper reporting, and the right mix of CD and liquid savings, your results become much stronger than simply chasing the highest rate.