A checking account is one of the most practical financial tools for managing day-to-day expenses, paying bills, receiving income, and keeping money accessible when you need it. For many households, it serves as the center of everyday banking because it makes spending, saving, and tracking cash flow far more organized than relying on cash alone.

What Is a Checking Account?

A checking account is a deposit account offered by banks and credit unions that’s designed for frequent transactions. Unlike accounts built mainly for long-term saving, a checking account gives you easy access to your money through a debit card, online banking, checks, ATM withdrawals, direct deposit, and electronic transfers.

People often use checking accounts for routine financial activity such as getting paid, paying rent or a mortgage, covering utility bills, shopping for groceries, and managing subscription payments. Because the money is meant to stay readily available, checking accounts usually pay little or no interest compared with savings accounts. What makes this type of account so useful is convenience. Instead of juggling multiple payment methods or carrying large amounts of cash, account holders can move money quickly and monitor transactions in real time.

How a Checking Account Works in Everyday Life

When you open a checking account, you deposit money into it and use that balance for daily spending and bill payments. Funds can enter the account through cash deposits, checks, bank transfers, or direct deposit from an employer or government benefits provider. Once the money is available, you can spend or transfer it in several ways.

A debit card is one of the most common tools connected to a checking account. When you swipe, tap, or make an online purchase, the money is typically deducted directly from your available balance. You can also pay using ACH transfers, online bill pay, peer-to-peer payment apps, and, in some cases, paper checks.

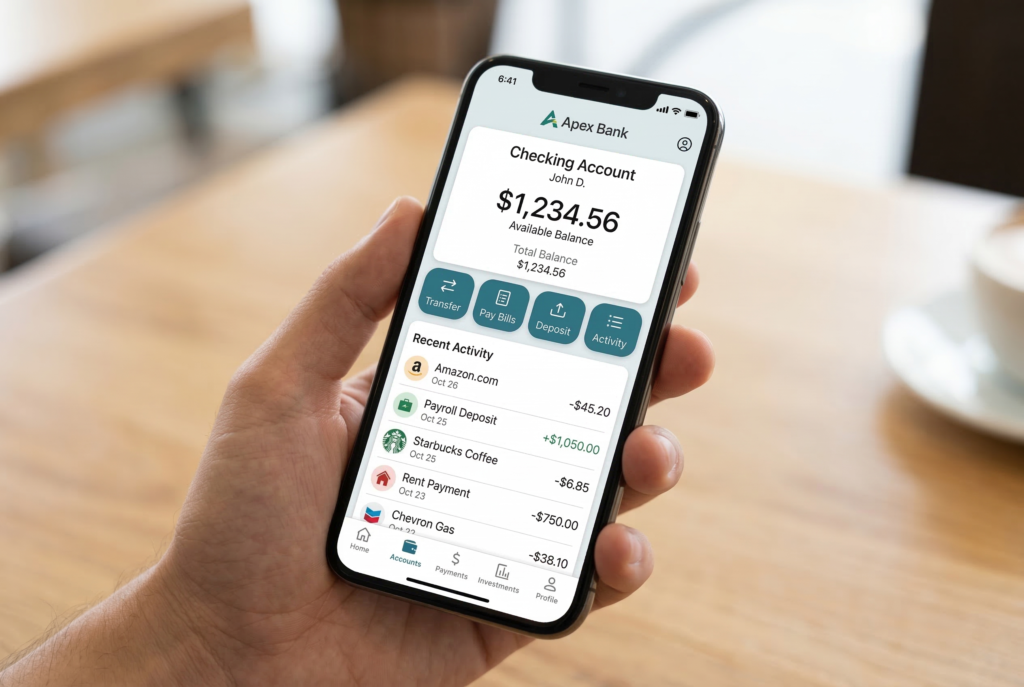

Most financial institutions now provide mobile apps that let customers review balances, deposit checks remotely, set alerts, freeze a card, and track spending patterns. That level of access helps people make better decisions because they can see where their money is going instead of waiting for a monthly paper statement. In simple terms, a checking account works as your financial operating hub. Income comes in, expenses go out, and your transaction history creates a clear record of how you manage money.

Why a Checking Account Is Essential for Money Management

A checking account plays an essential role in responsible money management. Without one, everyday financial tasks can become slower, more expensive, and harder to track.

First, it helps create structure. When paychecks are deposited into one secure account and regular bills are paid from that same place, budgeting becomes easier. You can review past transactions, identify spending habits, and spot recurring expenses that might otherwise go unnoticed. Second, it supports faster payments. Many employers prefer direct deposit, and many service providers encourage automatic or online payments. A checking account makes both possible. That reduces the risk of missed due dates and late fees.

Third, it improves security compared with carrying cash or using alternative financial services for every transaction. If a debit card is lost or stolen, it can often be locked quickly through an app or customer service line. Cash, on the other hand, generally can’t be recovered. Finally, a checking account can help build a stronger financial foundation. It often acts as the starting point for opening other products such as savings accounts, credit cards, loans, or certificates of deposit. For people working toward greater financial stability, that relationship can matter over time.

Key Features to Look for in the Best Checking Account

Not all checking accounts are the same, so it’s worth comparing features before opening one. The right choice depends on your spending habits, income pattern, and how you prefer to bank.

One important factor is the monthly maintenance fee. Some accounts charge a recurring fee unless you meet certain conditions, such as maintaining a minimum balance or receiving direct deposits. Others are marketed as no-fee checking accounts, which may be appealing for people who want to keep banking costs low.

ATM access also matters. If you withdraw cash regularly, look for a bank or credit union with a strong ATM network or reimbursement for out-of-network fees. Limited ATM options can quietly increase costs over time. Digital tools are another major consideration. A good mobile app, real-time alerts, mobile check deposit, and simple online transfers can make account management much easier. In everyday life, convenience often determines whether a banking experience feels efficient or frustrating.

Some checking accounts also offer perks such as early direct deposit, cash-back debit card rewards, overdraft protection options, or budgeting insights. These extras shouldn’t overshadow the basics, but they can add value when the account already fits your core needs.

Checking Account vs. Savings Account

Many people confuse checking and savings accounts, especially when they’re first learning about personal finance. While both hold deposited money, they serve different purposes. A checking account is designed for frequent use. It’s where money moves in and out regularly. You use it to pay bills, make purchases, send transfers, and receive deposits. Accessibility is the main priority.

A savings account, by contrast, is meant for money you don’t plan to spend every day. It’s better suited for emergency funds, short-term goals, or future expenses. Savings accounts often pay more interest, but they aren’t meant to function as your main spending account. The two accounts work best together. Many people keep enough in checking to cover routine expenses while moving extra funds into savings for upcoming goals and unexpected costs. That separation can reduce overspending and make progress easier to measure.

Common Fees and Mistakes to Avoid

Even a useful checking account can become expensive if you ignore the fine print. One of the most common issues is overdrafting, which happens when you spend more money than you have available. Depending on the account, that can lead to overdraft fees, declined transactions, or transfers from a linked backup account.

Another common mistake is overlooking monthly service charges. Some people open an account without realizing that avoiding the fee requires a minimum balance or recurring direct deposit. If those requirements aren’t met, the account becomes more costly than expected. Out-of-network ATM fees can also add up, especially if both your bank and the ATM operator charge separate amounts. It’s smart to know where you can withdraw cash for free before you need it. There’s also the issue of poor monitoring. When people don’t check their balances regularly, they’re more likely to miss fraud, duplicate charges, or subscription renewals they forgot to cancel. Reviewing transactions consistently is one of the simplest habits that supports better financial control.

Who Should Open a Checking Account?

A checking account is useful for almost anyone who earns, spends, or manages money on a regular basis. Students often need one for part-time job income and basic expenses. Working adults use it for payroll deposits, rent, utilities, groceries, and debt payments. Families rely on checking accounts to organize household cash flow and manage shared financial responsibilities.

It can also be especially important for people who want to move away from costly alternatives such as check-cashing services or prepaid debit cards with multiple fees. A well-chosen checking account can lower transaction costs and make money management more predictable.

For those opening an account for the first time, the best starting point is usually an option with low fees, strong digital banking tools, and simple account requirements. A checking account doesn’t need to be complicated to be effective. It just needs to support your actual financial life.

How to Choose the Right Checking Account for Your Needs

Choosing the right account starts with understanding your habits. If you use digital banking for nearly everything, an online bank might offer the convenience and low fees you want. If you value in-person service, a local bank or credit union may be a better fit.

Think about how often you use ATMs, whether direct deposit is available to you, how much balance you typically keep, and whether you want features like overdraft buffers or account alerts. These details make a real difference in how well an account supports your routine. It also helps to read the fee schedule carefully. A checking account may look attractive at first glance, but small charges can reduce its overall value. The best account is usually the one that feels easy to use, keeps costs manageable, and matches the way you already handle money.

Conclusion

A checking account plays a central role in everyday money management because it keeps your finances accessible, organized, and easier to control. From direct deposit and debit card purchases to bill payments and budgeting, it supports the transactions most people handle every week. When chosen carefully, the right account can reduce fees, improve financial visibility, and make daily banking far more efficient. For anyone looking to build stronger financial habits, a checking account isn’t just helpful. It’s one of the most essential tools for managing money with confidence.