If you’ve opened your credit card app and seen two different numbers at once, you aren’t overthinking it. The confusion around statement balance vs current balance is one of the most common credit card questions because both numbers look important, and both technically are. But they serve different purposes. The good news is that once you understand which one matters for interest and which one matters for real-time account tracking, the decision gets much easier.

This is the core issue most people are really trying to solve: which balance should you actually pay if you want to avoid interest, stay in control of your credit card statement, and protect your credit score? The answer is simpler than it looks.

The Short Answer: Which Balance Should You Pay?

If your goal is to avoid paying interest, you only need to pay the statement balance in full by the due date. You don’t have to pay the current balance to avoid interest. That’s the most important rule in this whole topic.

Your statement balance is the amount the issuer officially billed you for the last completed billing cycle. If you pay that amount in full and on time, you usually keep your grace period. That means new purchases made after the statement closed won’t start generating interest right away.

Your current balance is the more up-to-date number. It includes the statement balance, plus any new purchases, minus payments you’ve already made, and sometimes other posted activity. It’s useful, but it isn’t the number you must pay to avoid interest in a normal grace-period situation.

What Is a Statement Balance? The Locked Number

The easiest way to think about statement balance is as a snapshot. It is the amount you owed on the last day of your previous billing cycle. Once that statement is generated, that number is locked in. It won’t change just because you go out the next day and buy groceries, book a hotel, or pay for streaming services. Those newer purchases belong to the next cycle, not the statement that has already closed.

This is why the statement balance matters so much. It’s the official bill for that cycle. When people ask what amount they need to pay, this is usually the number that matters most.

Your credit card statement may also show a minimum payment, but paying only the minimum usually means you’ll keep carrying debt and may pay interest. The statement balance is the number that clears the full billed amount for that month.

What Does Current Balance Mean on a Credit Card? The Live Number

What does current balance mean on a credit card? Current balance is the live, running total of what you owe right now. It usually includes your statement balance, any new purchases made after the statement closed, any fees or interest that have been posted since then, and any payments or credits that have already been applied. That’s why current balance can be higher or lower than the statement balance.

If you’ve kept spending after the statement date, your current balance will usually be higher. If you already made a payment, it may be lower. If you get a refund, that can lower it too. The key idea is that current balance is dynamic. It changes as your account activity changes. So when people ask what does current balance mean or what does current balance mean on a credit card, the simplest answer is this: it’s the live amount currently owed, not the fixed amount you were billed for the last cycle.

Interactive Credit Card Payment Simulator

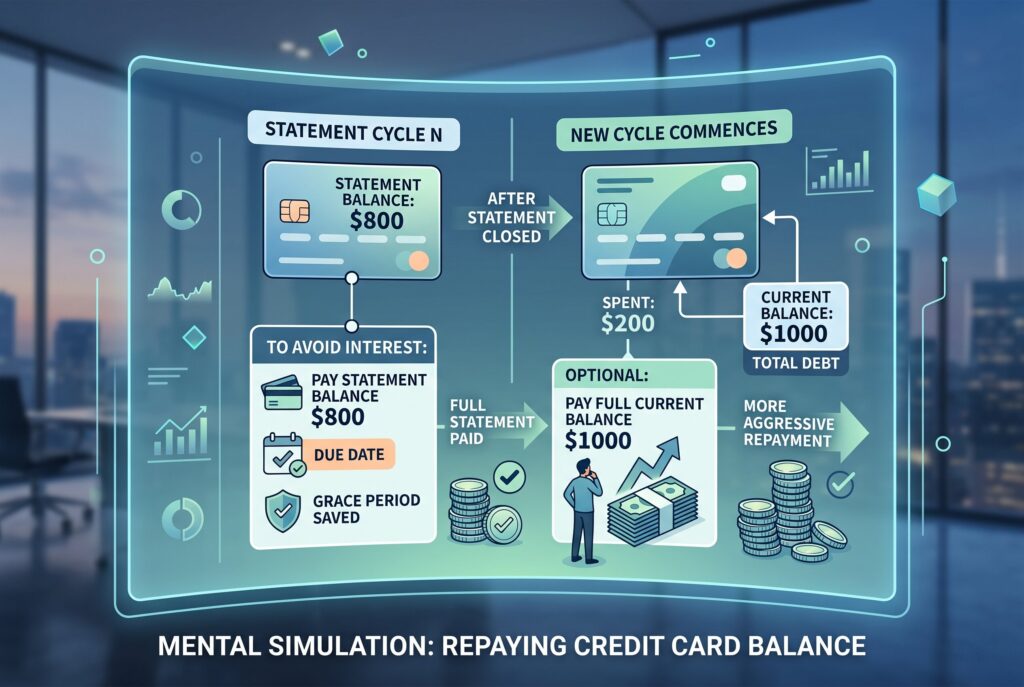

A helpful way to think about this is through a simple mental simulation. Imagine your statement balance is $800. After the statement closes, you spend another $200 on everyday purchases. Now your current balance is $1,000.

If you pay the $800 statement balance by the due date, you’ve done enough to avoid interest on the billed amount and preserve your grace period in a typical account situation. The extra $200 remains on the account, but it belongs to the next statement cycle. If you choose to pay the full $1,000 current balance, that’s also fine. You’ll reduce your balance more aggressively, and it may help with utilization. But it isn’t required to avoid interest in the usual grace-period scenario. That’s the distinction many cardholders miss.

Strategy Guide: When to Pay Which Balance

The best payment choice depends on your goal.

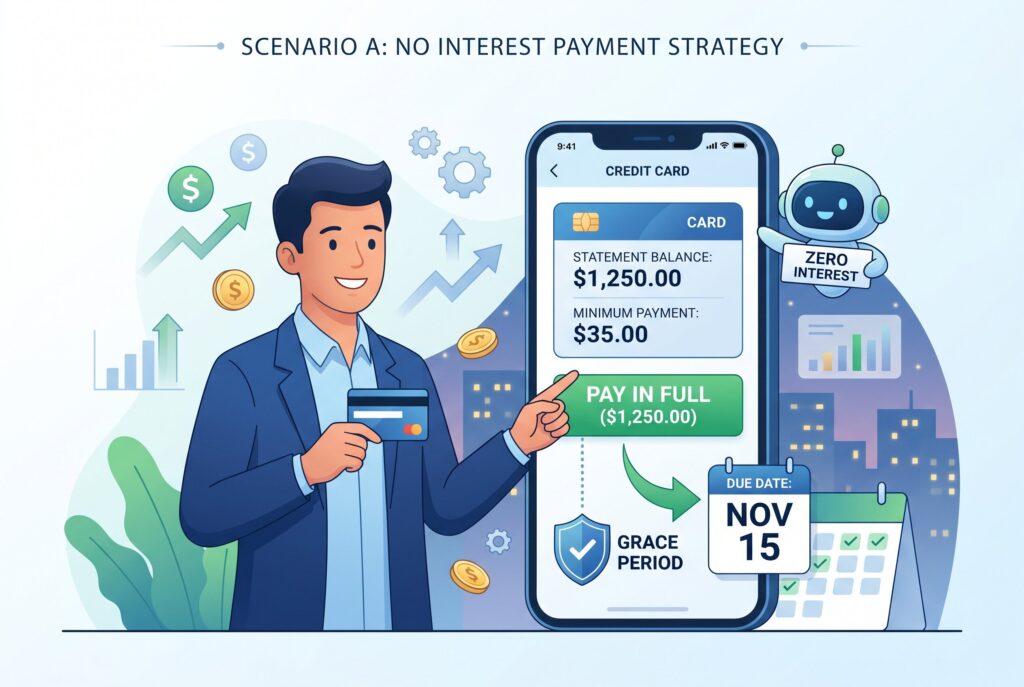

Scenario A: You Want to Pay Zero Interest

Pay the statement balance in full by the due date. This is the cleanest strategy for most cardholders. As long as your grace period is active, paying the full statement balance means you aren’t charged interest on that billed amount. New purchases made after the statement closed usually won’t start accruing interest immediately because they belong to the next cycle. If your goal is simple and sustainable, this is the best default rule.

Scenario B: You Want to Maximize Your Credit Score

Pay the current balance early, or at least reduce it before the statement closes. This is where credit utilization comes in. Utilization is the percentage of your credit limit that appears in use when the issuer reports your balance. If you wait until the due date, the reported balance may still reflect a higher amount from the statement-closing date. If you pay earlier and reduce the current balance before the statement generates, the reported utilization may be lower. This strategy matters more if you have a low credit limit, you’re preparing for a loan application, or you’re actively trying to optimize your score.

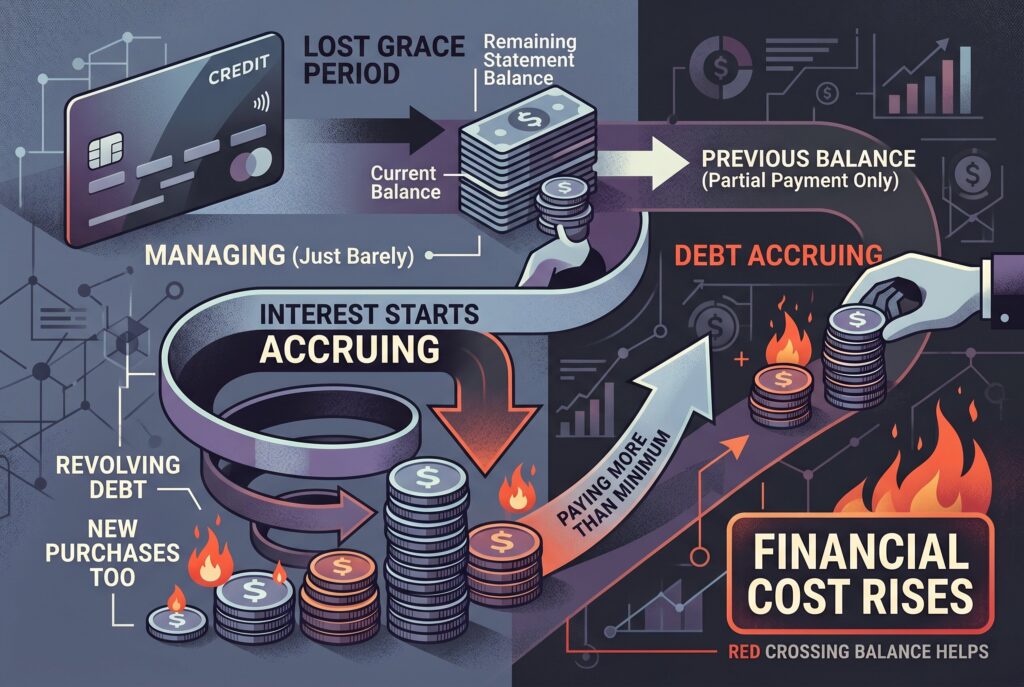

Scenario C: You Are Carrying Debt Month to Month

This is where remaining statement balance vs current balance becomes more serious. If you can’t pay the full statement balance, you may lose your grace period. Once that happens, interest can start accruing on revolving balances and often on new purchases too. In that case, the distinction between statement balance and current balance doesn’t disappear, but the financial cost of carrying debt becomes the bigger issue. If you’re in this situation, paying more than the minimum is usually important. The closer you get to paying off the remaining statement balance, the faster you reduce interest pressure.

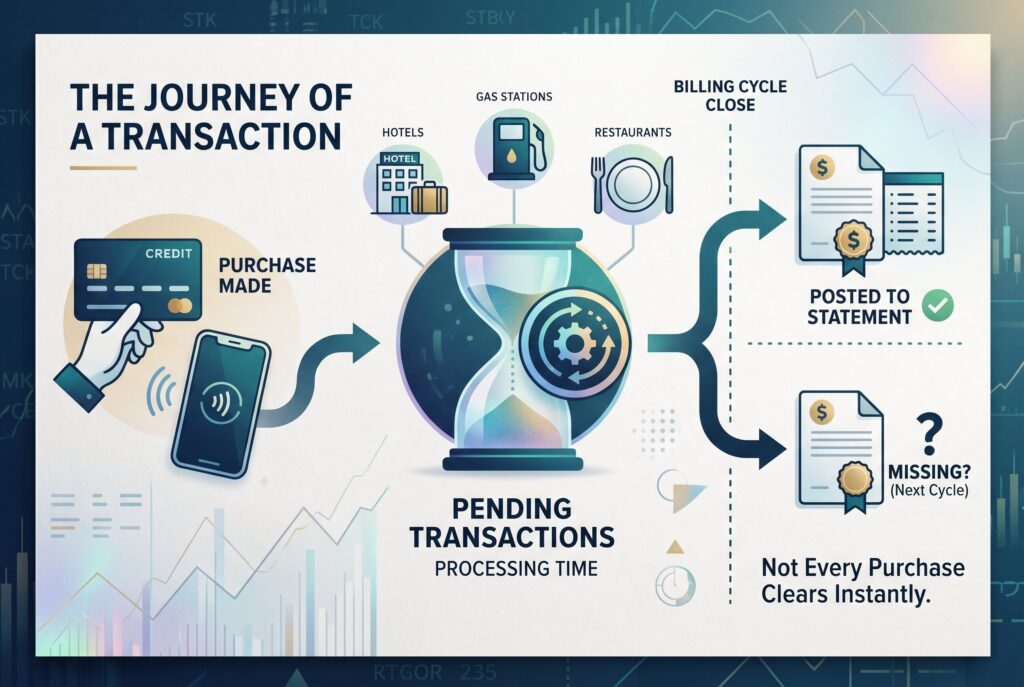

Missing Charges: Why Wouldn’t Every Purchase Show Up on Your Statement?

Why wouldn’t every purchase you made show up on your account statement? Because of pending transactions. Not every purchase clears instantly. Some transactions stay pending for a short time before they officially post. If you make a purchase near the exact end of your billing cycle, it may not be clear in time to appear on the statement that just closed. Instead, it shows up in your current balance and lands on the next statement.

This is especially common with certain merchants. Hotels, gas stations, and some restaurants may place authorization holds first. Those holds can affect what you see in your account activity before the final posted amount appears on the credit card statement. So if something seems missing, it usually isn’t gone. It’s just still moving through the system.

Conclusion

The simplest takeaway is this: if you want to avoid interest, pay the statement balance in full by the due date. If you want to lower your reported utilization and keep your balance especially clean, paying the current balance earlier can be useful too.

That’s why statement balance vs current balance matters. One is the fixed bill for the last cycle. The other is the live number that keeps changing. Once you understand that difference, your credit card statement becomes much easier to manage. A smart next step is setting up AutoPay for the full statement balance. That way, you protect your grace period, avoid missed payments, and keep earning rewards without paying unnecessary interest.

Related Articles

Current Balance vs Available Balance: Why They’re Different and How to Avoid Overdraft Fees