If you’re looking into recasting mortgage options, you’re probably trying to solve a very specific problem. You want lower monthly payments, but you don’t want to lose the low interest rate already attached to your loan. That’s exactly why a mortgage recast calculator matters. Instead of replacing your mortgage entirely, a recast lets you reduce your principal with a lump sum and keep the same loan structure. For many homeowners, that makes it one of the smartest ways to improve cash flow without stepping into a brand new mortgage.

This guide breaks the process down in plain English. You’ll see what recasting actually means, how to estimate the savings, when it beats refinancing, and what rules determine whether your loan can even be recast in the first place.

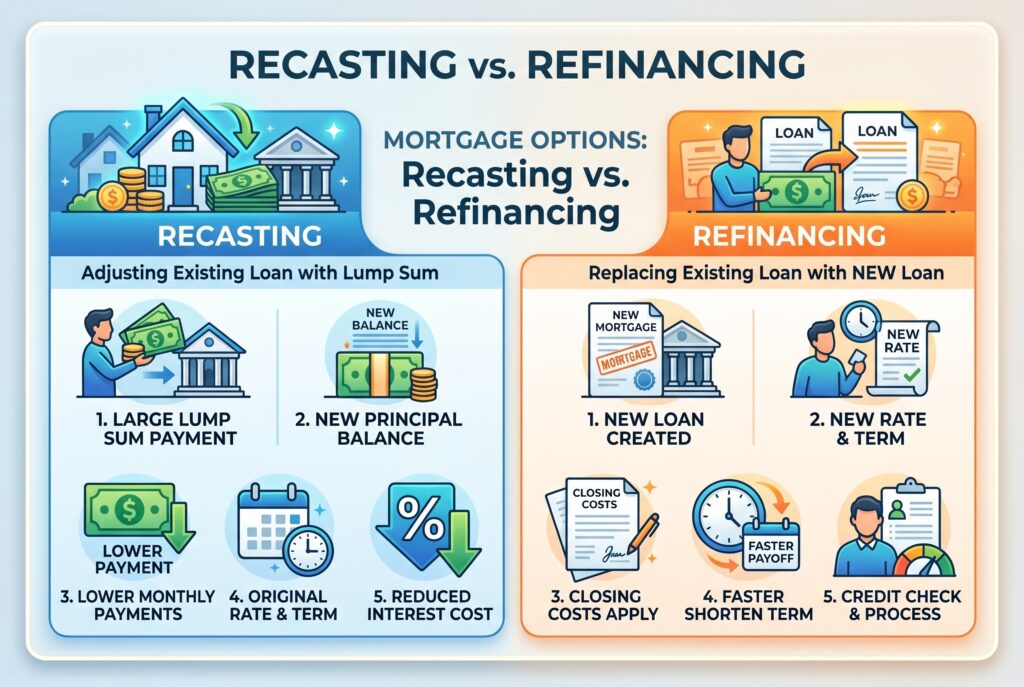

What Is Recasting a Mortgage?

A recast mortgage happens when you make a large lump sum payment toward the principal balance of your loan, and then the lender recalculates the remaining monthly payments over the original term. In other words, the bank will reamortize the balance after your payment goes through. The payoff date stays the same. The interest rate stays the same. But the required monthly payment becomes lower because you now owe less principal.

This is where the term principal curtailment comes in. Principal curtailment simply means making a direct reduction to the outstanding loan balance. But a principal payment by itself doesn’t automatically lower the required payment. The lower payment comes when the lender formally processes the recast and updates the amortization schedule.

That distinction matters. A lot of homeowners think that if they throw extra money at the mortgage, the monthly bill will drop on its own. Usually, it won’t. If you want the legal required payment to fall, the loan generally has to be formally recast.

Interactive Tool: The Mortgage Recast Calculator

Recast Calculator

Find out your new monthly payment and interest savings after recasting your mortgage.

Your Recast Results

A mortgage recast calculator is one of the most useful tools in this decision process because it turns a vague idea into real numbers. Instead of wondering whether a lump sum would help, you can estimate the likely monthly payment after the recast.

A recast mortgage calculator usually needs four main inputs. First, your current balance. Second, your interest rate. Third, your remaining term, usually in months. Fourth, the lump sum payment you’re planning to apply. Once you enter those numbers, a recast calculator can estimate the new payment and help you see whether the reduction is worth using that much cash.

This part is important because the outcome can vary more than people expect. A modest lump sum may reduce the payment, but not dramatically. A larger lump sum can make a substantial difference. That’s why the calculator stage matters so much. It helps you move from curiosity to decision making.

It also helps you compare options. If your payment only drops a little, you may decide to keep more liquidity instead. If the reduction is meaningful, the mortgage recast calculator may confirm that recasting is a strong move for your budget.

How a Mortgage Recast Works: A Step by Step Example

Imagine you have a mortgage balance of $300,000 with 20 years left and a fixed rate you don’t want to lose. Then imagine you receive a $50,000 bonus, inheritance, or home sale payout. If you apply that money as a lump sum to principal and ask your lender to recast the loan, the remaining balance might fall to $250,000 before the bank recalculates the payment.

At that point, the lender reamortizes the remaining balance across the original time left on the loan. The result is a smaller required monthly payment, even though the interest rate and maturity date remain unchanged. That’s what makes a recast so appealing. You aren’t restructuring the entire loan from scratch. You’re simply telling the lender to update the monthly math after a large principal curtailment. For homeowners, that can feel like the best of both worlds. You lower the payment while keeping the valuable financing terms you already have.

Recasting vs. Refinancing: Which Strategy Wins in 2026?

This is the question most borrowers eventually ask. Should you recast or refinance? Refinancing replaces your current mortgage with a brand new one. That means new underwriting, a new interest rate, and closing costs that can run much higher than a simple recast fee. If current rates are above the rate already attached to your mortgage, refinancing may lower payment pressure in one way while damaging the loan in another. You solve the monthly issue, but you give up the cheaper rate you already have.

Recasting mortgage strategies work differently. You keep the original loan, the original term, and the original rate. In many cases, that’s exactly what makes recasting so attractive. The administrative fee is usually much smaller than a refinance, and the process is often lighter.

So which one wins? If you already have a great rate and a lump sum available, recasting often makes more sense. If your current rate is high enough that a new lower rate would still save you money after fees, refinancing may be worth considering. But for homeowners protecting an older low-rate mortgage, a recast often has the stronger logic.

Eligibility and Requirements: Is Your Loan Recastable?

Not every loan can be recast, so this is where many people need a reality check.

A conventional loan recast is usually the most common scenario. Many conventional loans are eligible, especially those connected to standard conforming structures. Government-backed mortgages are a different story. FHA and VA loans generally don’t offer the same recast flexibility, and USDA loans are often treated similarly.

Lenders also usually require a minimum lump sum payment before they’ll process the request. In many cases, that threshold is at least $5,000, though some lenders may want more. There is also usually a fee, often in the range of a few hundred dollars.

This is why your next step should always be contacting the current servicer directly. Ask three things clearly. Does your loan allow recasting? What is the minimum payment required? What fee applies? The answer can vary by lender, and that variation is one reason the mortgage recast process feels simple in theory but more specific in real life.

Pros and Cons of Recasting Your Mortgage

A mortgage recast has clear benefits, but it also comes with tradeoffs. The biggest advantage is lower monthly payments. That’s the headline reason people do it. Another major benefit is keeping the low interest rate already attached to the loan. Recasting can also reduce total interest paid over the life of the mortgage because the principal falls earlier.

But the downsides matter too. First, it requires significant cash. Once that money is pushed into the mortgage, it isn’t easily available again. Second, the loan term doesn’t shorten. If your goal is becoming debt-free faster, extra principal payments without recasting may fit better. Third, recasting doesn’t improve the interest rate itself. If your existing rate is already weak and current market conditions happen to favor refinancing, a recast may not be the best answer.

That’s why the smartest decision usually depends on priorities. Do you want lower monthly overhead, or do you want maximum liquidity and faster payoff?

Conclusion

If you have a lump sum available and you want to lower your monthly payment without giving up a valuable old rate, recasting mortgage options deserve serious attention. A recast mortgage keeps the structure you already like and changes the part you want to improve most: the required monthly payment.

The best next step is practical, not theoretical. Run the numbers with a mortgage recast calculator one more time. Compare that result against your other options, including holding cash, investing it, or making simple extra principal payments instead. Then call your servicer and ask whether your current loan qualifies for a recast loan. That’s how you turn a useful idea into a real mortgage strategy.