If you’ve opened your banking app and noticed two different numbers, you aren’t imagining things. The gap between current balance vs available balance confuses a lot of people, especially when money looks like it’s there but can’t actually be spent yet. That’s also how overdraft fees happen. A person checks one number, assumes everything is fine, makes a purchase, and suddenly gets hit with a charge they didn’t expect.

The good news is that this difference isn’t random. Once you understand how account balance mechanics work, the two numbers make a lot more sense. More importantly, you can use that knowledge to avoid unnecessary fees and make safer decisions with your money.

Definition: Current Balance and Available Balance

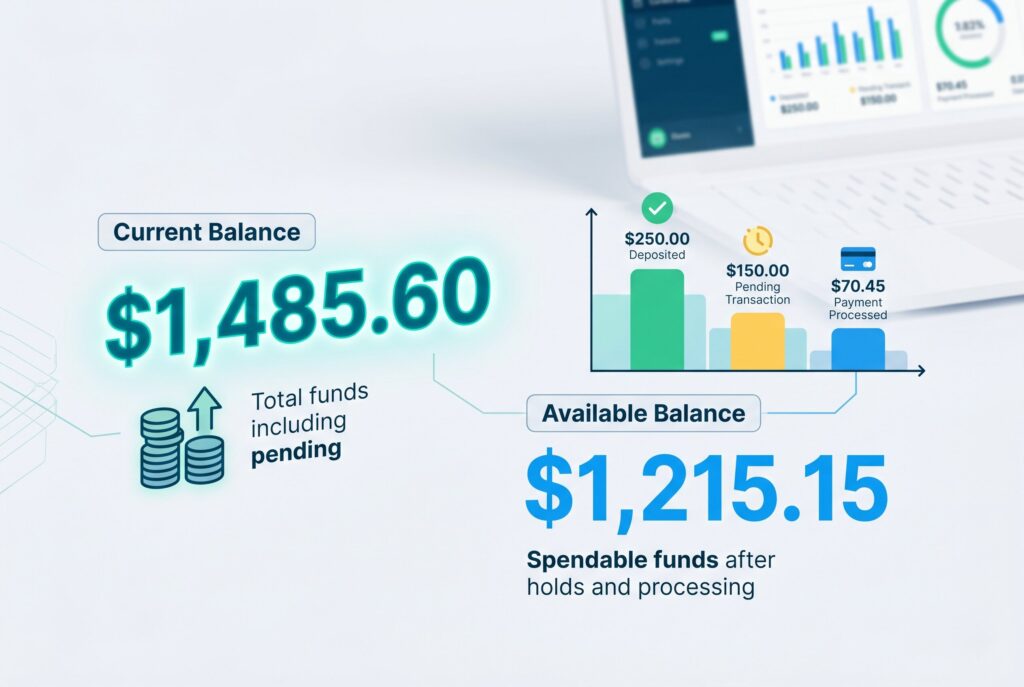

The easiest way to understand current balance vs available is to think of one number as the fuller record and the other as the safe-to-spend number. Current balance is the total amount in your account at that moment, including transactions that may still be in the process of settling. In everyday banking language, it often reflects the overall account balance you see when the bank totals what has been posted and what may still be moving through the system.

Available balance is the amount you can actually use right now without running into trouble. It takes pending transactions, temporary holds, and certain processing delays into account. In practical terms, this is usually the more important number when you’re deciding whether to swipe a debit card, withdraw cash, or schedule a payment. That’s why the difference matters so much. Current balance may show what exists in the account overall, but available balance shows what is truly spendable at this moment.

Why Do Current and Available Balances Sometimes Show Different Amounts?

This is the real question most people are trying to solve. Why do current and available balances sometimes show different amounts? The short answer is pending transactions. When a payment is started but not fully completed, your bank may reduce the available balance before the current balance fully catches up. This is especially common with debit card purchases, deposits, and checks.

Debit Card Holds

Some merchants place an authorization hold before the final amount settles. Gas stations, hotels, and restaurants are classic examples. A gas station may temporarily hold more than the amount of fuel you actually pumped. A restaurant may hold the pre-tip total before the final charge updates. A hotel may place a larger hold for incidentals. During that window, your available balance can drop even though your current balance may still look higher.

Check Holds

Checks are another common reason the numbers don’t match. If you deposit a check, some or all of the money may be on hold before it becomes fully available. Regulation CC governs part of this process, but the practical result for consumers is simple: money can appear in your account activity before it is fully available to spend.

Pending Deposits

Pending deposits can also create confusion. A payroll deposit, transfer, or mobile deposit may show up in your account activity before the bank releases the full amount into your available balance. That’s why a deposit can feel “there” without being ready yet. In other words, available balance reacts to risk and timing. Current balance reflects the broader account picture. The mismatch is the bank’s way of showing that a transaction has started, but hasn’t fully finished.

What Does Ledger Balance Mean? Is It the Same as Current Balance?

Ledger balance is a more technical banking term, but it’s useful to know because some banks still display it. Ledger balance meaning usually refers to the balance in your account at the close of the previous business day. It doesn’t always reflect the newest pending activity the same way your live app screen does. That’s why ledger balance vs available balance can be even more confusing than current balance vs available balance.

In many situations, ledger balance is close to a prior-day snapshot, while current balance is a more updated total, and available balance is the safe-to-spend amount right now. Different banks label these categories differently, which is part of the confusion. But the core idea stays the same: available balance is usually the most practical number for real-time spending decisions.

The Best Way to Avoid Overdraft Fees

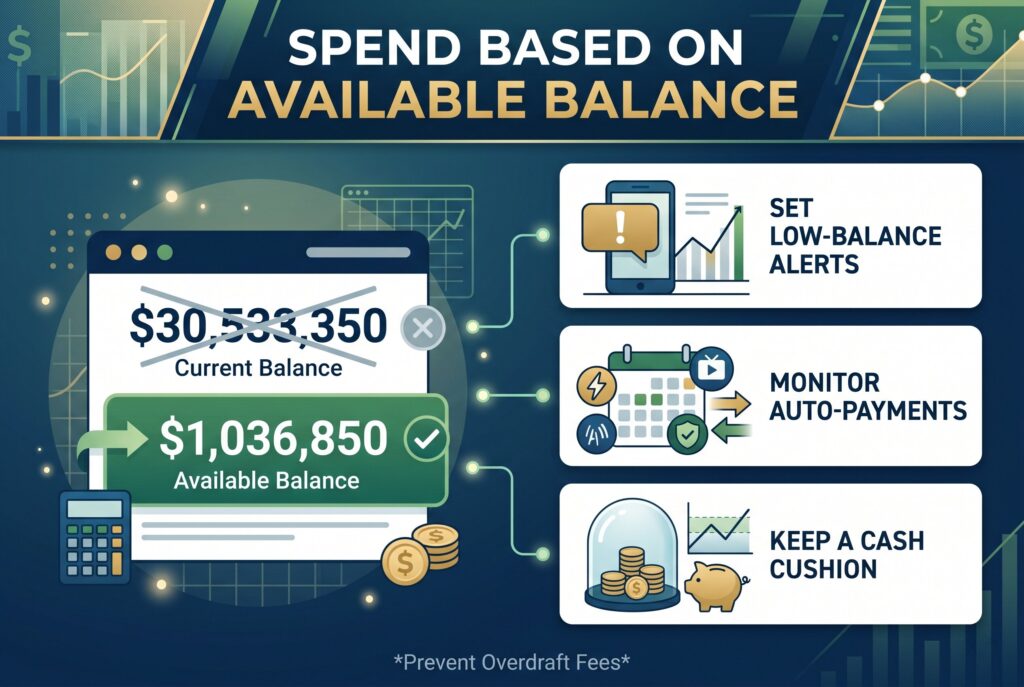

If you only remember one rule from this article, make it this one: spend based on your available balance, not your current balance. That one habit can prevent a lot of overdraft fees.

Overdraft fees happen when money leaves the account after pending or held activity has already reduced what was actually available. A person sees the larger number, assumes it’s usable, and then a check clears or a merchant hold settles. Suddenly the account goes negative, and the fee appears.

A few habits can make this much less likely:

- Set low-balance alerts in your bank app. Most banks let you choose a threshold so you get notified before things get tight. Watch automatic payments carefully.

- Subscriptions, utility bills, insurance drafts, and loan autopays can hit the account while other transactions are still pending.

- Keep a cushion if possible. Even a small extra buffer can protect you from timing issues, especially if you use a debit card often.

- Trust the available balance first. It isn’t always the prettier number, but it’s usually the safer one.

On Credit Cards: Statement Balance vs Current Balance

This balance confusion doesn’t stop with bank accounts. People also ask what current balance means on a credit card, and that’s a separate but related issue. On a credit card, current balance usually means what you owe right now, including recent charges that have been posted since your last statement closed. Statement balance vs current balance is the comparison that matters here. Your statement balance is the amount listed on your last billing statement. That is usually the amount you need to pay by the due date to avoid interest if you aren’t carrying a balance. Your current balance may be higher because it includes newer purchases that haven’t reached the next statement yet. So for checking accounts, the key distinction is current balance vs available balance. For credit cards, the more important comparison is statement balance vs current balance. They sound similar, but they solve different problems.

Conclusion

The difference between current balance vs available balance comes down to timing. One number reflects the broader account total, while the other reflects what you can safely use right now. Once you understand how pending transactions, holds, and deposit timing affect your account balance, the two numbers stop feeling contradictory.

That’s also the key to avoiding overdraft fees. Use your available balance as your spending guide, set alerts, and don’t assume every dollar that appears in the app is ready to use immediately. When you treat available balance as the real decision-making number, banking gets a lot less stressful.