A lot of savers hesitate before opening a money market account for one simple reason: they’re afraid their cash will get trapped. That fear is understandable, but it’s usually based on confusion between a money market account and a certificate of deposit. A money market account calculator helps solve the practical side of the question right away by showing how much your balance could grow over time, while the account itself remains flexible rather than locked. If you’ve been looking for a money market calculator because you want higher yield without giving up access, this guide will help you understand both the numbers and the fine print.

Interactive Tool: The Money Market Calculator

Based on monthly compounding. Results are projections and not guaranteed.

The most useful place to start is with the calculator itself. A strong money market account calculator should let you enter four basic inputs:

- Initial Deposit

- APY

- Monthly Contribution

- Time Period

That’s enough to create a realistic growth estimate for many savers. For example, if you deposit $12,000 into an account earning 4.25% APY, contribute $200 each month, and keep the money there for 24 months, the calculator can show not just the ending balance but the share of growth created by interest rather than contributions. This is why calculator-first content performs so well for savers. It turns the decision from a vague “should I open one?” question into a clear “what could this actually earn for me?” exercise.

The best way to use a money market calculator isn’t just once. It’s to test multiple scenarios. Try one set of inputs with no monthly contribution. Then try another with regular deposits. Then lower the APY slightly to see how sensitive the results are to rate changes. That approach gives you a more realistic picture of how your money market account may perform in the real world rather than under one perfect assumption.

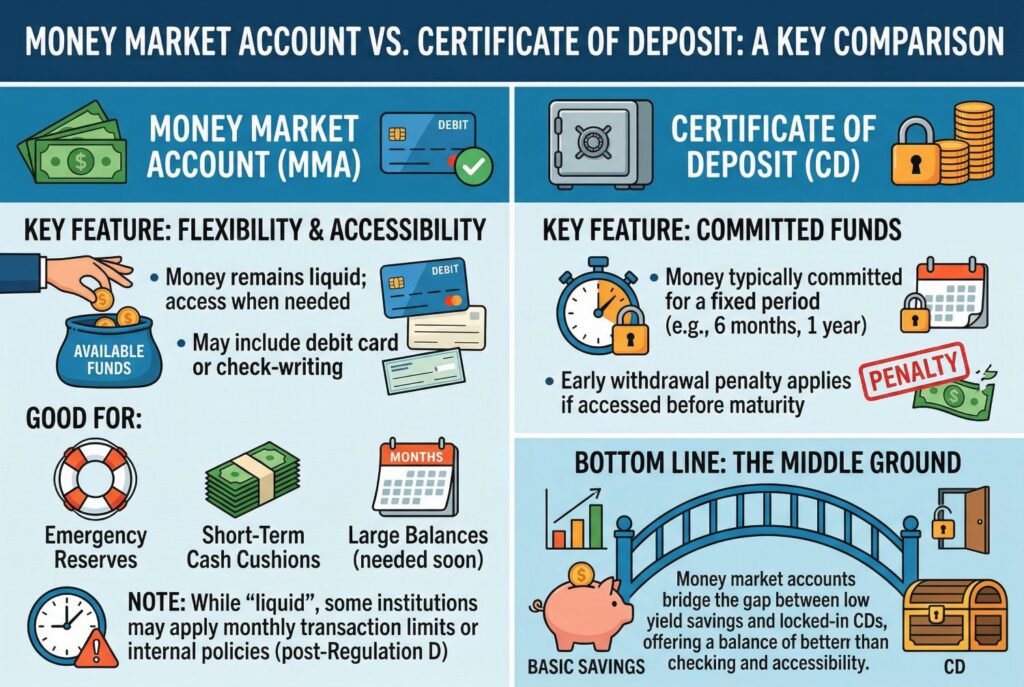

The Big Myth: Is Money Market Account Money Stuck for a Set Time?

This is one of the biggest misunderstandings in the category, and it needs a direct answer: no, money market account money stuck for a set time isn’t how these accounts work.

A money market account isn’t the same thing as a CD. With a CD, your money is typically committed for a fixed period unless you’re willing to accept an early withdrawal penalty. A money market account doesn’t work like that. The money remains liquid, which means you can usually access it whenever you need it. Some accounts even come with debit card access or check-writing privileges, which makes them more flexible than a basic savings account in everyday use.

That’s why a money market account can be useful for people who want a middle ground. You’re not locking the cash away for six months or a year, but you’re also not leaving it in a low-yield checking account earning almost nothing. For emergency reserves, short-term cash cushions, or large balances you may need within months rather than years, that flexibility is a major advantage.

Still, “liquid” doesn’t mean “limitless.” Some institutions may continue applying monthly transaction limits or internal withdrawal policies even though the old federal six-transaction cap from Regulation D is no longer mandatory in the same way. So your money isn’t locked, but it also isn’t always designed for constant everyday spending.

Liquidity Check: Money Market vs Savings vs CDs

The smartest way to understand the product is to compare it directly with two common alternatives. That’s where a simple comparison table helps:

|

Account Type |

Typical APY | Liquidity | Early Withdrawal Penalty |

|---|---|---|---|

| Money Market Account | Competitive, often variable | High | Usually no formal early withdrawal penalty |

| Savings Account / High-Yield Savings | Competitive, often variable | High | Usually no formal early withdrawal penalty |

| CD | Often fixed for a term | Low to medium | Yes, in most cases |

This is where the money market vs savings comparison becomes useful. A standard savings account, especially a high-yield savings account, is usually simpler and better for pure saving discipline. A money market account often becomes more attractive when you want similar yield potential but prefer additional access features. That’s also why many savers now compare money market accounts vs high yield rather than thinking of savings accounts in the old, low-rate traditional-bank sense.

The key question isn’t only “which one pays more?” It’s “which one fits how I’ll use the money?” If you want stronger separation from spending, a high-yield savings account may be the better behavioral choice. If you want easier access in a real emergency, a money market account may feel more practical.

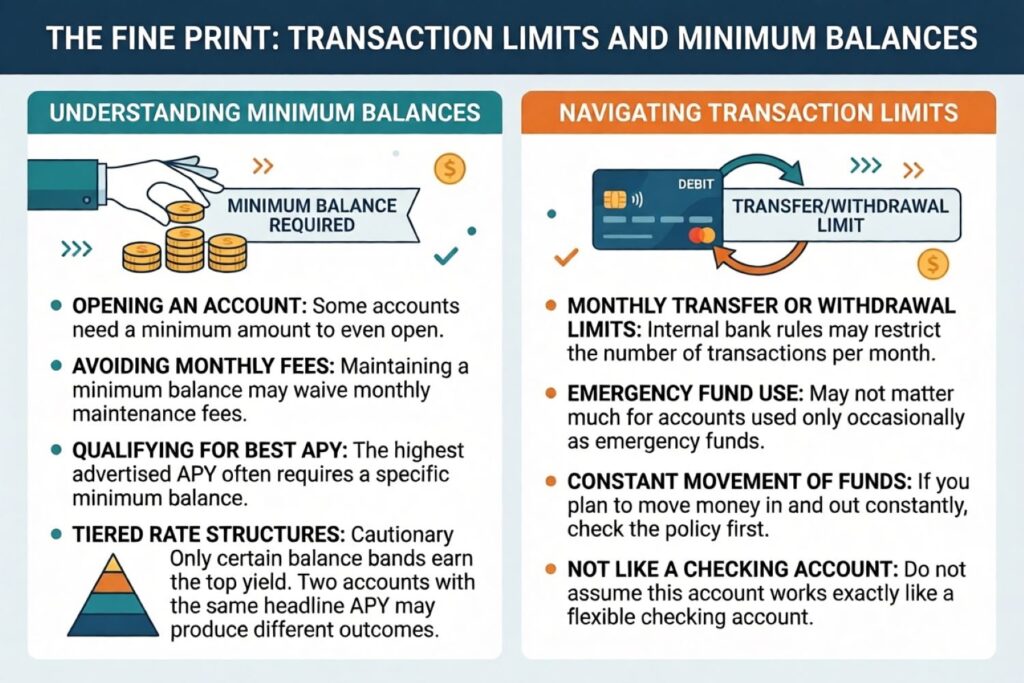

The Fine Print: Transaction Limits and Minimum Balances

This is where many comparison articles stay too shallow. Yield matters, but terms matter too. Some money market accounts require higher minimum balances to open the account, avoid monthly maintenance fees, or qualify for the best advertised APY. Others may use tiered rate structures, where only certain balance bands receive the highest yield. That means two accounts with the same headline APY may produce very different real outcomes depending on your balance.

Transaction rules matter too. Many banks still preserve internal monthly transfer or withdrawal limits even though the older regulatory rule changed. If you’re using the account as a true emergency fund, that may not matter much. But if you plan to move money in and out constantly, you need to check the policy before assuming the account works like a checking account.

What is Interest Saving Balance?

Another phrase that creates confusion is interest saving balance. So what is interest saving balance? In practice, it usually refers to the required average daily balance or minimum balance needed to earn interest at the advertised level or avoid certain fees. Different institutions phrase it differently, but the idea is the same: your actual return may depend on maintaining a qualifying balance over time.

That’s why understanding what interest saving balance matters so much. If your account requires a certain threshold to unlock the best rate or waive the maintenance fee, your real earnings may be lower than the calculator suggests unless you model the balance correctly.

How to Use the Money Market Calculator for Your Emergency Fund

A money market account is often most useful when tied to a real savings purpose. Emergency funds are one of the clearest examples.

Let’s say your target emergency fund is $15,000. You already have $8,000 saved, you can add $300 per month, and the account APY is 4.10%. Plug those numbers into the money market account calculator with different time periods. You’ll be able to estimate how long it takes to reach your target and how much interest helps along the way.

This is more valuable than just asking whether the rate “sounds good.” It lets you plan your reserve with actual numbers. You can also run a second scenario that assumes a slightly lower APY, which is smart because deposit rates aren’t fixed forever. A rate that looks attractive today may not stay there for the entire year.

If you’re using the money market calculator for an emergency fund, focus on accessibility first and yield second. The point of an emergency fund isn’t maximum return. It’s reliable access plus reasonable growth.

Conclusion

The biggest takeaway is simple: you can use a money market account to grow cash without locking it away for a fixed term. That’s why the money market account calculator is so useful. It helps you see the earning potential clearly, while the account itself keeps your funds liquid enough for real-life needs.

If you’re still deciding, go back to the calculator and test a few different scenarios with your own deposit amount, APY, contribution schedule, and time frame. Once you see how the numbers change, the product becomes much easier to evaluate. The best cash strategy usually isn’t just about chasing the highest rate. It’s about finding a balance between growth, access, and peace of mind.