When people ask what is a quitclaim deed, the simplest answer is this: it’s a fast legal document that transfers whatever ownership interest one person has in a property to someone else. The person giving up the interest is the grantor. The person receiving it’s the grantee. A quitclaim deed is quick, simple, and common in family transfers, divorce settlements, trust funding, and title cleanup. But it comes with one major warning. It gives no warranty. That means the grantor does not promise clear title, does not guarantee there are no liens, and does not even guarantee that they truly own the property.

The Reality Check: Quitclaim vs. Warranty Deed

A quitclaim deed and a warranty deed both transfer real estate ownership, but they don’t offer the same protection.

A Warranty Deed

A warranty deed is used in most normal home sales. It promises that the seller owns the property, has the legal right to transfer it, and is giving the buyer clear title. This is why title insurance and standard closing procedures usually support a warranty deed.

A Quitclaim Deed

A quitclaim deed is different. It transfers only the interest the grantor may have. If the grantor owns 100 percent, the grantee may receive 100 percent. If the grantor owns nothing, the grantee receives nothing. That is the core risk behind many repercussions of a quitclaim deed.

This is why a quitclaim deed should usually be used only between people who trust each other, such as spouses, parents and children, siblings, or a person transferring property into their own trust.

The Mortgage Trap: Why Banks Care

The biggest misunderstanding is that changing the deed changes the mortgage. It doesn’t. A deed controls ownership. A mortgage controls debt. If you sign a quitclaim deed giving your interest in the house to someone else, your name may disappear from the title, but you may still owe the bank if your name remains on the loan.

This becomes dangerous in divorce, family buyouts, and informal transfers. If your ex spouse misses payments after you quitclaim the house to them, the lender can still report late payments on your credit if you are still on the mortgage.

There is also a due on sale clause risk. Many mortgage agreements allow the lender to demand full repayment if property ownership changes without approval. A quitclaim deed can trigger that concern. The safest solution is often to combine the deed transfer with a refinance, so the person keeping the home also becomes the only person responsible for the mortgage.

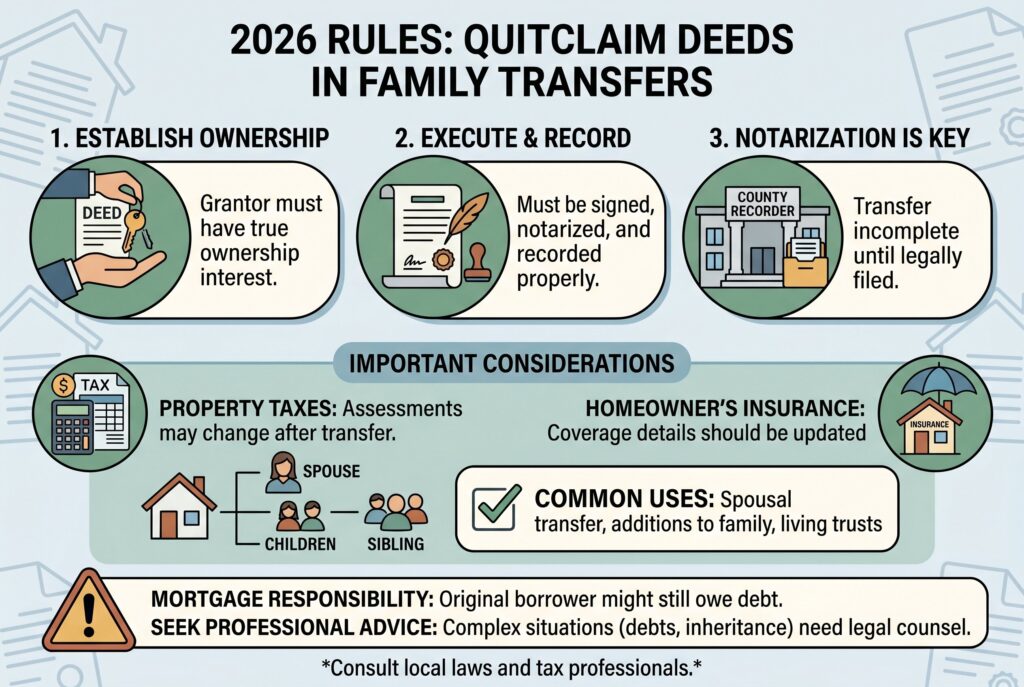

2026 Rules for Using a Quitclaim Deed in Family Transfers

Family transfers remain one of the most common uses of a quitclaim deed, but certain rules should be followed to avoid legal and financial problems. First, the grantor must actually have an ownership interest in the property to transfer. Second, the deed must be properly signed, notarized, and recorded according to state requirements. Simply signing a quitclaim deed doesn’t automatically complete the transfer.

Property owners should also remember that transferring ownership doesn’t remove an existing mortgage. If a loan is still attached to the property, the original borrower may remain responsible for the debt unless the lender approves a refinance or assumption. In some cases, transferring property can also affect property tax assessments, homeowner’s insurance coverage, or eligibility for certain tax benefits.

For most family transfers involving spouses, parents, children, siblings, or living trusts, a quitclaim deed can be a simple and effective solution. However, when the property has multiple owners, outstanding debts, or potential inheritance issues, professional legal or tax advice may be worth considering before the transfer is completed.

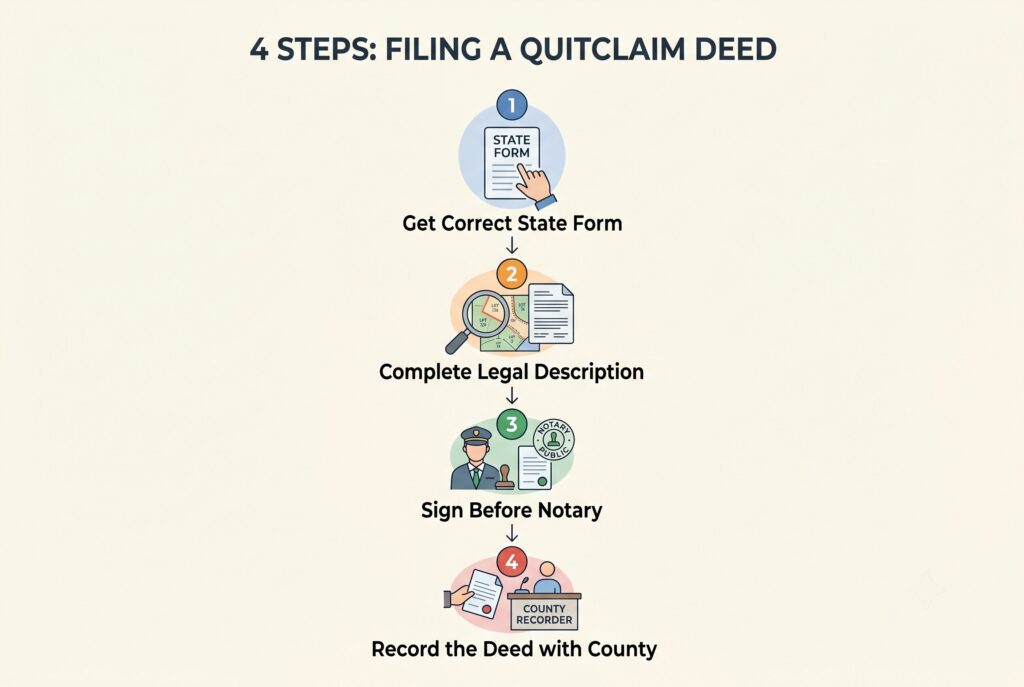

Execution: How to File a Quitclaim Deed Form in 4 Steps

Step 1: Get the Correct State Form

A quitclaim deed form must match local rules. Each state and county may have different formatting requirements, margin rules, witness rules, transfer tax forms, or legal description standards. Do not rely on a random online template unless you know it meets local recording requirements.

Step 2: Complete the Legal Description

The property address alone isn’t enough. A deed usually needs the full legal description from the prior deed, survey, or county records. This may include lot numbers, subdivision names, metes and bounds, or parcel descriptions. Copy this section carefully. Errors in the legal description can prevent the transfer from working correctly.

Step 3: Sign Before a Notary

Most quitclaim deeds must be signed by the grantor in front of a notary public. Some states also require witnesses. If the signature process is wrong, the county may reject the deed, or the transfer may be challenged later. The grantee often doesn’t sign, but local rules vary.

Step 4: Record the Deed with the County

A signed deed isn’t enough if it sits in a drawer. To make the transfer part of the public record, file the original with the County Recorder, Register of Deeds, or Clerk office where the property is located. Recording fees often range from about $20 to $50, though some counties charge more or require additional transfer tax paperwork.

When You Should Not Use a Quitclaim Deed

Before signing a quitclaim deed, it is important to understand situations where this type of transfer may create significant legal or financial risks.

- Don’t use a quitclaim deed to purchase property from someone you do not fully trust. Because the deed provides no guarantee of ownership, you could unknowingly receive property that is subject to liens, unpaid property taxes, ownership disputes, judgments, easements, or other title defects. If a problem arises later, you generally have little legal recourse against the grantor because no ownership warranties were provided.

- Don’t assume a quitclaim deed removes you from mortgage liability. Transferring ownership through a quitclaim deed does not automatically remove a borrower from an existing mortgage loan. Unless the lender formally approves a loan assumption, release of liability, or refinancing arrangement, the original borrower may remain legally responsible for making mortgage payments even after giving up ownership rights.

- Don’t use a quitclaim deed when title insurance protection is important without consulting the title company first. Some title insurers may have specific requirements regarding ownership transfers completed through quitclaim deeds. Using the wrong type of deed could complicate future title insurance coverage, refinancing, or resale transactions. Always verify how the transfer may affect insurability before proceeding.

- Don’t use a quitclaim deed as a substitute for professional estate planning in complex situations. While quitclaim deeds can be useful for simple family transfers, they may create unintended consequences when blended families, multiple heirs, outstanding debts, creditor claims, Medicaid planning concerns, or significant tax issues are involved. In these circumstances, consulting an estate planning attorney can help ensure the transfer aligns with your long-term legal and financial goals.

Conclusion

A quitclaim deed is a fast and simple way to transfer property ownership. It is often used for family transfers, trusts, divorce settlements, title corrections, and LLC transfers. However, it doesn’t guarantee clear title or remove mortgage obligations. It only transfers ownership rights and can create tax, insurance, or lender issues if used without proper planning.

Use it only when the relationship is trusted, the title situation is clear, the mortgage consequences are understood, and the deed is recorded correctly. In the right situation, it’s a practical tool. In the wrong situation, it can create years of legal and financial trouble.

Related Articles

Quit Claim Deed Loopholes & Repercussions: Protect Your Assets