An auto and renters insurance bundle is a simple way to buy two important policies from the same insurance company and unlock a multi-policy discount. Think of it like buying in bulk at the grocery store. Instead of paying separate prices for separate items, you combine your car insurance and renters insurance under one provider so the insurer rewards you with a lower overall cost.

How much can you save? In many cases, a multi-policy discount can reduce your total insurance cost by around 10% to 25%, depending on your location, driving record, coverage limits, claim history, and the company you choose. It isn’t always a guaranteed number, but it’s often meaningful enough to make bundling worth comparing.

The other big benefit of a car and renters insurance bundle is convenience. With a bundled policy, you may be able to manage your bills, claims, documents, renewals, and coverage changes in one place. That matters when life is busy, when you’re moving into a new apartment, or when you simply don’t want to juggle two companies every time something changes.

How It Works: The Laptop in the Car Scenario

A lot of people hear the phrase car and renters insurance and assume the two policies overlap. In reality, they protect different parts of your life. Car insurance mainly protects your vehicle, your liability on the road, and certain accident related costs. Renters insurance protects your personal belongings, your liability as a tenant, and sometimes temporary living expenses if your rental becomes unlivable after a covered event. Here’s the easiest way to understand why a renters and car insurance bundle can be valuable. Imagine you park your car outside your apartment building and leave your laptop in the back seat. Someone breaks the window and steals it. Your auto insurance may help with the broken window if you have the right coverage, but it usually won’t pay to replace the laptop itself. That laptop is personal property, so it typically falls under renters insurance.

This is where bundling becomes more than a discount. It helps close everyday coverage gaps. You’re not just buying two random policies. You’re creating a protection system around the way you actually live. Your car gets covered on the road, and your belongings stay protected whether they’re in your apartment, your car, or sometimes even with you while traveling. For renters, this matters because personal belongings add up fast. A phone, laptop, headphones, clothes, camera, furniture, kitchen gear, and sports equipment can easily represent thousands of dollars. Without renters insurance, replacing those items after theft, fire, smoke damage, or certain water damage events could come directly out of your pocket. With a bundle, you may get that protection while also lowering the total price of your insurance.

Navigating Life Events: Moving In Together

Insurance often becomes important during life changes, not just during emergencies. Moving into a new apartment, getting your first car, sharing rent with a partner, or combining finances with someone can all create questions you may not have thought about before.

In 2026, long-term renting is common for young professionals, couples, and roommates, making renters insurance more important than ever. A common question is whether you need to be married to bundle insurance. In most cases, no. Depending on the insurer, state rules, and household setup, unmarried couples may be able to combine or coordinate renters and auto insurance coverage. Roommates may also have options, although shared renters policies can be more complicated. The most important step is accurately reporting who lives in the home, who drives each vehicle, and who owns the insured property.

Before combining anything, decide who will be the primary policyholder, how bills will be paid, and what happens if one person moves out. This part isn’t romantic, but it’s practical. If you break up, change roommates, or move into separate apartments, you’ll need to update the policy quickly so both people remain properly protected. Insurance should match real life, not last year’s living situation.

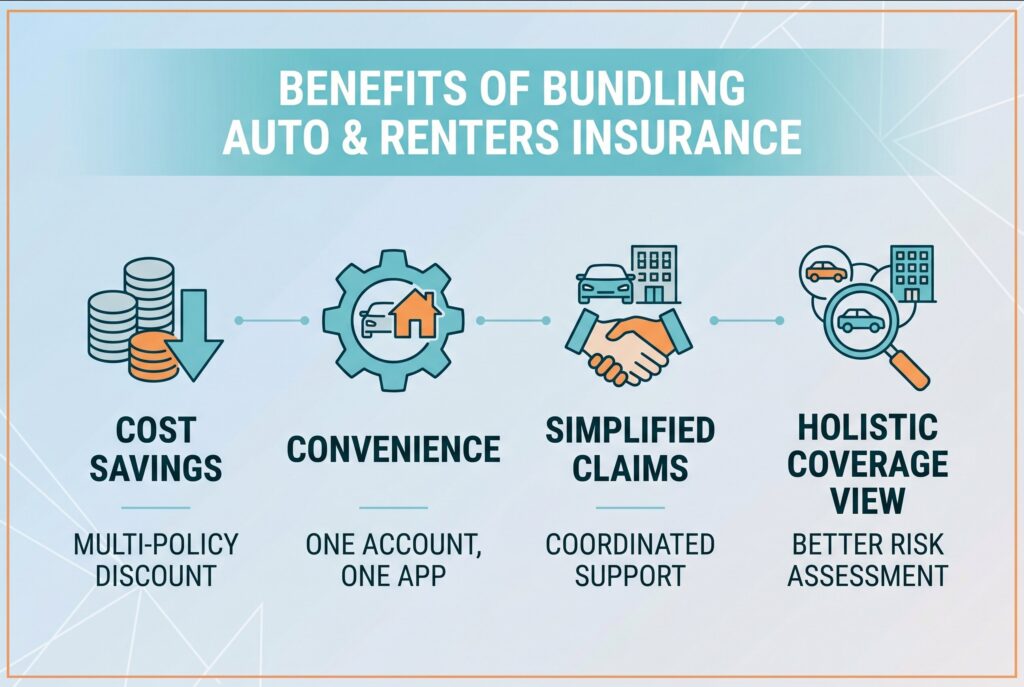

Why an Auto and Renters Insurance Bundle Can Be Worth It

Save Money With a Multi-Policy Discount

The biggest reason people search for an auto and renters insurance bundle is savings. When an insurer manages multiple policies for the same customer, it may reduce administrative and servicing costs, allowing it to offer a multi-policy discount.

Simplify Insurance Management

Bundling can make insurance easier to manage. One account, one app, one renewal schedule, and one customer service team can reduce the hassle of keeping track of multiple policies.

Make Claims Easier to Navigate

If an incident affects both your vehicle and personal belongings, having coverage with the same insurer may make the claims process easier to understand and coordinate, even when separate deductibles and coverage rules still apply.

Get a More Complete View of Your Coverage

Bundling encourages you to look beyond the cheapest individual policy and evaluate your overall protection. This approach can help ensure your coverage aligns with your actual risks and reduces the chance of being underinsured.

How to Bundle Renters and Auto Insurance and Save 15% or More

To maximize savings, compare standalone and bundled quotes using the same coverage levels. While bundle discounts alone may not always reach 15%, combining them with safe-driver, autopay, paperless billing, or telematics discounts often can. Just make sure the lower premium isn’t coming from reduced coverage. The best bundle is one that cuts costs while maintaining the protection you actually need.

Here is a simple process to follow:

- List your current annual auto insurance cost and renters insurance cost.

- Request standalone quotes and bundled quotes from at least three insurers.

- Ask each insurer for the exact multi-policy discount percentage.

- Compare quotes using the same coverage limits and deductibles.

- Add other eligible discounts such as autopay, paperless billing, safe driver, or telematics.

- Choose the option that saves at least 15% while keeping the coverage you actually need.

For example, if you currently pay $1,600 per year for auto insurance and $220 per year for renters insurance, your total annual cost is $1,820. A 15% savings would reduce that total by about $273 per year. If a bundled quote brings your annual cost down to around $1,547 or less with similar coverage, then the bundle meets the 15% savings target. The goal is to find the best total value. A strong auto and renters insurance bundle should lower your combined cost, keep your coverage limits strong, and make it easier to manage both policies in one place.

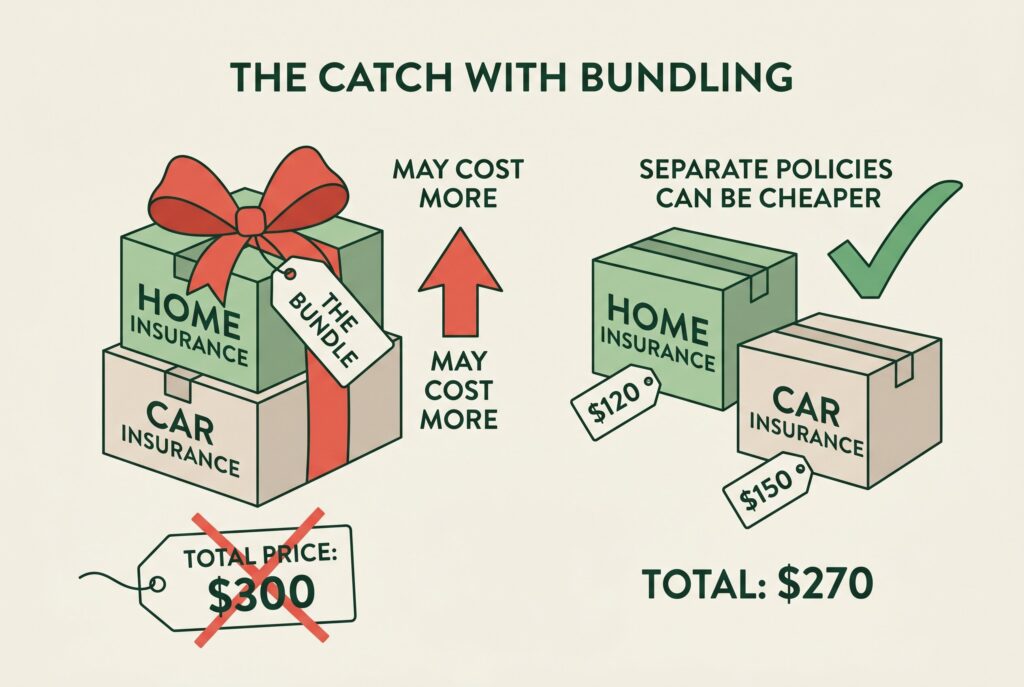

The Catch: When Bundling Actually Costs You More

A Bundle May Not Always Be the Cheapest Option

Bundling can be a smart way to save money, but it shouldn’t be automatic. The best insurance choice is the one that delivers the right coverage and overall value, not simply the largest advertised discount.

Drivers With Higher Risk Profiles May Benefit From Separate Policies

If you have accidents, traffic violations, or other risk factors on your record, a specialized auto insurer may offer significantly lower standalone car insurance rates than a bundled package. In some cases, separate policies can be more affordable overall.

Review Coverage Limits, Not Just the Monthly Premium

A lower price does not always mean better value. Before choosing a bundle, compare personal property coverage, liability limits, deductibles, replacement cost options, exclusions, and claim conditions. Understanding policy exclusions is especially important because they determine what is not covered.

Re-Shop and Reevaluate Your Bundle Every Year

Insurance needs and pricing change over time. An insurance bundle that worked well when you first rented an apartment may no longer be the best option after a move, a new vehicle purchase, a marriage, a roommate change, or improvements to your driving and credit history. Regular comparisons can help ensure you’re still getting the best value.

How to Compare Bundled vs Separate Insurance

Start with your current annual cost for both policies. Add your car insurance premium and renters insurance premium together. Then request a bundled quote with the same or better coverage limits. Make sure you compare equal deductibles, equal liability limits, and similar personal property protection. A bundle only saves money if the coverage comparison is fair.

Next, look at the real experience. Can you manage everything online? Is customer support easy to reach? Are claims reviews clear? Does the company explain policy exclusions in plain language? Price matters, but service matters when something goes wrong. Finally, think about your next twelve months. Are you moving in with a partner? Buying a car? Getting married? Changing apartments? Working from home with expensive equipment? These life details can affect the right setup. The best bundle isn’t just cheaper. It fits the way you live now.

Conclusion

An auto and renters insurance bundle can be a smart move for renters who want lower costs, simpler management, and stronger everyday protection. In many cases, choosing to bundle renters and auto insurance helps policyholders save money while keeping their coverage under one provider. It’s especially useful if you own a car, rent an apartment, keep valuable belongings at home, or are moving in with a partner and trying to organize shared finances.

The main thing is to compare carefully. A multi-policy discount can be attractive, but it shouldn’t distract you from coverage limits, deductibles, exclusions, and standalone rates. When the numbers and protection both make sense, bundling renters and auto insurance can give you a cleaner, more affordable way to protect your home life and your life on the road.