")

You lock your $1,500 mountain bike outside a coffee shop, step inside for ten minutes, and come back to an empty rack. The lock is cut. The bike is gone. Your first thought is probably: “I only have renters insurance for my apartment. Does renters insurance cover theft of bike outside the home?”

Yes, in many cases, renters insurance does cover theft of a bike outside your home. This is usually handled through off-premises coverage, which protects your personal belongings even when they are away from your rental unit. That means your bicycle may be covered if it’s stolen from a bike rack at work, outside a grocery store, near your school, in a storage unit, or on the street.

But the real question isn’t only whether renters insurance bike theft coverage exists. The bigger question is how much money you will actually receive after your deductible, actual cash value, depreciation, policy limits, and bicycle sublimits are applied. For e-bikes, racing bikes, delivery bikes, and expensive road bikes, the answer can become even more complicated.

Does Renters Insurance Cover Stolen Bike Outside Home?

Yes, renters insurance does cover theft of a bike outside your home in many standard policies. This is called off-premises coverage. If your bicycle is stolen from a public bike rack, parking area, workplace, campus, or coffee shop, your renters policy may treat it like any other stolen personal property.

Renters insurance also typically helps cover stolen items such as laptops, phones, bags, clothing, and bicycles, even when they are away from your apartment. However, your payout depends on your personal property coverage, deductible, actual cash value vs replacement cost coverage, and any bicycle sublimits in your policy. High-speed e-bikes, motorized bikes, bikes used for delivery work, and bicycles used for professional racing may not be covered under a standard renters policy. These often need separate bicycle insurance, an e-bike insurance policy, or a scheduled personal property endorsement.

How Off-Premises Coverage Protects Your Bike

Off-premises coverage means your personal property can be protected outside your home. In simple terms, your renters insurance doesn’t only follow your apartment. It follows your belongings. If someone steals your backpack from your car, your laptop from a hotel room, or your bicycle from a locked rack, your renters policy may help pay for the loss. For bike theft renters insurance claims, the location matters less than ownership and policy terms. You usually need to prove the bicycle belonged to you, the theft happened, and the loss is covered. That is why receipts, photos, serial numbers, and a police report are so important.

Still, off-premises coverage can have limits. Some policies reduce coverage for items stolen away from home. Others apply the same personal property limit but still subtract your deductible. Before assuming you are fully protected, check your declarations page and look for terms like personal property coverage, theft coverage, off-premises coverage, deductible, and special limits.

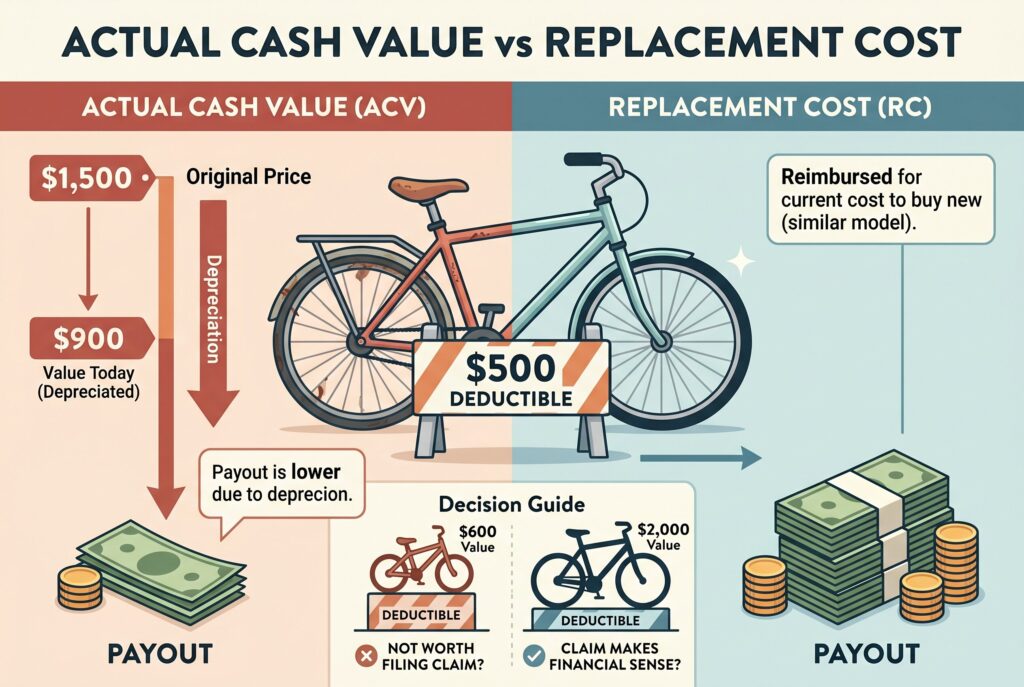

Actual Cash Value vs Replacement Cost: Why Your Payout May Be Smaller

Many renters are surprised when their stolen bike renters insurance claim pays less than expected. The reason is often actual cash value. Actual cash value means the insurer considers depreciation. If you bought a bike for $1,500 three years ago, the company may decide it’s only worth $900 today. If your deductible is $500, your payout may only be $400.

Replacement cost coverage is stronger. It may reimburse you based on the cost to buy a similar new bike, not the depreciated value. If you own a newer or higher-value bicycle, replacement cost coverage can make a major difference. Before filing a bike theft claim, compare the estimated payout with your deductible. If your stolen bike is worth $600 and your deductible is $500, filing a claim may not be worth it. But if your bike is worth $2,000, the claim may make financial sense.

E-Bikes and Professional Racing: The 2026 Exclusions

Renters insurance e-bike coverage is one of the trickiest parts of bicycle theft insurance. A regular human-powered bicycle is usually treated as personal property. An e-bike may not be. Many insurers look closely at whether the e-bike has a motor, throttle, high speed capability, or road-use classification. Some Class 1 e-bikes may be easier to insure under renters insurance, while Class 2 and Class 3 e-bikes can fall into a gray area because they may be treated more like motor vehicles.

If your e-bike is stolen, a standard renters policy may deny the claim if the policy excludes motorized vehicles. This is especially important for high-value electric bikes that cost $2,000, $3,000, or more. In that case, you may need electric bike insurance, a scheduled personal property endorsement, or a specialty bicycle insurance policy. Professional use is another common problem. If you use your bike for delivery work, courier services, bike messenger jobs, or professional racing, standard renters insurance may not cover the theft. Personal renters insurance is designed for personal property used in everyday life, not business equipment or professional sports use.

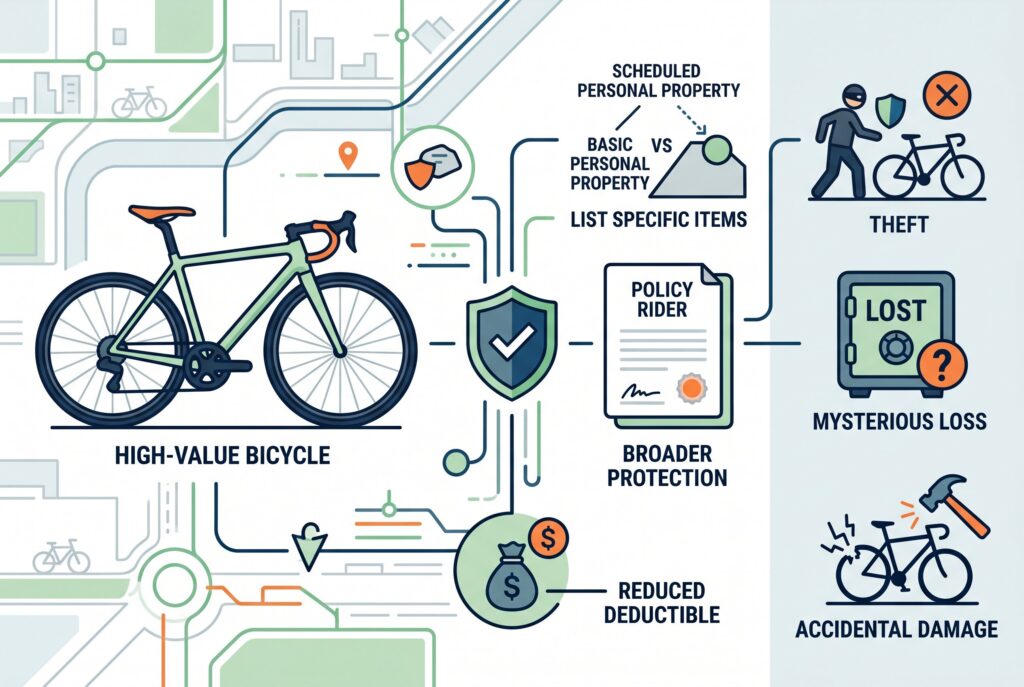

How to Insure a High-Value Bicycle

If your bicycle is expensive, don’t rely blindly on basic renters insurance bicycle theft coverage. Many policies have sublimits for certain categories of property. A sublimit is a smaller limit inside your larger personal property coverage. For example, your renters policy may show $30,000 in personal property coverage, but that doesn’t always mean your $4,000 road bike is fully protected. The policy may limit certain valuable items or require extra coverage.

This is where scheduled personal property can help. A scheduled personal property endorsement, sometimes called a rider, lets you list a specific valuable item on your policy. For a high-value bike, this can provide broader protection, higher limits, and sometimes a lower or zero deductible. Scheduled coverage may also help with risks that a base policy doesn’t fully cover, such as mysterious loss or accidental damage, depending on the insurer. If you own a carbon road bike, custom mountain bike, racing bike, or expensive e-bike, scheduling it may be smarter than hoping your standard policy is enough.

4 Things You Must Provide to Get Your Claim Approved

If your bike is stolen, move quickly. A strong bike theft claim depends on documentation.

- First, file a police report. Most insurers will ask for it before approving a theft claim. Make sure the report includes where the bike was stolen, when it happened, and any evidence of forced theft, such as a cut lock.

- Second, provide the serial number. This is one of the most important details. Many stolen bike claims become harder because the owner never recorded the serial number. Take a photo of it before anything happens.

- Third, show proof of purchase. A receipt, credit card statement, retailer invoice, online order confirmation, or appraisal can help prove the bike’s value.

- Fourth, include photos and lock evidence if possible. Photos of the bike, the broken lock, the rack, accessories, upgrades, and maintenance records can support your claim.

Conclusion

Renters insurance will often cover theft of a bike outside your home, but coverage isn’t the same as full reimbursement. Your final payout depends on your deductible, actual cash value vs replacement cost, sublimits, exclusions, and whether your bike is standard, electric, professional-use, or high-value.

Before your bike disappears, register the serial number, save your receipt, photograph the bike, and check your policy limits. If your bike is worth more than you could comfortably replace out of pocket, ask about scheduled personal property or separate bicycle insurance. A good lock helps prevent theft, but the right coverage helps you recover when prevention isn’t enough.