Low-income car insurance isn’t a single national program, but there are real ways to reduce your premium if money is tight. In 2026, the best option depends heavily on where you live. If you’re in California, New Jersey, Hawaii, or Maryland, you may qualify for a state backed program designed to help low-income drivers stay legally insured. Some programs can bring annual costs down to roughly $250 to $400, depending on eligibility, vehicle value, medical status, and state rules.

If your state doesn’t offer a special program, the next cheapest path is usually state minimum liability coverage. This can cost far less than full coverage because it only meets your state’s legal requirements instead of protecting your own car against theft, weather, or collision damage. For drivers who are choosing between insurance and other bills, that price difference can be the reason they stay legally on the road.

The goal isn’t only to find cheap car insurance. It’s to find affordable car insurance that keeps your license active, protects you from penalties, and prevents one accident from becoming a financial crisis.

Government Programs That Offer the Cheapest Car Insurance Rates for Low-Income Drivers

While most drivers shop through private insurance companies, several state-sponsored programs provide significantly lower rates for qualifying households. These programs are designed to help low-income drivers maintain legal coverage without paying the high premiums often found in the standard market.

Quick Comparison of Low-Income Car Insurance Programs

| Program | State | Estimated Annual Cost | Who Qualifies | Coverage Level |

|---|---|---|---|---|

| California Low Cost Auto Insurance (CLCA) | California | $244–$966 | Income-qualified drivers | Basic liability |

| Special Automobile Insurance Policy (SAIP) | New Jersey | About $365 | Certain Medicaid recipients | Limited medical coverage |

| Hawaii Public Assistance Auto Coverage Programs | Hawaii | Varies by eligibility | Certain public assistance recipients | Limited assistance |

| Maryland Auto Insurance | Maryland | Higher than CLCA/SAIP | Drivers denied private coverage | Standard state-required coverage |

| Assigned Risk Plans | Multiple States | Varies by state | High-risk or hard-to-insure drivers | State minimum coverage |

California Low Cost Automobile Insurance Program (CLCA)

The California Low Cost Automobile Insurance Program is often considered one of the best options for low-income drivers in the United States. Created by the state government, it provides affordable liability coverage to drivers who meet income requirements and own relatively modest vehicles.

Annual premiums generally range from approximately $244 to $966, depending on the county where you live and your driving profile. To qualify, applicants must meet household income limits, possess a valid driver’s license, and own a vehicle that falls below the program’s maximum value threshold. The biggest advantage of CLCA is cost. Many drivers pay substantially less than they would through traditional insurance companies. However, coverage is limited primarily to liability protection, meaning damage to your own vehicle may not be covered after an at-fault accident.

New Jersey Special Automobile Insurance Policy (SAIP)

The Special Automobile Insurance Policy, commonly called the “Dollar-a-Day” program, offers one of the lowest car insurance rates available anywhere in the country. Eligible drivers typically pay about $365 per year. SAIP is only available to certain New Jersey residents enrolled in Medicaid programs that include hospitalization benefits. Because eligibility is restricted, many drivers won’t qualify. The low price comes with important limitations. Unlike standard auto insurance, SAIP primarily covers emergency medical treatment following an accident and does not provide broad liability or collision protection. Drivers should carefully review the coverage before relying on it as their only policy.

Hawaii Assistance Programs for Low-Income Drivers

Hawaii offers limited assistance options for certain residents receiving public aid. Eligibility requirements can be strict and may vary depending on the specific program available at the time. While savings can be significant for qualifying households, these programs are generally less accessible than California’s CLCA or New Jersey’s SAIP. Drivers should contact local agencies or the Hawaii Insurance Division to determine current eligibility requirements and available benefits.

Maryland Auto Insurance

Maryland Auto Insurance serves drivers who struggle to obtain coverage through traditional insurers. While it may not always provide the absolute cheapest premium, it can be a critical option for drivers who have been declined elsewhere due to poor driving history, lapses in coverage, or other underwriting issues. Premiums vary widely based on driver characteristics, but the program ensures access to legally required insurance coverage when private-market options are unavailable. For many high-risk drivers, the value lies less in the price and more in the ability to obtain coverage at all.

State Assigned Risk Plans

Many states operate Assigned Risk Plans that help drivers secure coverage when private insurers refuse to write a policy. These plans generally do not offer the lowest premiums, but they provide guaranteed access to insurance for drivers who might otherwise be uninsured. Rates vary significantly by state and driving history. Although these plans are usually more expensive than programs like CLCA or SAIP, they often remain cheaper than driving uninsured and facing fines, license suspensions, or legal penalties.

Which Program Offers the Cheapest Rates?

For drivers who qualify, New Jersey’s SAIP program typically offers the lowest annual cost at roughly $365 per year. California’s CLCA program is often the next most affordable option, with some drivers paying less than $300 annually depending on location and eligibility. However, the cheapest program isn’t always the best value. Drivers should compare the cost savings against the coverage provided. A policy with a slightly higher premium may offer significantly better protection after an accident, making it the smarter long-term choice.

What if My State Doesn’t Have a Program?

Most states don’t offer a dedicated low income car insurance program. That doesn’t mean you’re stuck paying the highest rate. It means you need to shop more carefully.

Compare Quotes From Multiple Insurance Companies

The first strategy is to compare car insurance quotes from multiple companies. Prices can vary dramatically for the same driver, same car, and same address. One insurer may treat your profile as high risk while another may price you much more fairly.

Consider State Minimum Coverage for Older Paid-Off Cars

The second strategy is choosing state minimum coverage if you own your car outright. This is often the cheapest legal option. However, it won’t repair your own car after an accident you cause. If your vehicle is old and paid off, that tradeoff may be acceptable. If your car is newer or essential for work, you need to think carefully before dropping full coverage.

Ask About Every Available Discount

The third strategy is asking about car insurance discounts. Many drivers miss savings because they don’t ask. Discounts may apply for safe driving, low mileage, paperless billing, automatic payments, defensive driving courses, good student status, anti-theft devices, and bundling with renters insurance. Pay per mile insurance can also help if you don’t drive much. If you work from home, use public transit, or only drive for errands, a mileage based plan may lower your cost compared with a traditional policy.

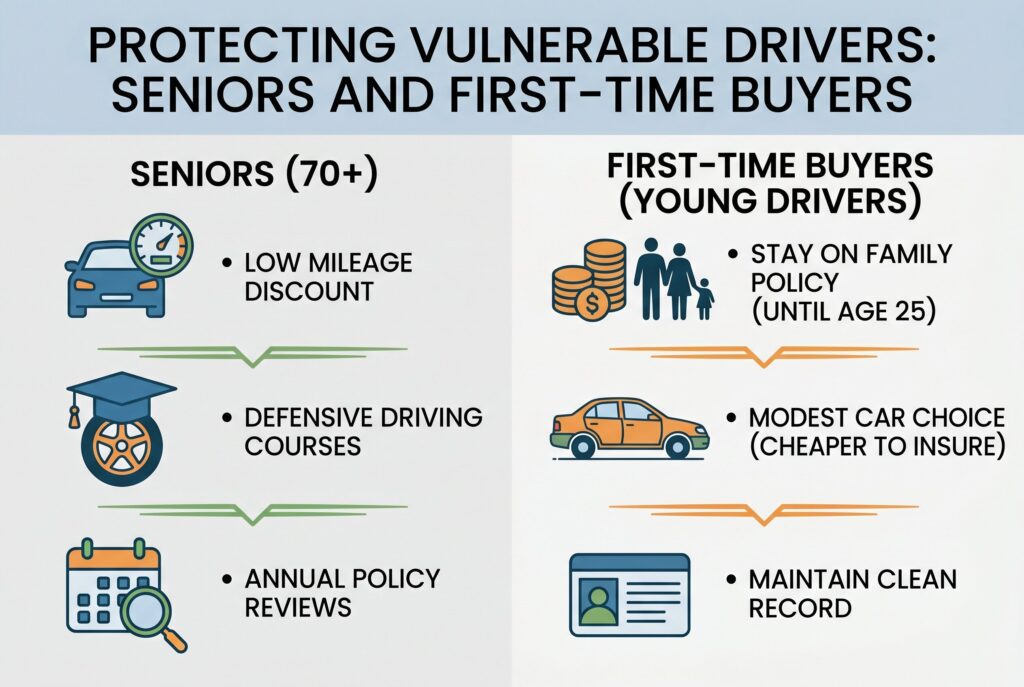

Protecting Vulnerable Drivers: Seniors and First Time Buyers

Auto insurance can be challenging for both seniors and young drivers, but for different reasons. Seniors often see rates increase after age 70 as insurers factor in age-related risk, even with decades of safe driving. To lower costs, they should ask about low-mileage discounts, complete defensive driving courses, and review their policy annually.

Young drivers typically pay more because they lack a driving history. Rates often begin to decrease around age 25 for drivers with clean records, and staying on a family policy is usually the most affordable option. For first-time buyers, choosing a reliable used sedan instead of a sports car or luxury vehicle can also help keep insurance costs down.

The Vehicle Trap: Zero Down Car Loans and High Premiums

For many low-income buyers, a zero-down car loan can make vehicle ownership possible when saving thousands of dollars for a down payment simply isn’t realistic. It allows drivers to get transportation for work, school, or family responsibilities without a large upfront expense. This can be especially helpful for people who need a car immediately but have limited savings.

However, there are important tradeoffs to understand before choosing a zero-down financing option. Most lenders require full coverage insurance until the loan is paid off, which means you may not be able to purchase the cheaper state-minimum coverage that many budget-conscious drivers prefer. As a result, your monthly insurance premium can be significantly higher than expected.

Low-income buyers should also be aware that zero-down loans often come with higher monthly payments and may cost more in interest over time. Before signing, it’s important to compare the total monthly cost of the loan and insurance together, not just the car payment. If possible, choosing an affordable, reliable vehicle and borrowing only what you need can help keep both financing and insurance costs manageable.

Conclusion

Driving uninsured may feel like the only option when bills are overwhelming, but it can create much bigger problems. You could face fines, license suspension, vehicle impoundment, higher future premiums, and personal responsibility for accident costs.

Low-income car insurance is about finding the lowest safe path to legal protection. Start by checking whether your state has a program. Then compare private quotes, ask for every discount, consider state minimum coverage if your car is paid off, and avoid loans that force you into premiums you can’t sustain.

The cheapest policy isn’t always the best policy, but no policy at all is usually the most dangerous choice. With the right strategy, affordable car insurance can keep your car legal, protect your income, and give you one less financial emergency to worry about.