Renters insurance can cover temporary housing, but only if your home becomes uninhabitable due to a covered peril, such as fire, storm damage, or certain types of water damage. This protection, known as loss of use or additional living expenses (ALE) coverage, may help pay for a hotel, temporary rental, meals, and other necessary extra costs while repairs are completed.

Before booking accommodations, contact your insurer to confirm coverage and understand your limits. Keeping receipts from the start can make the claims process much smoother.

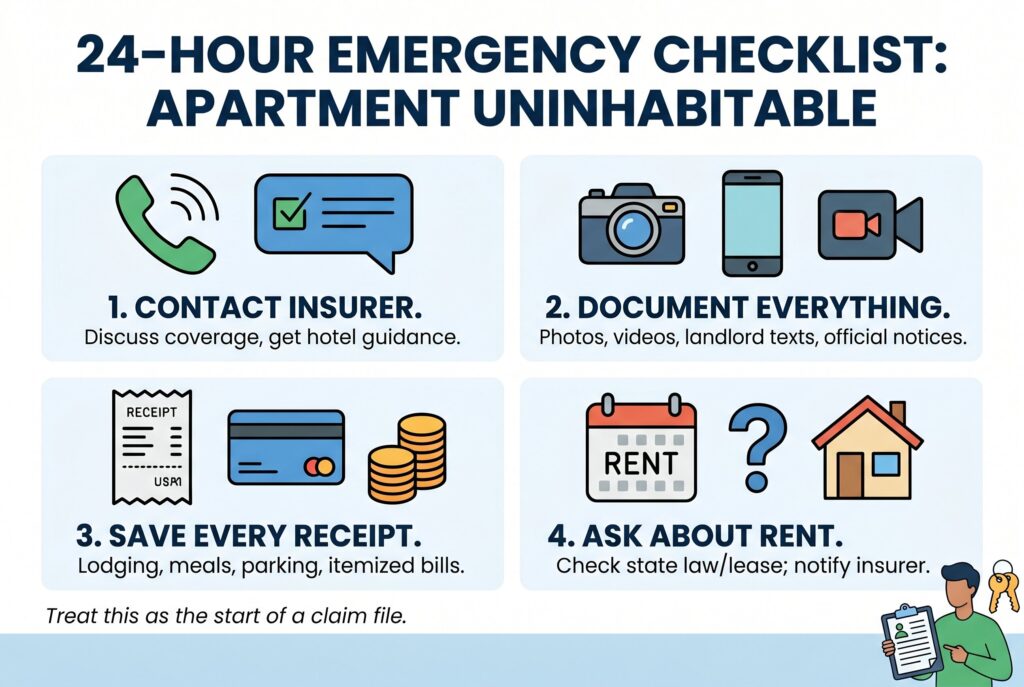

The 24 Hour Emergency Checklist

When your apartment suddenly becomes uninhabitable, don’t treat the first night like a vacation. Treat it like the beginning of a claim file.

First, contact your insurance company or agent as soon as you’re safe. Explain what happened, ask whether the event appears to be covered, and request guidance before choosing a hotel. If your studio apartment rents for $1,400 a month, the insurer probably won’t reimburse a luxury suite unless there’s no reasonable alternative.

Second, document everything. Take photos and videos of the damage, the blocked entrance, the soaked ceiling, the burned kitchen, or the official notice that says you can’t return. Keep texts from your landlord, fire department reports, repair notices, and evacuation orders.

Third, save every receipt. Meals, lodging, parking, laundry, rideshare charges, storage, pet boarding, and temporary rental deposits should all be tracked. A credit card statement alone may not be enough. Itemized receipts are cleaner and easier for adjusters to approve.

Fourth, ask about rent. If your apartment is legally uninhabitable, state law or your lease may affect whether you still owe rent. Don’t stop paying without checking local rules, but do tell your insurer if rent is reduced or paused because that changes the ALE calculation.

Decoding Loss of Use Coverage

Loss of use coverage is the part of renters insurance that helps you maintain a normal standard of living when a covered loss forces you out. Its purpose is to help you maintain your normal routine while your rental is being repaired.

So, does renters insurance cover hotel stays? Usually yes, if the stay is necessary because your apartment can’t be lived in after a covered peril. A hotel, extended stay hotel, short term apartment, or furnished rental may qualify if the cost is reasonable.

Food can also be reimbursed, but only the extra cost. If you normally spend $400 a month on groceries and now spend $700 because you’re eating restaurant meals, the insurer may consider the extra $300. The same logic applies to transportation. If your temporary housing adds a longer commute, extra gas, parking, tolls, or transit costs may be included.

Storage can also qualify if your belongings need to be moved while repairs happen. Pet boarding may be covered if your hotel doesn’t accept pets. Laundry costs may be reimbursed if your temporary housing doesn’t have a washer and dryer. The important phrase is extra necessary expense. If you would have paid the cost anyway, it usually isn’t ALE.

Covered Peril vs. Excluded Disaster

Renters insurance temporary housing coverage only works when the displacement comes from a covered peril. Common covered perils may include fire, smoke, explosion, theft related damage, vandalism, certain burst pipes, windstorms, hail, and some types of accidental water damage.

But some disasters are commonly excluded. Flooding from outside water usually isn’t covered by a standard renters policy unless you bought separate flood insurance. Earthquakes are usually excluded unless you added earthquake coverage. Long term mold, neglect, pest problems, gradual leaks, and poor maintenance may also be denied.

This is why the cause matters more than the inconvenience. If the apartment is uncomfortable but still legally habitable, loss of use may not apply. If the power is out for a few hours, that usually isn’t enough. If the ceiling collapses, the heat system fails during a dangerous cold after a covered event, or the fire department orders you out, the claim becomes much stronger.

Extended Stay Hotel vs. Temporary Apartment

If repairs will take only a few nights, a regular hotel may be fine. If repairs will take weeks or months, an extended stay hotel or furnished apartment can protect your ALE limit. Extended stay housing often includes a kitchenette, laundry access, workspace, parking, and weekly rates. That can lower meal costs because you can cook instead of eating out every day. A furnished apartment may feel more stable for families, remote workers, or renters with pets.

Before booking, ask your adjuster what they consider reasonable. Some insurers can connect you with temporary housing vendors. Others reimburse after you pay. If you can’t afford upfront hotel costs, say that clearly and ask about direct billing options.

3 Reasons Your Displacement Claim Will Be Denied

1. The Apartment Wasn’t Uninhabitable

Insurance companies generally provide temporary housing benefits only when a rental property becomes uninhabitable. If the damage is minor and the home remains safe to occupy, a request for temporary housing may be denied even if the situation is inconvenient or uncomfortable. Issues such as cosmetic damage, damaged flooring, broken cabinets, minor roof leaks, or limited repairs often do not qualify on their own. As long as the property remains structurally sound and essential services like water, electricity, and heating are available, insurers may determine that the home is still livable.

To support a temporary housing claim, you typically need evidence showing that the property is unsafe, impossible to live in, or legally restricted from occupancy. Photos, inspection reports, contractor assessments, utility outage records, and official notices can help demonstrate that the damage has made the rental uninhabitable.

2. The Cause Was Excluded

Certain situations can lead to more complicated claim decisions. Damage caused by floods, earthquakes, gradual wear and tear, pest infestations, or long-term maintenance problems is often treated differently from sudden and accidental losses. Depending on the cause of the damage, temporary housing benefits may be limited or excluded altogether.

Claims can become especially challenging when there is evidence that a problem existed for an extended period before the loss occurred. For example, if a landlord was aware of a leaking roof, plumbing issue, or mold problem for months and failed to address it, an insurer may determine that the situation resulted from ongoing neglect rather than a covered event. In these cases, renters insurance may not be the primary source of protection. Landlord insurance, local tenant protection laws, lease provisions, and potential legal remedies may play a larger role in helping tenants recover costs or secure alternative housing while the property is repaired.

3. The Spending Was Unreasonable

Additional Living Expense (ALE) coverage helps pay for temporary housing and other necessary expenses while your home is being repaired after a covered loss. The goal is to maintain your normal standard of living, not upgrade it. Insurers generally expect you to choose accommodations similar to your usual home, so always confirm coverage before booking expensive lodging to avoid paying the difference yourself.

Conclusion

So, does renters insurance cover temporary housing? In many cases, yes, but only for covered losses and within your policy limits. Understanding your loss of use coverage before an emergency, keeping receipts, and documenting your expenses can help you get the full benefits your policy provides when you need them most.

Related Articles

Does Renters Insurance Cover Airbnb? 2026 Theft and Damage Guide