Explained: How It Works, Key Risks, Benefits, and Who Should Choose It")

When shopping for a mortgage, many homebuyers are faced with a tough decision: fixed-rate mortgage or adjustable-rate mortgage (ARM)? While fixed-rate mortgages offer predictable payments, ARMs often come with lower initial rates, which can make them an attractive option for buyers looking to minimize payments in the early years. But what exactly is an ARM, how does it work, and is it right for you? In this article, we’ll break down everything you need to know about adjustable-rate mortgages (ARMs), from how they work to their benefits and risks, and who should consider them.

What Is an Adjustable-Rate Mortgage (ARM)?

An adjustable-rate mortgage (ARM) is a type of home loan where the interest rate is fixed for a specific period (usually 3, 5, 7, or 10 years) and then adjusts periodically based on market conditions. During the initial fixed-rate period, you enjoy lower interest rates compared to what you’d typically get with a fixed-rate mortgage. After this period, the rate adjusts based on the index (such as LIBOR or Treasury index) plus a margin set by your lender, which could lead to an increase or decrease in your payments.

For example, a 5/1 ARM would have a fixed rate for the first 5 years, after which it adjusts annually. The periodic adjustments are generally capped, so they won’t skyrocket uncontrollably, but they still create uncertainty about future payments.

How Do Adjustable-Rate Mortgages Work?

When you take out an ARM, you initially lock in a fixed interest rate for a predetermined number of years (the fixed period). After the fixed period, the interest rate is subject to market fluctuations. The adjustment happens periodically (annually or biannually, depending on your loan), based on a specific interest rate index, like the LIBOR (London Interbank Offered Rate) or Treasury index, plus a margin (a fixed percentage added to the index rate).

Example:

- If you have a 5/1 ARM, your rate is fixed for the first 5 years, and then it adjusts every year after that.

- If the index rate (for example, LIBOR) is 2% and your margin is 3%, your new interest rate after the first 5 years would be 5%.

Most ARMs have caps to prevent huge rate increases. These caps include periodic caps (limiting rate adjustments in any given period), lifetime caps (limiting the maximum rate increase over the life of the loan), and payment caps (limiting the increase in monthly payments).

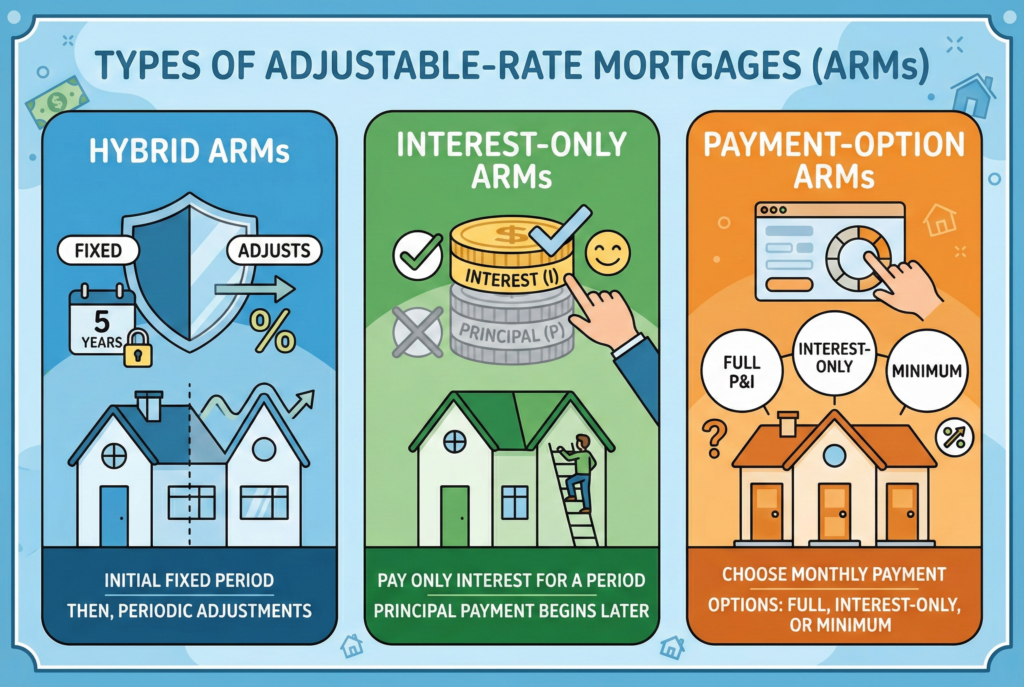

Types of ARMs

Hybrid ARMs

These combine the predictability of a fixed-rate period with the flexibility of an adjustable rate. For example, a 7/1 ARM has a 7-year fixed-rate period, followed by annual adjustments thereafter.

Interest-Only ARMs

These loans allow you to pay only the interest for a set period (usually 5–10 years). This can significantly lower your monthly payments in the initial years, but it also means that you aren’t reducing your principal during this time. At the end of the interest-only period, your payments will increase.

Payment-Option ARMs

These loans give you the option to choose how much you want to pay each month, with the lowest payment being an interest-only option. However, paying less than the required amount can result in negative amortization, where your loan balance actually increases over time.

Pros of an Adjustable-Rate Mortgage

Lower Initial Payments

The most obvious benefit of an ARM is the lower initial interest rates, which can save you money during the early years of your mortgage. This is particularly beneficial for first-time homebuyers or those who expect to refinance or sell the house within a few years.

Potential for Rate Reductions

If interest rates fall, your payments could decrease, making ARMs appealing in a declining interest rate environment. This can be an advantage over fixed-rate mortgages, which remain locked in regardless of market conditions.

Great for Short-Term Homeowners

If you don’t plan to stay in your home for long (for example, 5 to 7 years), an ARM allows you to enjoy lower rates without worrying about the long-term risks of interest rate increases after the fixed period.

Cons of an Adjustable-Rate Mortgage

Uncertainty and Risk of Rate Increases

The biggest disadvantage of an ARM is the uncertainty. Once the initial fixed-rate period ends, your payments can increase significantly, especially if market interest rates rise.

Payment Shock

If interest rates increase substantially, you could experience payment shock, where your monthly mortgage payments increase by a significant amount. For example, if your rate increases by several percentage points, your monthly payment could increase by hundreds of dollars.

Negative Amortization

With interest-only or payment-option ARMs, you could face negative amortization, where you pay less than the required interest and end up owing more than you borrowed.

Who Should Choose an ARM?

An adjustable-rate mortgage can be a good choice if:

- You plan to move or refinance within the fixed-rate period (typically 5, 7, or 10 years).

- You expect your income to increase over time and can handle potential payment increases.

- You want to take advantage of lower initial rates and are comfortable with the risk of rate changes.

However, if you’re planning on staying in the same house for decades or if you have a fixed budget that can’t handle unpredictable payments, a fixed-rate mortgage might be a better option.

How to Minimize the Risks of an ARM

Understand The Caps

Make sure you know the periodic and lifetime caps on rate adjustments. This will help you estimate the maximum amount your payments could rise.

Consider Refinancing

Keep track of the interest rate market. If rates drop significantly, consider refinancing into a fixed-rate mortgage before your rate adjusts.

Budget For Potential Increases

Plan for the possibility that your payments might increase. Make sure your budget can accommodate potential payment hikes, and try to save money during the fixed-rate period to cover future increases.

Conclusion

Adjustable-rate mortgages can be an excellent tool for certain buyers, especially those who plan to move or refinance in a few years or expect their financial situation to improve. However, they come with risks, and it’s crucial to understand how ARMs work, their benefits, and their potential drawbacks. By knowing when an ARM makes sense and how to minimize its risks, you can make a more informed decision about your mortgage and take advantage of lower initial payments while still protecting your long-term financial stability.

Related Articles

30-Year Fixed Mortgage Explained: Pros, Cons, Costs, and Who This Loan Works Best For