Growing your retirement savings faster doesn’t usually come from one dramatic financial move. It’s more often the result of steady contributions, thoughtful investing, and a plan that keeps working through different stages of life. For many households in the United States, retirement saving competes with housing costs, insurance, debt payments, and everyday expenses. That can make progress feel slow at first. Still, a well-structured approach can help you build momentum and make your savings work harder over time. Rather than chasing quick gains or constantly adjusting your portfolio, the goal is to pair smart investing with consistent long-term contributions so your retirement savings can grow in a practical, disciplined, and sustainable way.

Start With Contribution Consistency Before Chasing Higher Returns

Many people focus first on investment performance, but contribution consistency usually matters more in the early and middle stages of retirement saving. If you’re contributing regularly, you’re building the base that future growth depends on. Without that foundation, even a strong investment year won’t have as much impact.

This is why automated retirement contributions are so effective. When money moves into your retirement account through payroll deductions or scheduled transfers, you’re less likely to skip months or reduce savings on impulse. The habit becomes part of your financial system rather than a decision you have to remake every month.

Consistent contributions also help smooth out market uncertainty. You won’t be depending on finding the perfect moment to invest. Instead, you’ll be adding money over time, which supports long-term discipline and reduces emotional decision-making.

Contribute Enough to Capture Employer Matching

If you have access to a workplace retirement plan with an employer match, this is often one of the fastest ways to improve your retirement progress. Matching contributions can immediately increase the amount going into your account, which gives your money more time and more capital to grow.

Too many workers leave part of that benefit unused because they delay enrolling or contribute less than needed to qualify for the full match. If your budget allows it, reaching that threshold is usually one of the most valuable starting points in retirement planning.

This strategy matters because it improves growth without requiring you to take more investment risk. It strengthens your retirement savings simply by making full use of a benefit already available to you.

Increase Contributions Gradually Instead of Waiting for the Perfect Time

A common mistake is assuming retirement contributions need to begin at a high level to be worthwhile. In reality, gradual increases can be extremely effective. Starting with a manageable amount and raising it over time often works better than waiting until your finances feel perfect.

For example, increasing your contribution rate whenever you receive a raise can help your retirement savings grow faster without placing all the pressure on your current budget. Even small increases can add up significantly over time, especially when paired with compounding.

This approach also helps reduce lifestyle inflation. When part of each income increase goes directly toward retirement, you’re more likely to strengthen your long-term security instead of allowing every raise to disappear into higher spending.

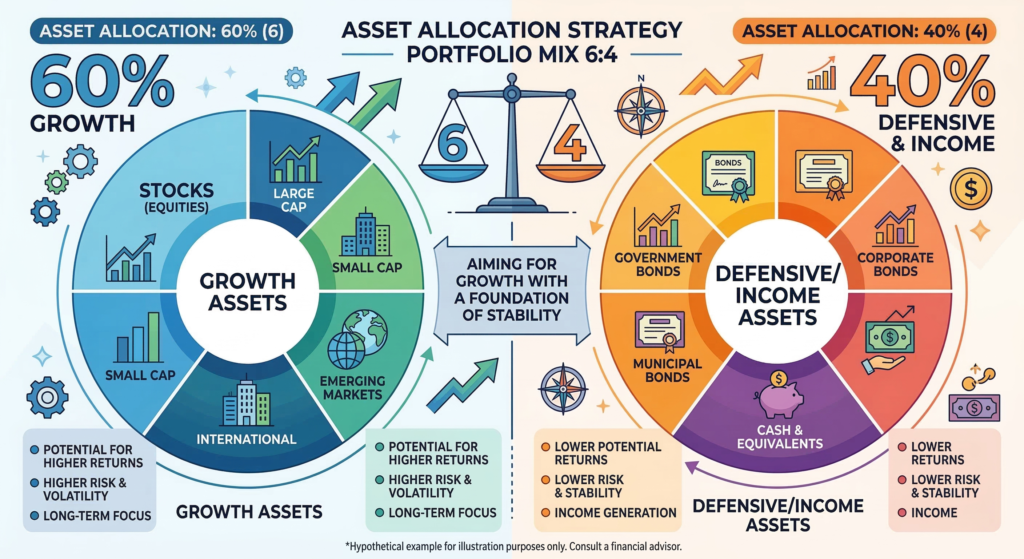

Focus on Asset Allocation, Not Market Predictions

Trying to predict short-term market moves is one of the least reliable ways to build long-term retirement wealth. A better approach is choosing an asset allocation that fits your age, time horizon, and risk tolerance, then staying consistent with it.

Asset allocation refers to how your investments are divided among categories such as stocks, bonds, and cash equivalents. A younger investor with decades until retirement may choose a more growth-oriented mix. Someone closer to retirement may want a more balanced allocation that still supports growth but reduces extreme volatility.

The right mix should help you stay invested through market ups and downs. If your portfolio is so aggressive that you panic during downturns, or so conservative that growth stays weak for years, it may not support your long-term goals effectively. Smart investing is often less about finding the hottest investment and more about building a portfolio you can stick with.

Let Compounding Work by Staying Invested for the Long Term

One of the most powerful tools in retirement saving is compound growth. When your investments generate returns and those returns remain invested, future growth builds on a larger base. Over long periods, that effect can become substantial.

But compounding only works well when time remains on your side and when money stays invested. Pulling back contributions during every downturn or moving in and out of the market can interrupt that process. The most effective long-term investors usually aren’t the ones making constant changes. They’re the ones who keep contributing and stay invested through different market environments.

This is especially important during volatile periods. Market declines can feel discouraging, but they don’t automatically mean your strategy is broken. For long-term savers, consistency during those periods can actually support future growth.

Use Diversification to Support Growth With Manageable Risk

Growing retirement savings faster doesn’t mean concentrating all your money in one area. In fact, excessive concentration can create more risk than reward. A diversified portfolio spreads investments across different asset types, sectors, and sometimes geographic markets so that one weak area doesn’t determine your entire outcome.

Diversification doesn’t prevent losses, and it doesn’t guarantee returns. What it can do is help create a more balanced investing experience over time. That balance often makes it easier to stay committed to your plan, which is critical for long-term progress. For many savers, diversified mutual funds, index funds, or target-date funds offer a practical way to build retirement exposure without constantly managing individual investments.

Keep Fees Low So More Growth Stays in Your Account

Investment fees may look small on paper, but over the long run they can reduce how much of your portfolio growth you actually keep. Because retirement investing often spans decades, even modest differences in expense ratios and account fees can have a meaningful effect. This doesn’t mean the lowest-cost option is always automatically the best. It does mean fees deserve attention. If two funds serve a similar purpose, lower ongoing costs can help preserve more of your returns over time.

Reviewing your retirement accounts periodically to understand what you’re paying is a smart part of long-term planning. Keeping costs reasonable is one of the few parts of investing you can control directly.

Protect Retirement Progress by Managing High-Interest Debt

Retirement growth is easier when your broader financial life is stable. If high-interest debt is consuming a large portion of your cash flow, it can become much harder to contribute consistently or raise contribution levels over time.

This is why retirement saving and debt management often need to be addressed together. That doesn’t necessarily mean stopping retirement contributions entirely while paying off debt. In many cases, especially when employer matching is involved, it makes sense to do both. The key is creating enough balance that debt doesn’t keep forcing you to interrupt long-term investing. A stable budget, manageable debt, and a basic emergency fund all make it easier to stick with retirement contributions through real-life financial challenges.

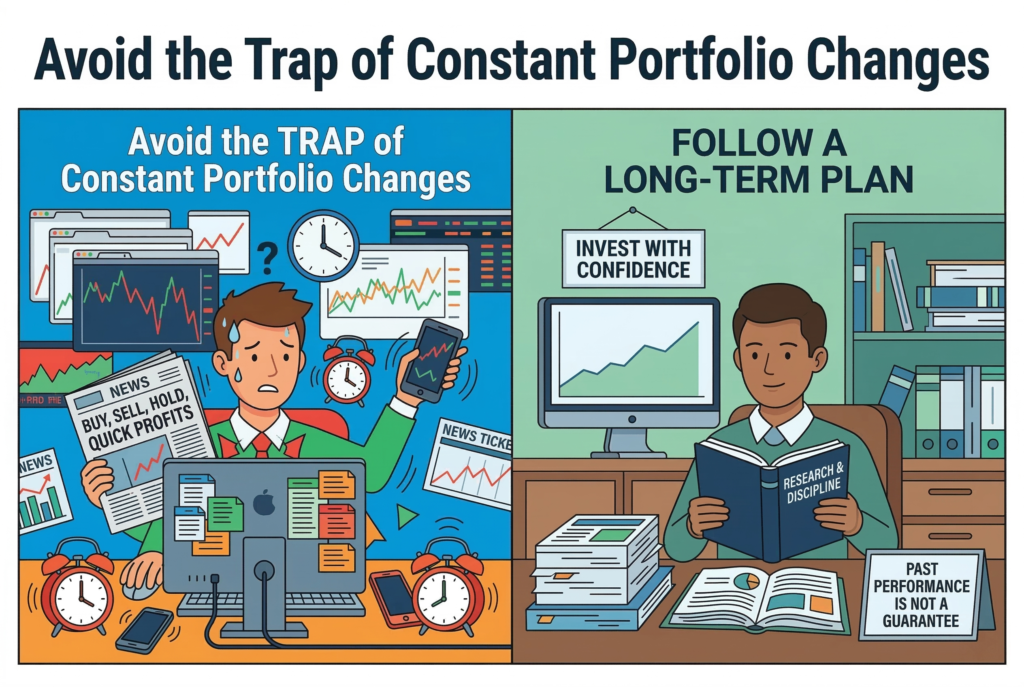

Avoid the Trap of Constant Portfolio Changes

It’s natural to want to improve your returns by reacting to news, economic headlines, or market trends. But constant portfolio changes can undermine long-term results. Frequent shifts often come from fear or excitement rather than a disciplined process.

Retirement investing works best when changes are intentional and based on meaningful life developments, such as a different retirement timeline, a major shift in income, or a reassessment of risk tolerance. Outside of those situations, staying consistent is usually more valuable than making repeated tactical adjustments. A portfolio doesn’t need to feel exciting to be effective. In fact, a steady, well-structured plan is often what supports the strongest long-term outcomes.

Rebalance Periodically to Keep Your Strategy Aligned

Over time, market performance can shift your portfolio away from its intended balance. If stocks perform very strongly for several years, for example, they may end up representing a larger share of your retirement account than you originally planned. Rebalancing helps bring your portfolio back in line with your target allocation. This process can reduce unintended risk and keep your investment strategy aligned with your goals. It doesn’t need to happen constantly. For many investors, reviewing allocation periodically is enough.

The purpose of rebalancing goes beyond maximizing short-term gains. It helps maintain discipline and keeps your portfolio from drifting into a risk profile that no longer fits your situation.

Think Beyond the Account Balance

It’s easy to measure retirement progress only by the size of your account, but long-term success also depends on how your savings may support future income. A growing balance is important, but so is the ability of that balance to help fund housing, healthcare, daily living, and other retirement costs over time.

That’s why faster retirement growth should be paired with thoughtful planning. Contribution rates, investment choices, expected retirement age, and future spending all connect to the bigger picture. A larger account balance matters most when it supports a sustainable retirement lifestyle. Keeping that perspective can help you make better decisions now. Instead of chasing performance alone, you’ll focus on building a retirement plan that supports both growth and long-term stability.

Conclusion

Growing your retirement savings faster with smart investing and consistent long-term contributions comes down to a few disciplined habits. Contribute regularly, take full advantage of employer matching when available, increase savings gradually as income rises, use a diversified investment strategy, keep fees in check, and stay committed through changing market conditions. These steps may not feel dramatic, but over time they can make a powerful difference.

Retirement progress depends less on perfect timing or constant portfolio changes and more on consistency, patience, and a plan you can maintain in real life. When you combine steady contributions with sound long-term investing decisions, you give your retirement savings a stronger chance to grow and support the future income you’ll eventually need.

Related Articles

- A Practical Guide to Balancing Retirement Savings and Living Well Today

- Costly Retirement Savings Mistakes That Can Damage Your Financial Stability

- How Inflation Impacts Retirement Planning Over Time and What to Do About It

- A Practical Guide to Adjusting Your Retirement Plan as Life Changes

- A Practical Guide to Preparing for Retirement Without Feeling Overwhelmed