Your credit utilization ratio is one of the most important factors in your credit profile because it shows how much of your available revolving credit you’re using at a given time. Even if you pay your bills on time, a high utilization ratio can still hurt your credit score and make lenders view you as a riskier borrower. Understanding how this ratio works can help you make better borrowing decisions and improve your overall financial health.

What Is a Credit Utilization Ratio?

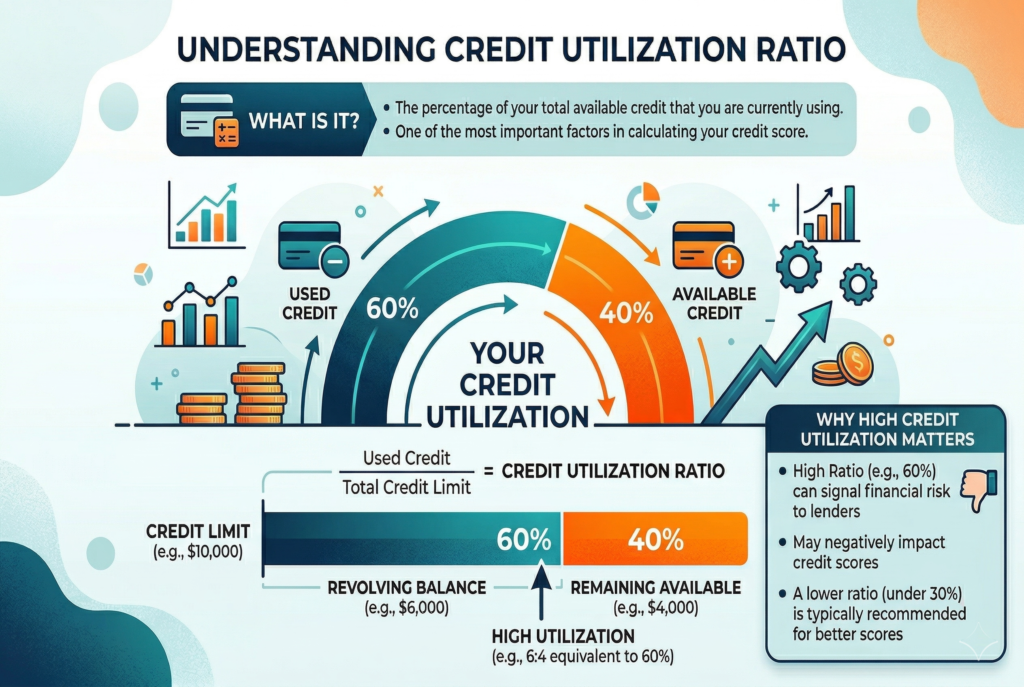

A credit utilization ratio is the percentage of your available revolving credit that you’re currently using. It’s most commonly calculated using credit cards and other revolving credit lines, not installment loans like mortgages, auto loans, or standard personal loans.

For example, if you have a total credit limit of $10,000 across all your credit cards and your combined balances are $2,500, your credit utilization ratio is 25 percent. The formula is simple: divide your total card balances by your total credit limits, then multiply by 100.

Lenders and credit scoring models pay close attention to this number because it helps indicate how dependent you may be on borrowed money. A lower ratio often suggests that you’re using credit conservatively, while a higher ratio can signal greater financial strain, even if you haven’t missed any payments.

Why Credit Utilization Matters So Much

Your credit utilization matters because it’s one of the clearest signals of revolving credit behavior. A person who uses only a small share of available credit often appears more financially stable than someone who is close to maxing out their cards.

This is why utilization can influence your credit score so strongly. It doesn’t just reflect what you owe. It also reflects how much flexibility remains in your available credit. Someone with low utilization may appear better positioned to handle unexpected expenses or new borrowing than someone already using most of their limits.

This factor is especially important because it can change quickly. Unlike some credit score components that take years to build, such as length of credit history, utilization can rise or fall within a billing cycle depending on balances and payments.

How Credit Utilization Ratio Is Calculated

There are two main ways utilization is looked at. The first is overall utilization, which compares all your revolving balances against all your revolving credit limits combined. The second is per-card utilization, which measures the balance on each individual card against that card’s specific limit.

Both can matter. For example, you might have low overall utilization across several cards, but if one card is nearly maxed out, that can still look risky. A person with three cards totaling $15,000 in available credit and $3,000 in combined balances may have a fairly reasonable overall ratio of 20 percent. But if one of those cards has a $3,200 limit and carries a $3,000 balance, that individual card is heavily utilized.

This is why improving utilization isn’t only about the total amount you owe. It’s also about how those balances are distributed across your credit accounts.

How Credit Utilization Ratio Affects Your Credit Score

A high credit utilization ratio can lower your credit score because it suggests you may be relying too heavily on revolving credit. Even when payments are made on time, carrying large balances relative to your limits can raise concerns for lenders and scoring models.

The impact can be surprisingly noticeable. A person with otherwise solid credit habits may still see score pressure if card balances rise too high, especially if those balances are reported near the statement closing date. This often catches people off guard because they assume on-time payments alone are enough to protect their score.

They’re important, but they aren’t the whole picture. Credit scores are designed to evaluate several behaviors at once, and utilization is one of the most visible ongoing signals. A lower ratio generally supports stronger credit health because it shows you aren’t stretching your revolving credit too far.

What Is Considered a Good Credit Utilization Ratio?

In general, lower credit utilization is better than higher utilization, but extremely low isn’t always the only goal. Many people aim to keep utilization below 30% because that’s often seen as a broad upper boundary for healthier credit management. Still, many strong credit profiles tend to have much lower utilization than that.

A ratio in the single digits or low teens often looks stronger than one that sits closer to 30%. Using your credit cards isn’t an issue; however, maintaining low balances compared to your credit limits can help improve your score. What matters most is consistency. If your balances regularly stay high, your score may reflect that ongoing pressure. If your utilization stays low most of the time, that usually sends a more favorable signal.

Why High Balances Can Hurt Even if You Pay on Time

One of the most frustrating parts of credit utilization ratio is that it can affect your score even when you’ve never missed a payment. This happens because credit card issuers usually report balances to the credit bureaus at specific points in the billing cycle, often around the statement closing date.

If your reported balance is high when the issuer sends that information, your score may reflect high utilization even if you plan to pay the card off a few days later. In other words, the timing of your payment can matter almost as much as the payment itself.

This is one reason people sometimes notice a drop in their score after using a card heavily for travel, large purchases, or temporary expenses. The balance may have been short-lived, but if it was reported at the wrong time, it may still influence the score until the next update.

Common Reasons Credit Utilization Gets Too High

There are several common reasons utilization rises. One is relying on credit cards for routine expenses when income is tight. Another is making a large purchase and letting the balance report before paying it down. Even temporary spending spikes can affect the ratio if they coincide with the reporting date.

Some people also run into trouble because they have low total credit limits. In that case, even moderate spending can produce a high utilization ratio. A person with only $1,500 in total available credit doesn’t need a large balance for the ratio to climb quickly.

Closing old credit cards can also raise utilization unexpectedly. When an account is closed, its available credit limit is removed from the total. If balances stay the same while total limits shrink, the utilization ratio rises.

How to Improve Your Credit Utilization Ratio

The most direct way to improve your credit utilization ratio is to lower your credit card balances. Paying down debt reduces the percentage of available credit you’re using and can quickly improve how your credit profile looks.

Making payments before the statement closing date can also help. If you pay part of the balance early, the amount reported to the credit bureaus may be lower, which can improve utilization even before the due date arrives.

Another strategy is spreading balances more evenly across cards instead of letting one card carry most of the burden. This can help reduce high utilization on a single account, which may matter even if your overall ratio isn’t extreme. In some cases, requesting a credit limit increase may help as well, provided you don’t use the added limit as an excuse to spend more. A higher limit can lower your ratio by increasing available credit, but it only works if balances don’t rise alongside it.

Should You Avoid Using Credit Cards Altogether?

Avoiding credit cards entirely isn’t usually necessary to manage credit utilization well. In fact, responsible card use can help support a healthy credit profile. The key is using credit in a way that remains controlled and affordable.

It’s possible to use cards regularly for convenience, rewards, or recurring bills and still maintain a low utilization ratio by paying balances promptly and keeping spending within your budget. The problem isn’t card use itself. The problem is letting balances grow too high relative to available limits. A practical goal is to treat credit cards as a payment tool, not a source of long-term borrowing unless there’s a clear repayment plan in place.

Mistakes to Avoid When Trying to Improve Utilization

One common mistake is closing old credit cards after paying them off. While this may feel like a clean financial move, it can reduce your available credit and push your utilization ratio higher.

Another mistake is focusing only on the due date. Paying on time is essential, but if you wait until after a high balance has already been reported, your score may still reflect that elevated utilization temporarily.

Some people also assume a balance must be carried from month to month to help their credit. That isn’t true. Carrying debt and paying interest isn’t required to show responsible credit use. What helps is demonstrating controlled use and timely payment, not keeping unnecessary debt.

How Credit Utilization Fits Into Overall Credit Health

Your credit utilization ratio is important, but it’s only one part of your overall credit picture. Payment history, account age, credit mix, and recent applications also matter. A strong score usually reflects a combination of good habits rather than one perfect metric.

Still, utilization deserves special attention because it’s so easy to overlook and because it can change so often. Someone who pays on time and avoids major credit mistakes may still hold back their score if they regularly allow balances to report too high.

Managing utilization well can strengthen the impact of your other positive habits and make your overall credit profile more attractive to lenders.

Conclusion

A credit utilization ratio measures how much of your available revolving credit you’re using, and it plays a major role in shaping your credit score. High utilization can hurt your score even when you pay on time, while lower utilization usually signals stronger credit management and lower borrowing risk. By paying down balances, making payments before statement dates, avoiding unnecessary card closures, and keeping credit use within a manageable range, you can improve your utilization ratio and build a healthier credit profile over time.