Buying a home usually requires more money than most people can pay upfront, which is why mortgages play such a central role in homeownership. A mortgage makes it possible to buy a property now and repay the loan over time through monthly payments. For homebuyers in the United States, understanding how a mortgage works, what loan types are available, and how to compare options can make a major difference in both affordability and long-term financial stability.

What Is a Mortgage?

A mortgage is a loan used to buy a home or other real estate. The lender provides money for the purchase, and the borrower agrees to repay that amount over a set period, usually with interest.

The home itself serves as collateral for the loan. That means if the borrower stops making payments, the lender can take legal steps to recover the property through foreclosure. Because the loan is secured by real estate, mortgage rates are often lower than rates on unsecured debt like credit cards or personal loans.

Most mortgages are repaid in monthly installments over 15 years, 20 years, or 30 years. Each payment typically includes principal, interest, property taxes, and homeowners insurance. In some cases, mortgage insurance may also be included.

How a Mortgage Works

A mortgage loan allows you to borrow a large amount and repay it gradually. The amount you borrow is called the principal. In return for lending that money, the lender charges mortgage interest.

Each month, part of your payment goes toward interest and part goes toward reducing the loan balance. Early in the loan, a larger share of the payment usually goes toward interest. Over time, more of the payment starts going toward principal. This repayment process is known as amortization.

For example, if you buy a home with a down payment and finance the rest with a mortgage, the lender calculates your monthly payment based on the loan amount, interest rate, and term. If you have a fixed-rate loan, the principal and interest portion typically stays the same each month, though taxes and insurance can still change. Understanding this structure matters because the full cost of a home loan goes beyond the purchase price. Interest, fees, insurance, and taxes all affect what you’ll actually pay over time.

The Main Parts of a Mortgage Payment

A typical mortgage payment includes several components, often referred to as PITI.

- Principal is the portion that reduces the amount you owe on the loan.

- Interest is the cost of borrowing money from the lender.

- Taxes usually refer to local property taxes, which may be collected monthly through escrow.

- Insurance generally includes homeowners insurance, and sometimes flood insurance if required.

Some borrowers also pay mortgage insurance, especially if the down payment is small. This can apply to conventional loans with private mortgage insurance or to government-backed loans with their own insurance structure. Knowing what’s included in your monthly housing payment is important because the mortgage rate alone doesn’t tell the full story.

Common Types of Mortgages

Fixed-Rate Mortgage

A fixed-rate mortgage has an interest rate that stays the same for the life of the loan. This means the principal and interest payment remains stable, making budgeting easier. This is one of the most popular mortgage types because it offers predictability. It’s often a strong fit for buyers who expect to stay in the home for many years and want consistent monthly payments.

Adjustable-Rate Mortgage

An adjustable-rate mortgage, or ARM, starts with a fixed interest rate for an initial period and then adjusts based on market conditions. It may begin with a lower rate than a fixed loan, but the rate can rise later. This type of mortgage may work for borrowers who plan to move, sell, or refinance before the adjustable period begins. Still, it carries more uncertainty.

Conventional Loan

A conventional mortgage is a home loan that isn’t backed by the federal government. These loans often require stronger credit and may have stricter qualification standards than some government-backed options. Conventional loans can be attractive for borrowers with solid credit, stable income, and a competitive down payment.

FHA Loan

An FHA loan is backed by the Federal Housing Administration. It’s designed to help borrowers who may have lower credit scores or smaller down payments qualify for home financing. These loans can make homeownership more accessible, but they also come with mortgage insurance requirements that can increase total loan cost.

VA Loan

A VA loan is backed by the Department of Veterans Affairs and is available to eligible service members, veterans, and some surviving spouses. These loans can offer valuable benefits, including no required down payment in many cases and no private mortgage insurance. For eligible borrowers, a VA loan can be one of the strongest mortgage options available.

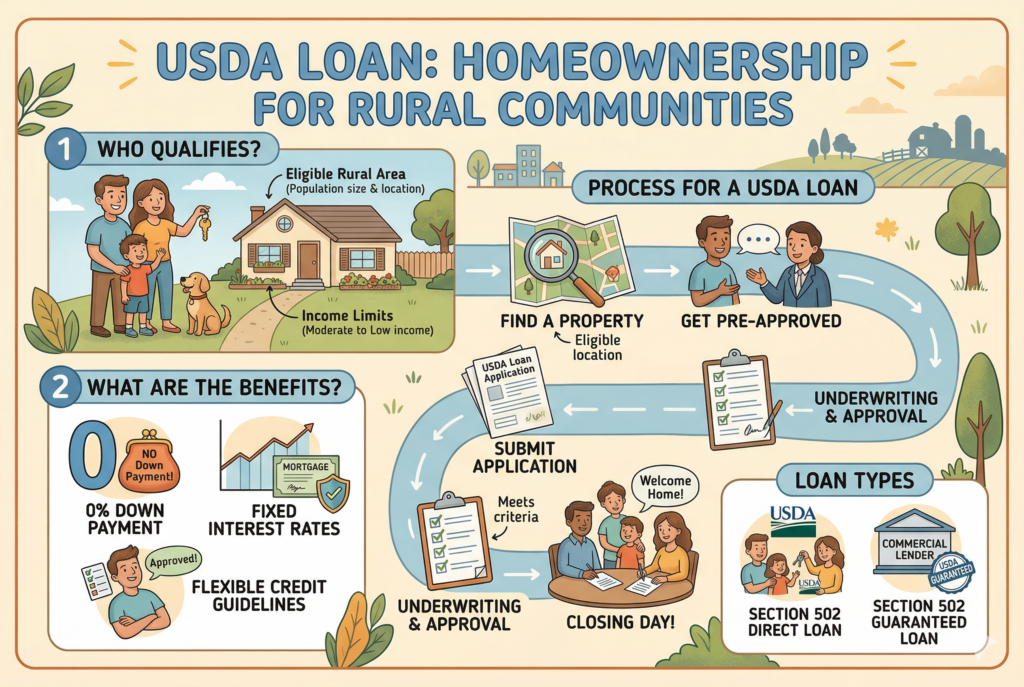

USDA Loan

A USDA loan is backed by the U.S. Department of Agriculture and is designed for certain eligible rural and suburban homebuyers. It may allow low or no down payment financing for qualified borrowers and properties. This loan type can be a useful option for buyers in eligible areas who meet income and property requirements.

How Mortgage Interest Rates Work

Mortgage interest rates are one of the biggest factors affecting your monthly payment and total loan cost. The rate you receive depends on both market conditions and your personal financial profile.

Lenders usually look at your credit score, debt-to-income ratio, income stability, down payment, loan type, and loan term. Higher credit scores and stronger financial profiles often qualify for better rates.

The difference between even two close rates can matter a lot over time. A slightly lower rate may reduce your monthly payment and save thousands of dollars over the life of the loan. That’s why comparing lenders carefully matters. The best mortgage isn’t always the one with the lowest advertised rate. Fees, points, and the APR, or annual percentage rate, also affect the real cost.

How Much House You Can Afford

Choosing the right home loan starts with affordability, not just approval. A lender may approve you for a certain amount, but that doesn’t always mean that amount fits comfortably into your budget.

A realistic mortgage payment should leave room for other financial priorities, including emergency savings, retirement contributions, maintenance costs, utilities, and everyday living expenses.

When evaluating affordability, it helps to consider your full monthly housing cost, not just principal and interest. Property taxes, homeowners insurance, mortgage insurance, homeowners association fees, and maintenance can all add up. The right loan is one you can manage consistently, even if unexpected expenses come up.

What Lenders Look For

When applying for a mortgage, lenders usually review several key factors. Your credit score helps them estimate repayment risk. A stronger score can improve both approval chances and loan pricing. Your debt-to-income ratio shows how much of your income is already committed to debt payments. Lower ratios generally make qualification easier.

Lenders also review employment history, income documentation, savings, and the amount available for a down payment and closing costs. The property itself matters too. The lender usually requires an appraisal to confirm that the home’s value supports the loan amount.

How to Choose the Right Mortgage

Choosing the right mortgage loan means looking beyond the headline interest rate. The best option depends on how long you plan to stay in the home, how much risk you’re comfortable taking, and what your monthly budget can handle.

A fixed-rate mortgage may be best for someone who wants payment stability and expects to stay for a long time. An adjustable-rate mortgage may appeal to someone with a shorter timeline and a strong plan to move or refinance.

The loan program also matters. A borrower with strong credit and a solid down payment may prefer a conventional loan. Someone with limited upfront cash may find an FHA loan more accessible. Eligible military borrowers may benefit most from a VA loan. It’s also worth comparing loan terms. A 30-year mortgage usually has a lower monthly payment, while a 15-year mortgage often comes with a lower rate and much less total interest paid.

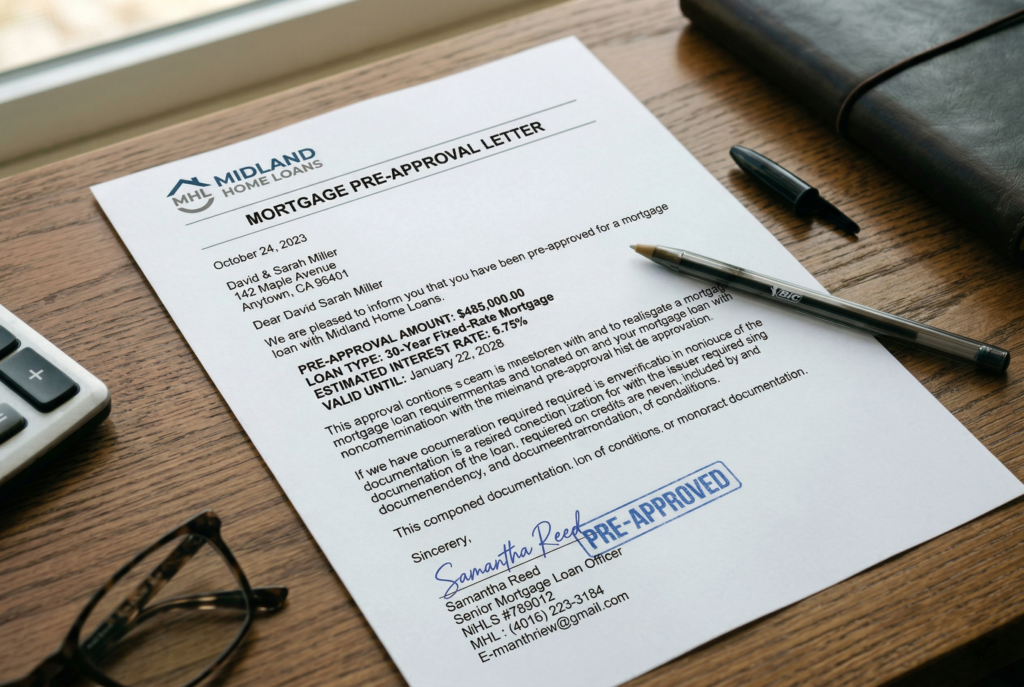

Why Mortgage Preapproval Matters

Getting mortgage preapproval can be a smart early step in the homebuying process. It gives you a clearer idea of how much you may be able to borrow and shows sellers that you’re a more serious buyer. Preapproval isn’t a final loan commitment, but it can help narrow your home search to a realistic price range. It also gives you a chance to spot financial issues early, such as credit problems or missing documentation, before you’re under contract on a home.

Conclusion

Mortgages make homeownership possible for many buyers by allowing them to spread the cost of a home over time. But not all loans work the same way. Understanding how a mortgage works, the differences between fixed-rate and adjustable-rate loans, and the pros and cons of programs like conventional, FHA, VA, and USDA loans can help you make a more confident decision.

The right home loan should match your budget, credit profile, down payment, and long-term plans. When you compare loan types carefully and look at the full cost, not just the advertised rate, you put yourself in a stronger position to choose a mortgage that supports both homeownership and long-term financial health.